Never miss an important update on your stock portfolio and cut through the noise. Over 7 million investors trust Simply Wall St to stay informed where it matters for FREE.

Lumentum Holdings (NasdaqGS:LITE) has exchanged nearly US$475 million of convertible senior notes for approximately 5.7 million common shares.

This capital structure change comes alongside a US$2 billion private investment from Nvidia and a multi year supply agreement.

The company is positioned as a key optical technology provider for Nvidia linked AI data center projects.

Lumentum focuses on optical and photonic technologies that sit inside communications networks and data centers, areas that are central to rising AI computing needs. With Nvidia committing US$2 billion and a supply agreement, Lumentum’s role in high speed optical links for AI data center build outs is now firmly in the spotlight. Readers following infrastructure around AI training and inference may see this as a way to look beyond GPUs and into the networking layer that connects them.

The convertible note exchange increases the common share count and adjusts the company’s mix of debt and equity, which can affect earnings per share math and potential dilution over time. Investors tracking NasdaqGS:LITE may now want to follow how the Nvidia partnership and AI related demand interact with this new capital structure, including any future financing steps, product wins or updates on AI data center deployments tied to the agreement.

Stay updated on the most important news stories for Lumentum Holdings by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Lumentum Holdings.

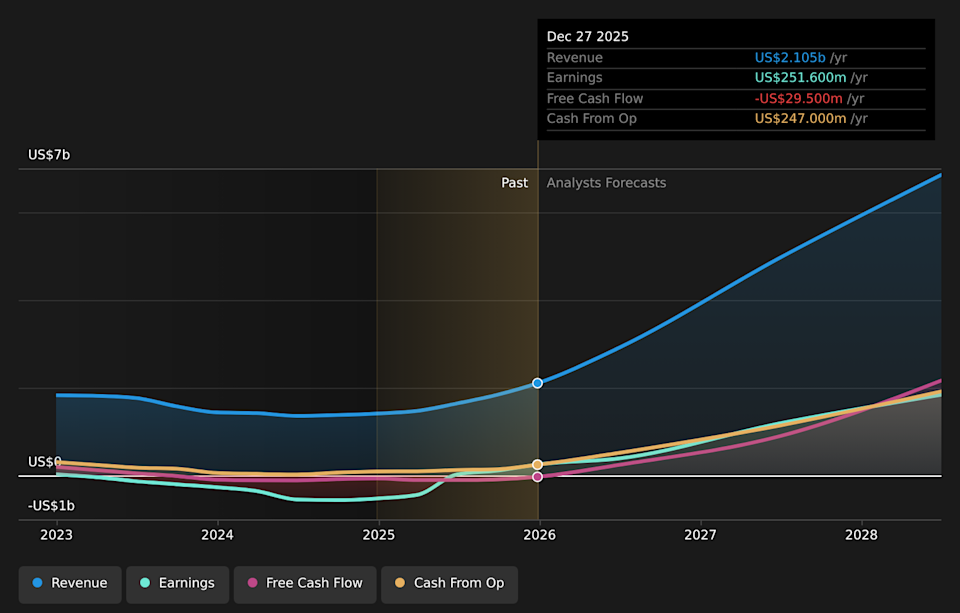

NasdaqGS:LITE Earnings & Revenue Growth as at Apr 2026

NasdaqGS:LITE Earnings & Revenue Growth as at Apr 2026

We’ve flagged 4 risks for Lumentum Holdings. See which could impact your investment.

The Nvidia partnership and the convertible note exchange reshape both Lumentum’s customer mix and its balance sheet at the same time. On one side, multibillion dollar purchase commitments and a US$2b preferred investment from Nvidia signal that Lumentum’s optical technology is tightly linked to AI data center build outs at hyperscalers. On the other, swapping roughly US$474.6m of convertible notes for 5.7 million shares reduces financial liabilities while increasing the share count, which can influence per share metrics investors track.

The Nvidia funding, purchase commitments and new Greensboro InP facility directly support the narrative that capacity expansion and AI focused optics can be a key growth catalyst for Lumentum’s cloud and networking franchise.

Relying more heavily on a small group of large AI and cloud customers, including Nvidia, reinforces the concentration risk highlighted in the narrative, especially compared with peers like Coherent, Broadcom and Marvell that also supply data center optics.

The decision to exchange a large block of convertible notes for equity, and the specifics of the preferred stock structure, are not fully captured in the earlier narrative and may change how investors think about leverage, dilution and future capital allocation.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Lumentum Holdings to help decide what it is worth to you.

⚠️ Higher customer concentration, with Nvidia and a few hyperscalers driving a large share of demand, leaves results more exposed if any one account changes its AI optics roadmap.

⚠️ Analysts have flagged 4 key risks, including concerns that debt is not well covered by operating cash flow, which means execution on new capacity and AI programs will be closely watched.

🎁 The company is benefiting from strong earnings and revenue momentum, with earnings forecast to grow 72.07% a year and the business having recently moved into profitability.

🎁 Lumentum is flagged as trading 50.6% below one estimate of fair value, which some investors may view as upside potential if AI optics demand and long term agreements with customers such as Nvidia play out as expected.

From here, focus on how quickly Lumentum converts Nvidia’s US$2b investment, multiyear supply agreements and the Greensboro facility build out into sustainable orders and margins, especially relative to rivals such as Coherent and Fabrinet in AI data center optics. Quarterly updates around the planned fiscal Q3 2026 earnings release on May 5, progress on the US manufacturing ramp to mid 2028 and any further balance sheet changes after the note exchange will give a clearer picture of how durable this AI driven demand looks against the added dilution and capital spending commitments.

To ensure you are always in the loop on how the latest news impacts the investment narrative for Lumentum Holdings, head to the community page for Lumentum Holdings to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LITE.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com