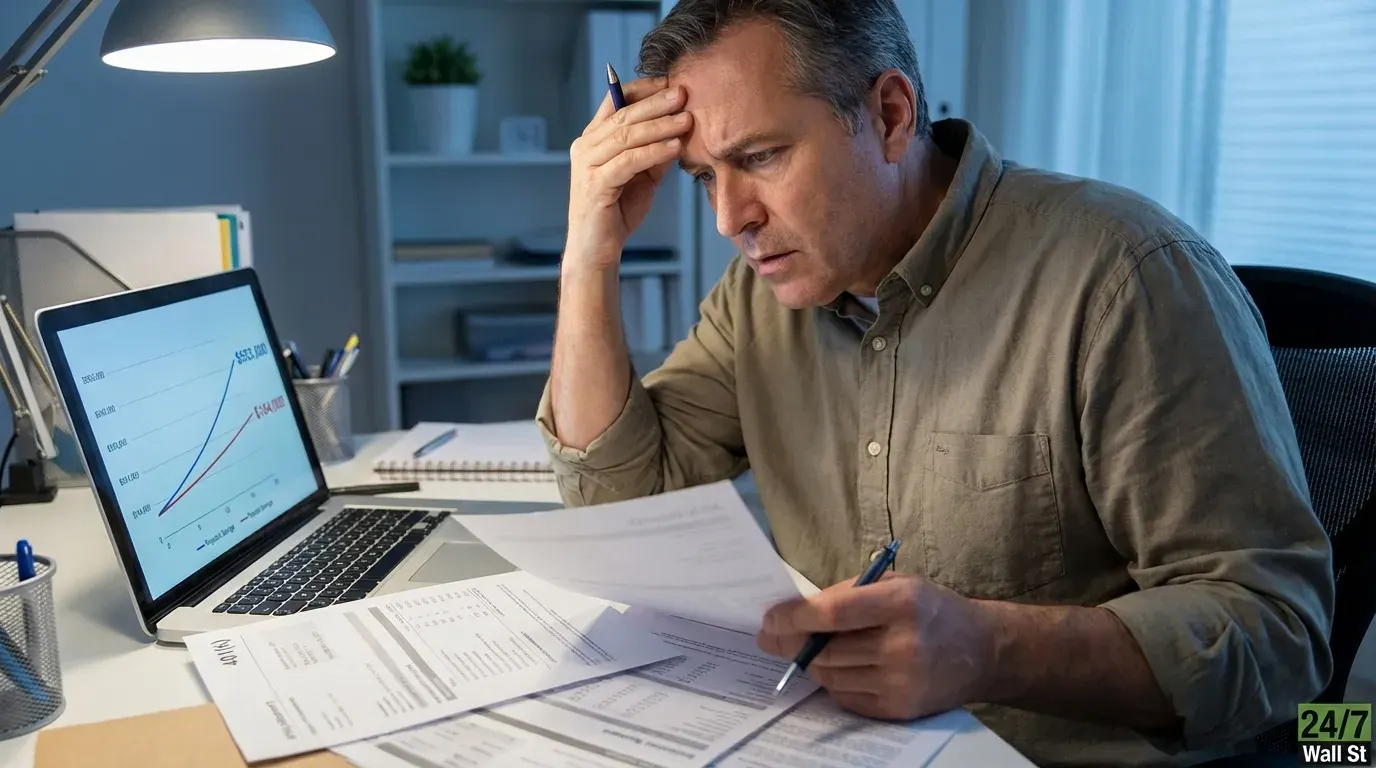

A 35-year-old auto-enrolled at 3% and left on autopilot will contribute $1,950 per year per year and arrive at retirement with roughly $184,000. That sounds like progress until you see what the same person accumulates by simply doubling their contribution rate to 6% and capturing the full employer match: closer to $553,000. The difference runs into the hundreds of thousands of dollars and comes not from market timing or stock picks, but from a single default setting that most workers never revisit.

Why 3% Became the Default

Plan sponsors set auto-enrollment defaults deliberately low. The original logic was that a low default rate would reduce opt-outs from employees worried about reduced take-home pay. Three percent felt painless. The problem is that most people never revisit the number. Research has consistently shown that inertia keeps the majority of auto-enrolled participants at whatever rate they were defaulted into, sometimes for years or even decades.

The most common employer matching structure is a 50% match on contributions up to 6% of salary, according to Fidelity and Kiplinger data from 2025. At a $65,000 salary, contributing only 3% means forfeiting half the available employer match — roughly $975 annually every year. That forfeited money, left to compound over a working career, can grow into tens of thousands of dollars in lost wealth. The employer match is the highest guaranteed return available to most workers, and the default contribution rate causes millions of people to miss it entirely.

The Auto-Escalation Feature Almost Nobody Uses

Most plans include automatic contribution escalation alongside auto-enrollment. It increases your deferral rate by 1% per year until you hit a cap, typically 10% or 15%. According to Vanguard’s 2026 How America Saves preview, 71% of plans with auto-enrollment included an automatic escalation feature. Yet the feature is almost universally opt-in, and most participants never activate it.

A 35-year-old starting at 3% and escalating by 1% annually reaches a meaningful contribution rate within just a few years. The compounding effect of those early rate increases, applied over three decades, is what produces the $200,000-plus gap — not market timing, but simply staying on a scheduled increase. The damage is not from a single bad year. It comes from years of under-contribution during the period when compounding does the most work.

Despite this, 62% of plans with auto-enrollment defaulted employees at a contribution rate of at least 4% as of year-end 2025 — still short of the 6% threshold needed to capture the full employer match in most plans. Even a 4% default leaves a meaningful employer match gap for workers whose plans match up to .

SECURE 2.0 Changed the Rules, But Only for New Plans

The SECURE 2.0 Act requires new 401(k) plans established after December 29, 2022 to auto-enroll eligible employees at a minimum of 3% and escalate automatically by at least 1% per year until reaching at least 10%. But this mandate applies only to new plans, not existing ones. If your employer’s plan predates that, the old defaults still apply and the escalation feature may be sitting dormant in your account settings right now.

Consumer sentiment data from the University of Michigan shows a reading of 56.4 as of January 2026, well below the 80-point neutral threshold. Financial anxiety is high, and it often pushes people to avoid looking at retirement accounts rather than engage with them. That is exactly the environment where auto-enrollment defaults do the most long-term damage.

Two Actions That Take Less Than Two Minutes

The fix is not complicated, but it requires actually checking account settings.

Check your current deferral rate. Workers who navigate to their 401(k) plan portal contribution settings and confirm their contribution percentage can identify whether they are leaving employer money behind. Those contributing only 3% when their employer matches up to 6% are forfeiting free money every pay period. Raising to 6% on a $65,000 salary costs roughly $1,950 more per year out of pocket but captures an equal amount in employer contributions previously forfeited.

Review the auto-escalation feature. It is usually labeled “automatic increase” or “contribution escalation” in the same settings screen. Workers who set it to increase by 1% per year can meaningfully close the gap over time. A 1% raise on a $65,000 salary is barely noticeable on most paychecks. Most people never notice it.

Workers whose combined household income is approaching Medicare’s income-related premium thresholds may find that increasing pre-tax 401(k) contributions also reduces modified adjusted gross income, which can protect against Medicare premium surcharges in retirement. That conversation is worth having with a fee-only advisor, but the starting point is confirming the current contribution rate.