AtaiBeckley (ATAI) is back in focus after two catalysts: inclusion in major US equity indices and publication of peer reviewed Phase 2a data for its BPL-003 nasal spray in treatment resistant depression.

See our latest analysis for AtaiBeckley.

Despite the fresh index inclusions and progress with BPL-003, the share price is US$3.54 and short term momentum has been weak, with a 1 month share price return of 10.83% decline and a 90 day share price return of 15.51% decline. However, the 1 year total shareholder return of 140.82% and 3 year total shareholder return of 122.64% still point to a very strong move over a longer window.

If you are tracking how clinical news can reshape sentiment across the sector, this is a good moment to scan other opportunities through 36 healthcare AI stocks

With AtaiBeckley trading at US$3.54, are recent index inclusion and BPL-003 progress already reflected in the price, or are investors still applying a heavy discount that could leave room if the pipeline executes and markets price in future growth?

DCF valuation: does a big gap to fair value change the story?

According to the SWS DCF model, AtaiBeckley has an estimated future cash flow value of $16.76 per share, compared with the last close of $3.54, which implies a large discount. That is a wide gap for a company with a clinical stage pipeline and limited current revenue.

The DCF model projects future cash flows for AtaiBeckley, then discounts them back to today using a required rate of return. For a business that is currently loss making, the model leans heavily on assumptions about when cash flows could inflect and how large they might eventually become rather than on present day earnings.

Here, that means the DCF outcome is highly sensitive to expectations around the mental health portfolio, including assets such as BPL-003 for treatment resistant depression and alcohol use disorder, RL-007 for cognitive impairment associated with schizophrenia, and other candidates that are still in clinical trials. With reported revenue of $4.1m and a net loss of $660.0m, the current financials are not driving the valuation result; the projected future cash flows are.

Look into how the SWS DCF model arrives at its fair value.

Result: DCF Fair value of $16.76 (UNDERVALUED)

However, you still need to weigh clinical trial setbacks or delays and the current $660.0m net loss, as both could challenge the long term upside story.

Find out about the key risks to this AtaiBeckley narrative.

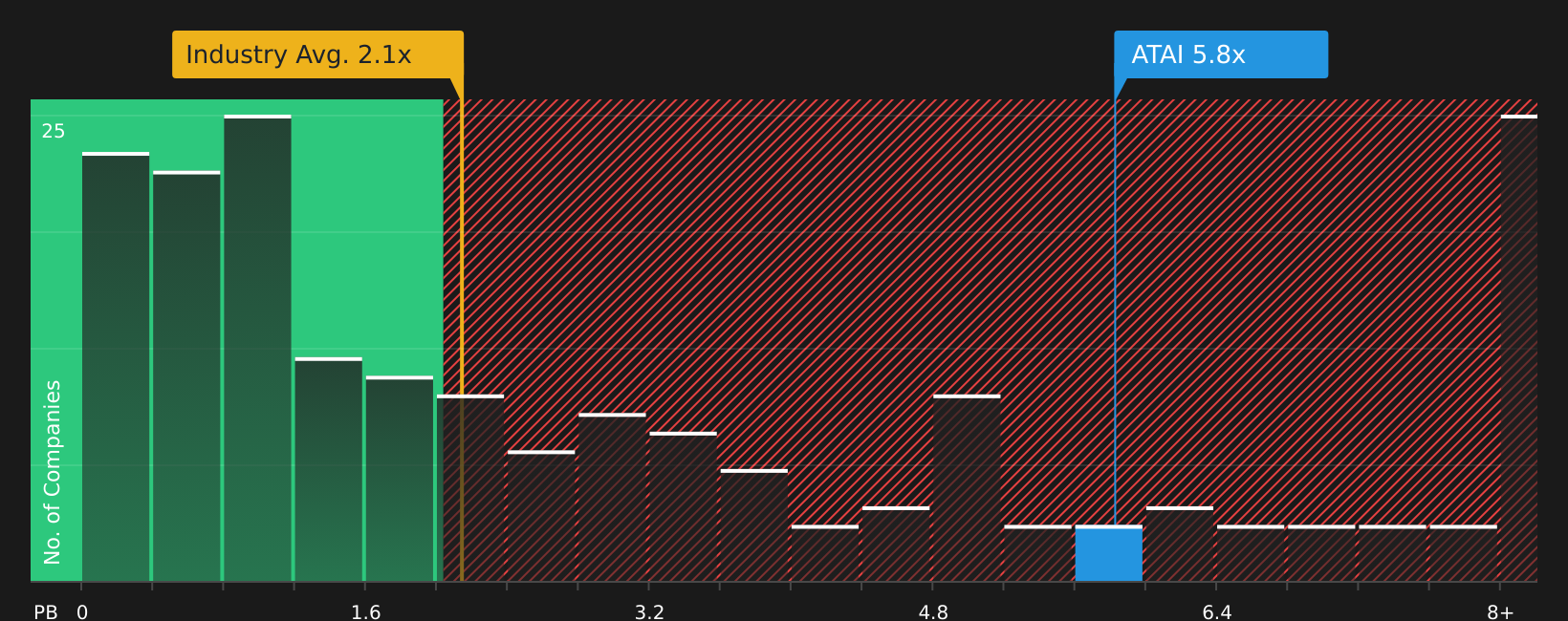

Another View: What P/B Says About Market Expectations

While the SWS DCF model points to a large discount, the P/B ratio tells a very different story. AtaiBeckley trades at 5.8x book value, compared with 2.1x for the US Pharmaceuticals industry and 5.7x for its peer group, which suggests the stock is priced at a premium on this measure.

That kind of gap can signal that the market is already baking in strong expectations around the mental health pipeline, even with limited current revenue and ongoing losses. For you as an investor, the question is whether this premium feels like a buffer or a risk if sentiment changes.

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGM:ATAI P/B Ratio as at Mar 2026

NasdaqGM:ATAI P/B Ratio as at Mar 2026

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AtaiBeckley for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match – so you never miss a potential opportunity.

Next Steps

The mix of upside and risk in this story is clear, so move quickly, review the data for yourself, and weigh AtaiBeckley using 2 key rewards and 4 important warning signs.

Looking for more investment ideas?

Once you have formed a view on AtaiBeckley, do not stop there. Broaden your watchlist with other ideas that fit different roles in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com