The final data releases have now been received in 2025, the latest the RBNZ banking data dump. That includes their C5 series tracking the size and movements in the overall loan books of lenders.

And the biggest set within that is for home loans, accounting for almost 64% of all lending, and 2025 saw this reach its record high.

Lending for housing is now at $388 bln* of all lending which now totals $609 bln.

The economy may not have grown, but our housing debt did.

Our collective ability to service this debt got easier in 2025, and our monthly home loan affordability reviews show this was true for first home buyers as well.

Lending for housing grew +5.6% in the year to November, much faster than the +3.6% in the near to November 2024, and the +2.9% in 2023. But that was less than the +7.0% compound growth in the five year period 2015 to 2020. And far less than the +21% in 2021.

But of course, this expansion wasn’t even among all banks. Interestingly, the two main banks with the smallest market share five years ago have made the largest gains through to 2025.

We have granular detail about individual banks to September 2025 from the RBNZ Dashboard.

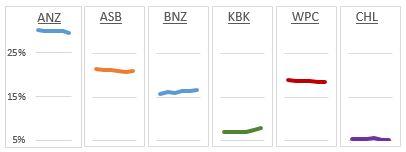

This is a chart representation of the quarterly market share shifts over the past five years.

Only BNZ and Kiwibank are ending 2025 with higher market shares than where they started in 2020.

Mortgage market shares change slowly because of the very large embedded bases that are on fixed rates. Competition is fierce mainly because every bank knows who they lost and are able to target them to win them back. And with interest rates very little different between banks, the incentives to change have to be material to make the effort worthwhile.

In the past five years, ANZ has seen its mortgage book rise by +$26.4 bln to $113.9 bln. ASB’s rose +$18.6 bln, BNZ by +$18.0 bln, Kiwibank by +$9.9 bln and Westpac by +$15.8 bln. It has been a period where “everyone wins”, just some more than others.

Kiwibank’s outsized drive to win mortgage share by concentrating on getting the support of mortgage brokers has helped them in the past two years (including via its captive NZHL network).

Challenger banks (CHL) however aren’t really getting a look in.

* And just for the record, the RBNZ data shows the value of all residential housing is currently $1.65 tln, giving a national LVR of 23.4%. Household debt as a percentage of household disposable income has been little-changed in over 20 years. And household debt servicing is currently at its long-run (25 year) average level.