Key insights: Visa and Mastercard are building mobile wallet scale through a series of partnerships.

What’s at stake: Both card networks say internal research is tracking popularity for mobile wallets.

Forward look: Apple’s agreement with EU regulators to open its NFC technology will draw more wallet providers in the next year.

As 2025 winds to a close, Mastercard has advanced two partnerships designed to enable merchant access to mobile wallets in dozens of countries, joining rival Visa in building global distribution as consumers and merchants migrate more of their lives to smartphones.

Mastercard’s December moves include a collaboration with TerraPay, a London-based cross-border payments company, to enable TerraPay’s mobile wallet users to access more than 150 million Mastercard acceptance points for Near-Field Communication-based payments.

NFC is a key enabling technology for smartphone payments. Under regulatory pressure, Apple has agreed to ease access to NFC, which the tech giant traditionally controlled. This is expected to open the market to dozens of mobile wallets, creating a need for Visa and Mastercard to broaden their ability to support a range of new ones.

Mastercard’s TerraPay partnership comes as the card brand plans to boost mobile wallet usage in Latin America via a joint venture with Telefonica, a Madrid-based telecom. Telefonica and Mastercard plan to launch a mobile wallet in Brazil and surrounding countries that could have an addressable market of up to 87 million consumers.

Mastercard’s other recent collaborations include “Pay like a local,” a partnership between: Alipay and Mastercard to offer international travelers an option to make cashless payments in China; an integration with Alipay Wallet; and a contactless pay technology tie-up with Alipay.

“Collaborations with key ecosystem players like Terrapay play a key role in scaling the positive impact via their multiple wallet partners and simplifying the implementation process,” said Prakriti Singh, executive vice president for core payments at Mastercard for Europe, the Middle East and Africa, in a statement.

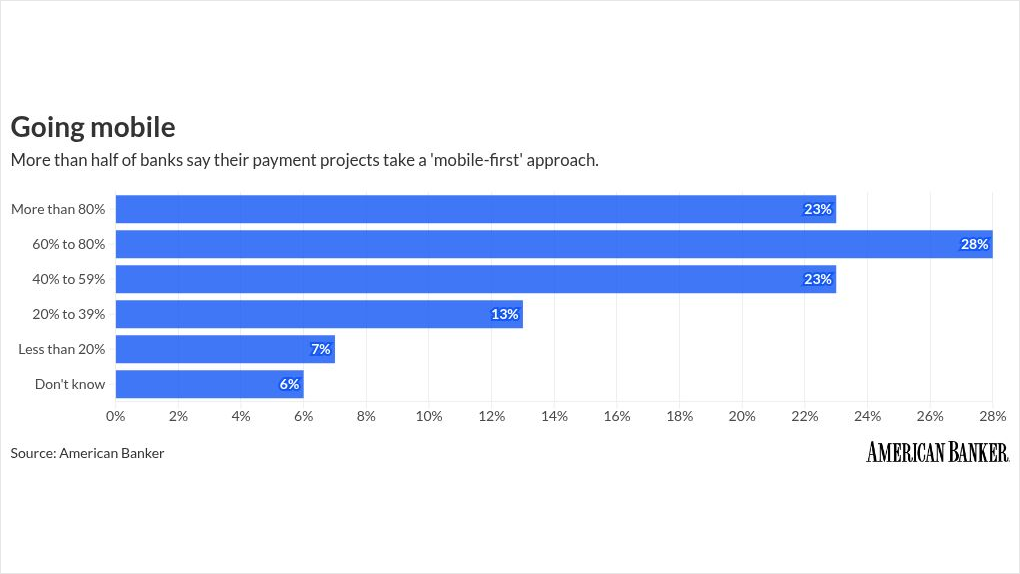

Seventy percent of in-person Mastercard transactions are now contactless, the card network said, suggesting the popularity of mobile wallets is migrating from e-commerce to brick and mortar. Banks are also embracing mobile wallets. More than half of banks say at least 60% of their payment initiatives take a “mobile first” strategy, according to research from American Banker.

Story Continues

Like Mastercard, Visa has made a series of partnerships to scale its mobile wallet strategy.

Visa recently announced a digital wallet partnership with BBVA in Spain that combines Visa’s Token Service with the bank’s payment technology to enable BBVA’s mobile wallet. (A “token” in this case refers to digital payments security, not migrating services to a blockchain.)

Other Visa mobile wallet projects in the EU include an iOS/Android contactless mobile payment collaboration with Klarna; a Visa co-wallet with Vipps Mobile Pay in the Nordics; and a planned 2026 pilot with Bancomat, an Italian digital payments product.

“This will enable consumer choice, which is a big underlying issue for us and our strategy,” Mathieu Altwegg, senior vice president and head of product and solutions for Europe at Visa, told American Banker.

Visa also cited its own research, reporting mobile payments make up 59% of all e-commerce transactions in Europe, with growth on pace to reach 75% in the next four years. Thirty-two percent of European consumers only use mobile wallets for payments, according to the card brand.

“We’re seeing demand for these wallets, both to pay online and for face to face transactions,” he said.

Altwegg did not directly address Apple’s EU NFC settlement, but noted a proliferation of wallets. “Being able to use different types of wallets will level the playing field,” he said.

In Europe, the threat to the card networks is Europe’s bank-led wallets that use direct bank transfers instead of card networks, according to Ron van Wezel, a strategic advisor for Datos Insights.

“Bank consortia provide digital wallets across Europe, launched through collaborative efforts between multiple banks,” Van Wezel told American Banker, noting that common successful bank-led wallets for specific domestic markets include MobilePay in Denmark, Swish in Sweden, Vipps in Norway and Bizum in Spain.

“They’re direct bank account payment systems that compete with cards,” Van Wezel said. “When someone pays with these wallets, the money moves bank-to-bank via SEPA instant transfers, with no Visa, no Mastercard, and no interchange fees.”

This is why the Apple/EU settlement matters so much, Van Wezel said, adding that these bank wallets couldn’t work on Apple devices at the point-of-sale prior to Apple’s EU settlement.

In this environment it’s critical that cards be available in digital wallets, Tony DeSanctis, a senior director at Cornerstone Advisors, told American Banker. “The question is which wallets are going to be relevant,” he said.