ppeal to needle-averse people and be perceived as easier to access, even if pricing and supply still matter. If that holds, forecasts for the pill may prove conservative, and Novo’s early launch and marketing push could help it stay ahead in oral options.

Why should I care?

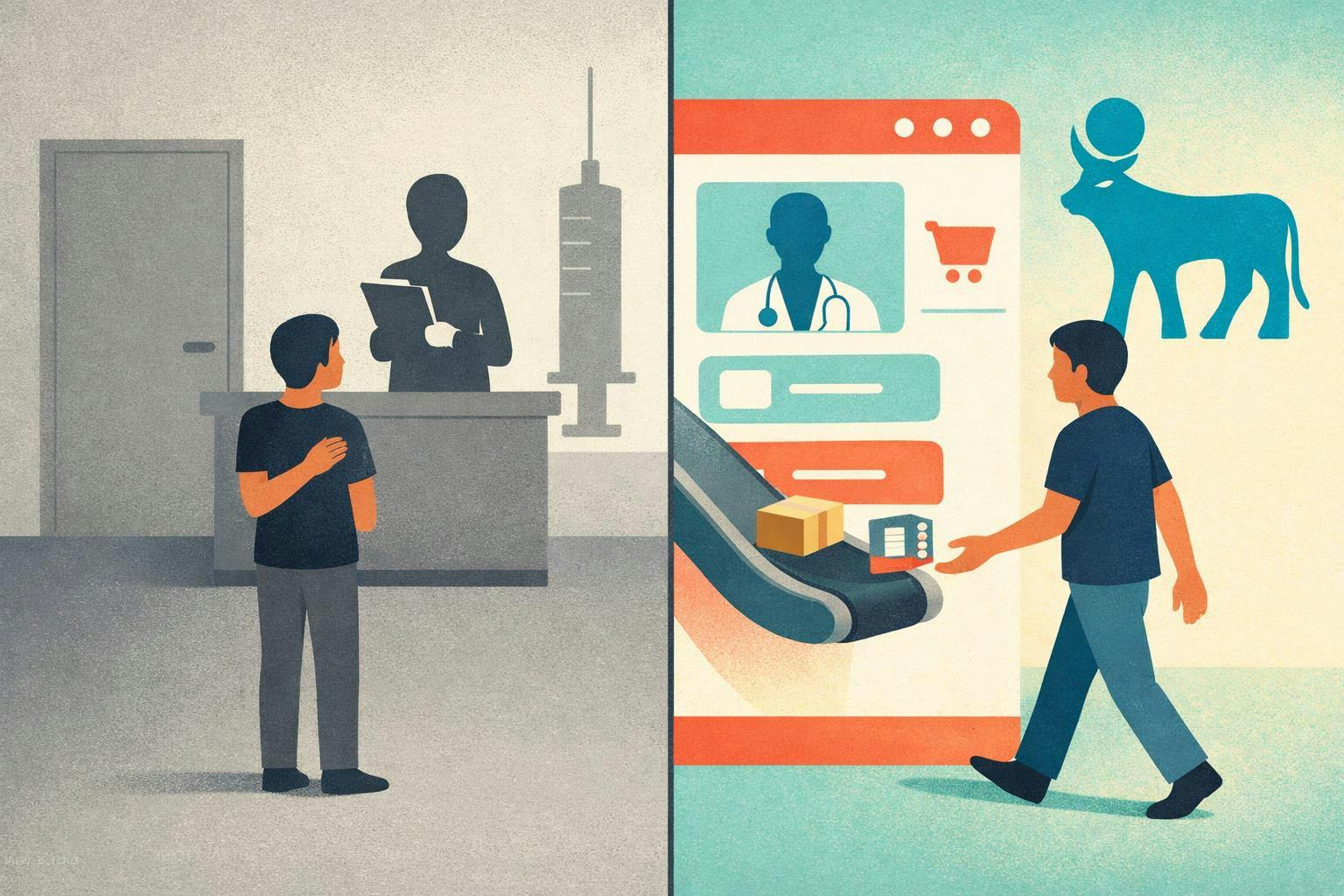

For markets: Access is becoming part of the moat.

GLP-1 competition is shifting from “best drug wins” to “best drug plus easiest pathway.” Berenberg kept a buy rating and reiterated a 415 Danish kroner price target, citing signs of stronger consumer traction after the NovoCare upgrade. If online onboarding, prescribing, and fulfillment drive more of the category’s growth, firms with smoother digital funnels and reliable supply could gain share, while slower movers risk being boxed out.

Zooming out: Obesity care is getting consumerized.

Telehealth and online pharmacies are pulling weight-loss treatment into the same digital lane as routine care, lowering the friction of appointments and refills. That can expand the market beyond patients willing to navigate injections, referrals, and long waits. As pills broaden adoption, differentiation may increasingly hinge on perceived affordability, availability, and how quickly someone can start – not only clinical trial data.