Nintendo (TSE:7974) has reduced Switch 2 production targets after an initial post-launch surge. The shift comes despite early game successes, including the strong reception of Pokémon Pokopia. Management is reassessing long term demand for the console and its software lineup.

Nintendo, best known for its Switch hardware and franchises like Mario, Zelda and Pokémon, sits at the intersection of console hardware and first party software. The decision to pull back on Switch 2 production after a record-setting launch puts more attention on how hardware cycles and game releases interact over time. For you as an investor, it highlights how quickly demand expectations can change even when early sales data looks encouraging.

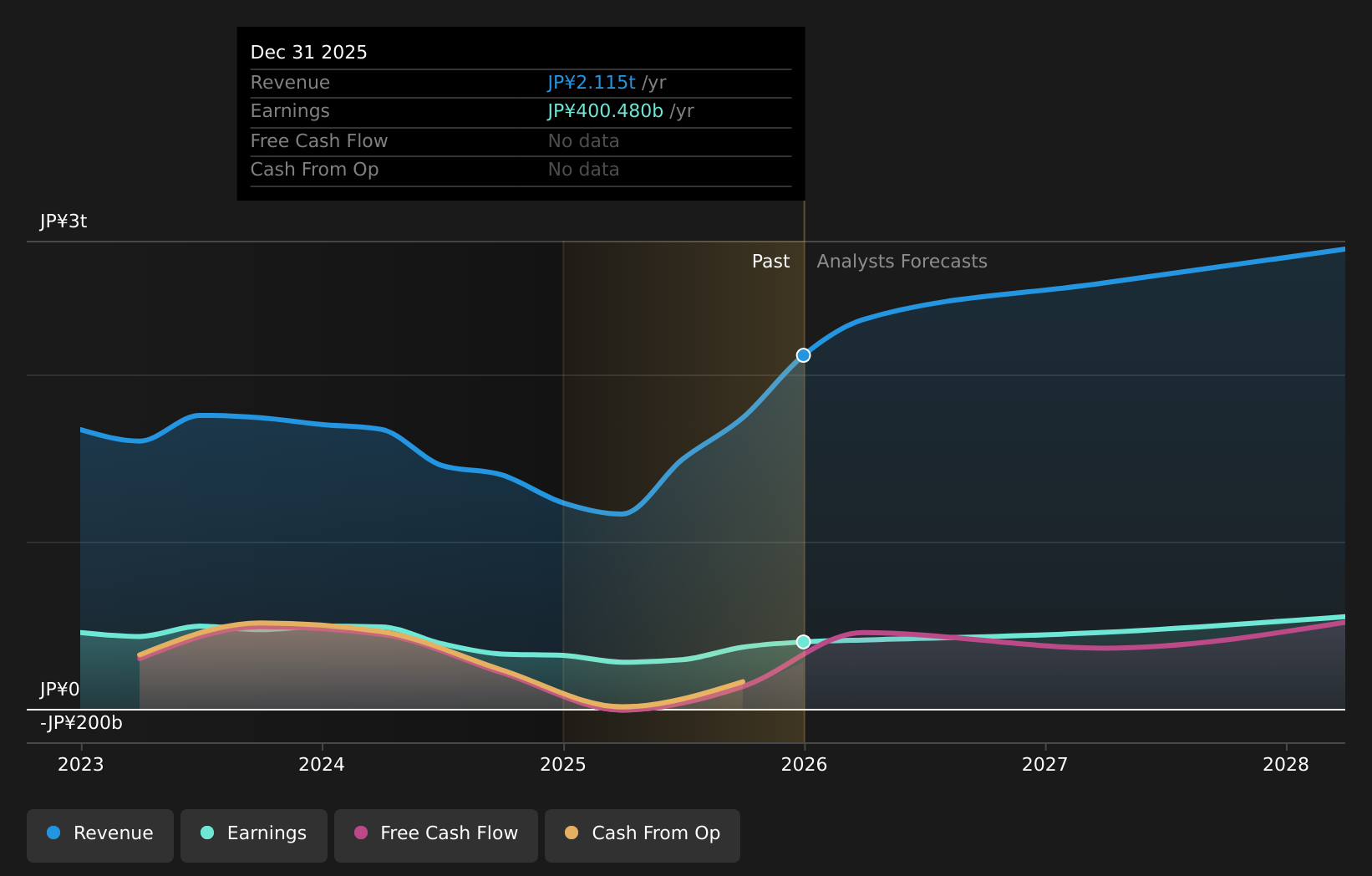

This production reassessment also raises questions about how management thinks about inventory risk, pricing power and the mix between hardware and software revenue. While the company has signalled caution on long term demand, the eventual path of Switch 2 sales and attach rates for titles like Pokémon Pokopia will be important reference points for how stable Nintendo’s cash flows from this cycle might be.

Stay updated on the most important news stories for Nintendo by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Nintendo.

TSE:7974 Earnings & Revenue Growth as at Mar 2026

TSE:7974 Earnings & Revenue Growth as at Mar 2026

📰 Beyond the headline: 1 risk and 3 things going right for Nintendo that every investor should see.

The decision to scale back Switch 2 production, even with strong early reception for games like Pokémon Pokopia and the new Super Mario Bros. Wonder edition, points to Nintendo prioritising hardware profitability and inventory discipline over chasing headline unit volumes. For you as an investor, it underlines how dependent the business model is on timing hardware cycles correctly and keeping a steady flow of high quality first party titles that justify console ownership. Softer-than-hoped demand in the US during the holiday period suggests consumer appetite may be more sensitive to price, upgrade fatigue, or competing devices from Sony and Microsoft, which can limit how aggressively Nintendo pushes supply.

The Risks and Rewards Investors Should Consider ⚠️ Lower Switch 2 production targets increase the risk that fixed hardware development and marketing costs are spread over fewer units, which can pressure margins if not offset by higher software or digital revenue. ⚠️ Reassessing long term demand highlights execution risk around the console cycle, especially if competitors launch attractive hardware bundles or services that pull players away from Nintendo’s ecosystem. 🎁 The decision to reduce output early may help avoid discounting and excess inventory, supporting pricing discipline on both hardware and limited edition bundles tied to major franchises. 🎁 Strong engagement around Pokémon and Mario releases at events like PAX East shows that Nintendo’s core intellectual property still attracts players, which can support recurring software and add on content sales per active console. What To Watch Going Forward

From here, focus on how hardware unit trends line up with software performance for Switch 2, particularly attach rates for titles like Pokémon Pokopia and upcoming Pokémon Champions. Any further adjustments to production guidance, regional pricing, or promotional activity will give you clues about how confident management is in sustaining demand across the current console cycle. It is also worth tracking how Nintendo positions its ecosystem as Sony and Microsoft refine their own hardware and subscription offerings, because shifts in player time and spending across platforms can be just as important as headline console shipment numbers.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Nintendo, head to the

community page for Nintendo to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Nintendo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com