Paramount Skydance, listed as NasdaqGS:PSKY, is reported to be exploring a takeover bid for Warner Bros. Discovery that could affect Warner’s current deal with Netflix for key studio and streaming assets. Public remarks from advisers involved in the talks indicate confidence in Paramount Skydance’s interest, while Warner Bros. Discovery is said to be open to a revised and higher offer. The situation places Paramount Skydance in the middle of a high profile contest over control of content libraries and distribution rights across major streaming platforms.

Paramount Skydance shares most recently traded at $10.75, with the stock showing a 5.2% decline over the past week and a 17.2% decline over the past month. Year to date, NasdaqGS:PSKY is down 18.4%, and over the past 3 years the share price decline is 49.3%, extending to 78.6% over 5 years. This gives the new bid added relevance for existing shareholders who are monitoring the company’s direction.

The potential move on Warner Bros. Discovery puts a spotlight on how Paramount Skydance may try to reshape its content footprint and streaming partnerships. As the bidding and deal terms evolve, investors can monitor updates on how any revised proposal might affect control of key assets and the company’s role in future distribution agreements.

Stay updated on the most important news stories for Paramount Skydance by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Paramount Skydance.

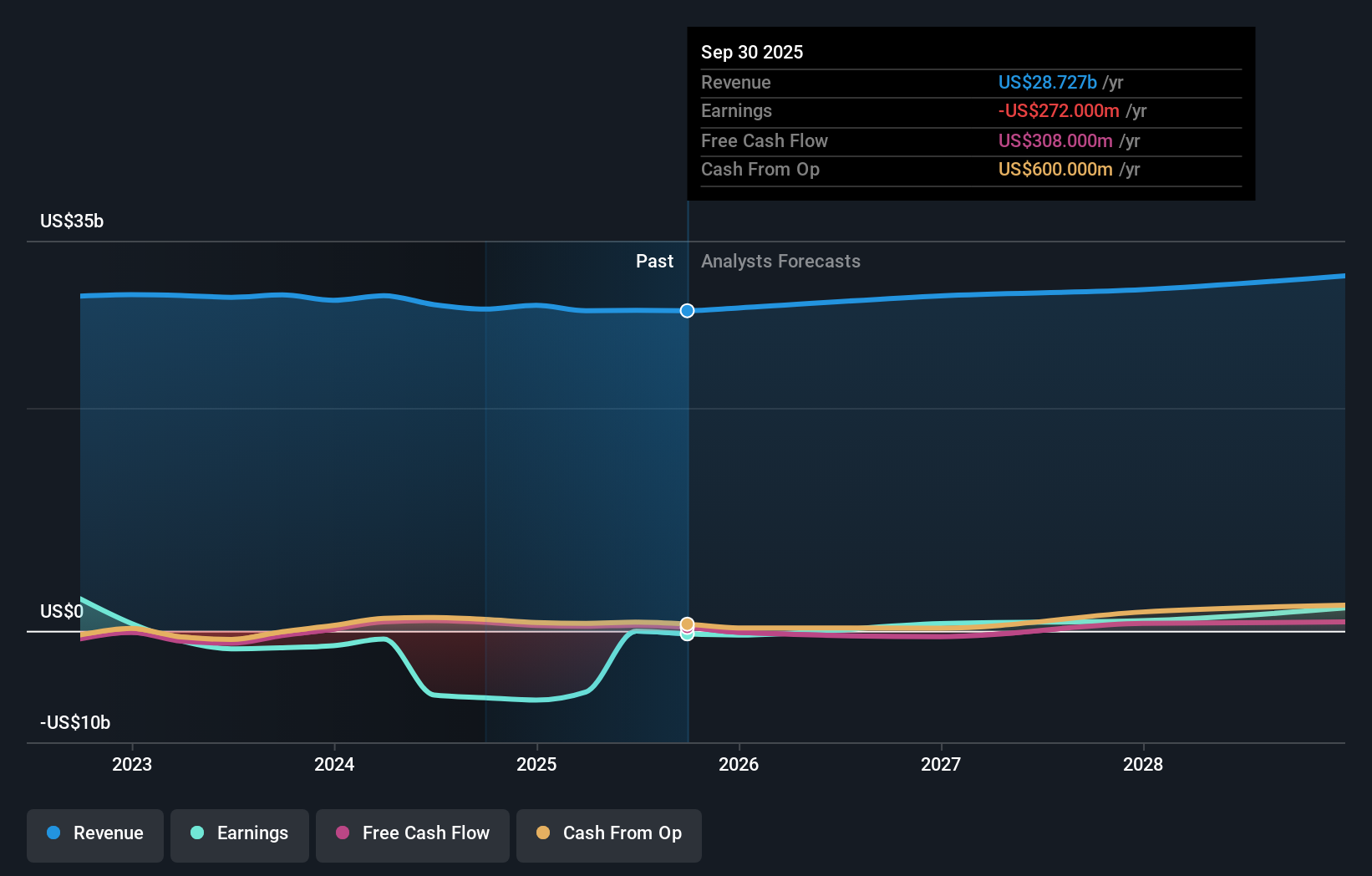

NasdaqGS:PSKY Earnings & Revenue Growth as at Feb 2026

NasdaqGS:PSKY Earnings & Revenue Growth as at Feb 2026

How Paramount Skydance stacks up against its biggest competitors

The potential takeover bid for Warner Bros. Discovery would be a major swing at scale for Paramount Skydance, putting it in more direct competition with Netflix, Disney and Comcast for control of studio libraries and streaming rights. Set alongside its existing content deals, including the expanded Sky partnership in New Zealand, the move signals an effort to secure both owned franchises and long-duration distribution pipelines rather than relying only on third party licensing.

How this fits into the Paramount Skydance narrative

The possible Warner Bros. Discovery deal sits on top of an existing plan that already leans heavily on more premium content, larger theatrical slates and a bigger Paramount+ footprint. If Paramount Skydance were to combine its current content plans with Warner’s franchises and studio assets, it would reinforce the narrative of using a broader library and recognizable brands to feed film, streaming, licensing and consumer products across multiple markets.

Risks and rewards investors are weighing ⚠️ A large acquisition on top of higher content investment could strain the balance sheet and raise questions about how comfortably interest costs and future dividends, such as the recently affirmed US$0.05 quarterly payment, can be supported. ⚠️ Integration risk is significant, as bringing together two big studios while Warner Bros. Discovery already has an agreed deal with Netflix could lead to complex regulatory, contractual and execution challenges. 🎁 Control of a larger combined content library could give Paramount Skydance more negotiating leverage with distributors and advertisers, especially as it pushes Paramount+ and other direct to consumer offerings. 🎁 If the bid terms are structured carefully, the company could increase its long term content supply and potential revenue streams without losing the flexibility to keep selective licensing deals with partners such as Sky. What to watch next

From here, the key things to track are whether Paramount Skydance formalizes a revised offer, how Warner Bros. Discovery responds relative to the existing Netflix agreement, and what management says on the upcoming earnings call about funding, integration and capital allocation priorities. If you want a broader context for how this potential deal lines up with longer term growth plans and risks, check community narratives on Paramount Skydance here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com