Just when you thought India’s payments story couldn’t get any more interesting, the iPhone maker is quietly preparing its next move.

Apple Inc. is reportedly considering launching Apple Pay in India by mid-to-late 2026. Apple is in talks with ICICI, HDFC, and Axis Bank, along with global card giants Visa Inc. and Mastercard to bring its payments ecosystem to the country. Apple Pay could roll out in phases:

Open FREE Demat Account within minutes!Join now

Starting with card-based contactless payments, where users can simply tap their iPhone or Apple Watch on NFC machines to pay. That’s a notable shift, considering Indian-issued cards can’t even be added to Apple Wallet right now.

Then, Apple might go a step further and plug into UPI itself, subject to regulatory approvals, opening the door to QR-based payments that power India’s digital economy.

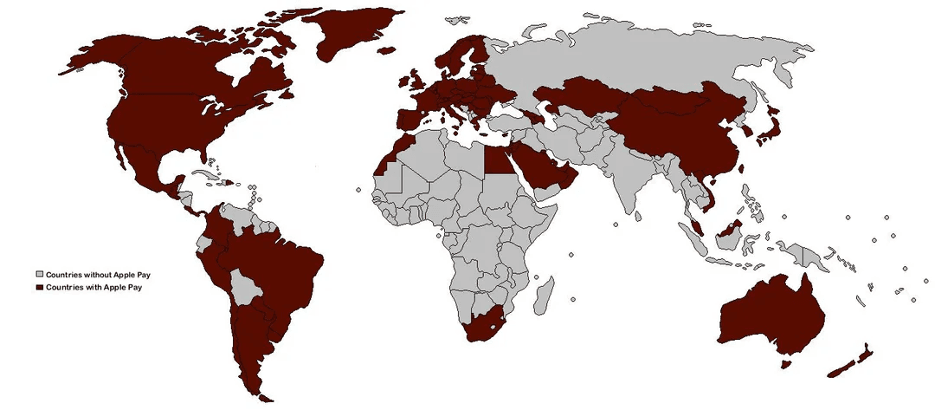

To understand why this move matters, it’s important to first look at Apple Pay’s global footprint. Apple Pay is already live in about 89 countries:

Source: Apple, As of January 2025

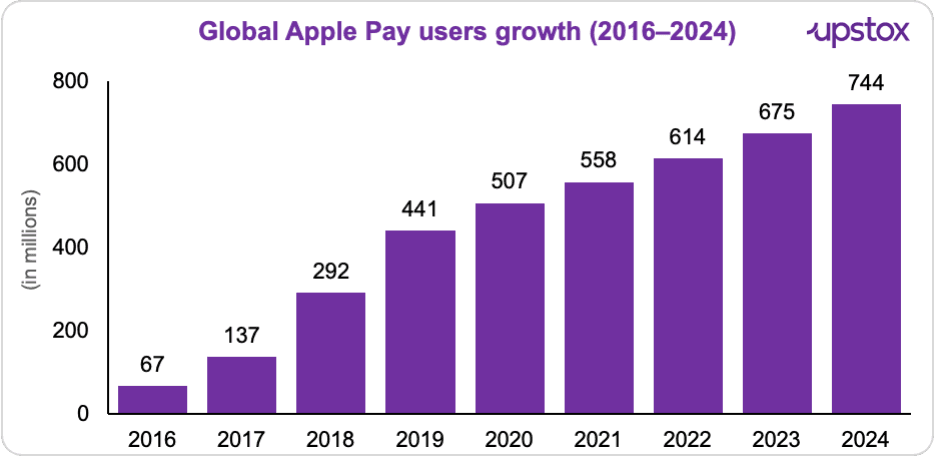

Apple Pay’s user base has grown rapidly, rising from 67 million in 2016 to around 744 million in 2024.

Source: Capital One

The question isn’t just where Apple Pay operates, but how it fits into the global payments ecosystem. With digital wallet transactions at $3.6 trillion in 2024, its India entry is a natural next step.

Source: Capital One

Why now – And what’s in it for Apple?

User base at scale

In FY25, Apple Inc.’s India business saw net profit rise 16% to ₹3,196 crore, while revenue grew 19% to ₹79,060.5 crore.

At the same time, iPhone shipments hit a record 5 million in Q3 2025 (IDC), pushing Apple to the fourth spot. For the full year, its market share hovered around 9–10%, placing it among the top five smartphone brands, alongside a steadily expanding retail presence.

Seeking new markets

In the United States, Apple Pay has already done most of what it set out to do. With iPhones deeply embedded in everyday life and Apple Inc.’s ecosystem working exactly as intended, there isn’t much low-hanging fruit left in its home market.

That’s where India starts to look interesting. Not just because of its scale, but because it still offers something Apple’s home market doesn’t, headroom.

Now, let us look at what works in Apple Pay’s favour this time?

Stronger on security

From April 1, 2026, the Reserve Bank of India is tightening digital payment rules; moving beyond basic OTPs to dynamic, transaction-level authentication, including biometrics and device-based verification.

Now, for most players, that’s an upgrade.

For Apple Inc., it’s already the default.

Face ID, device-level security, and biometric authentication are built into how Apple Pay works. So instead of adapting to new rules, Apple walks in already aligned with them.

Limits on existing players

There’s a structural shift happening in the background.

The National Payments Corporation of India has extended the deadline to enforce a 30% cap on third-party UPI apps to December 31, 2026. In simple terms, no single app can process more than 30% of total UPI transactions.

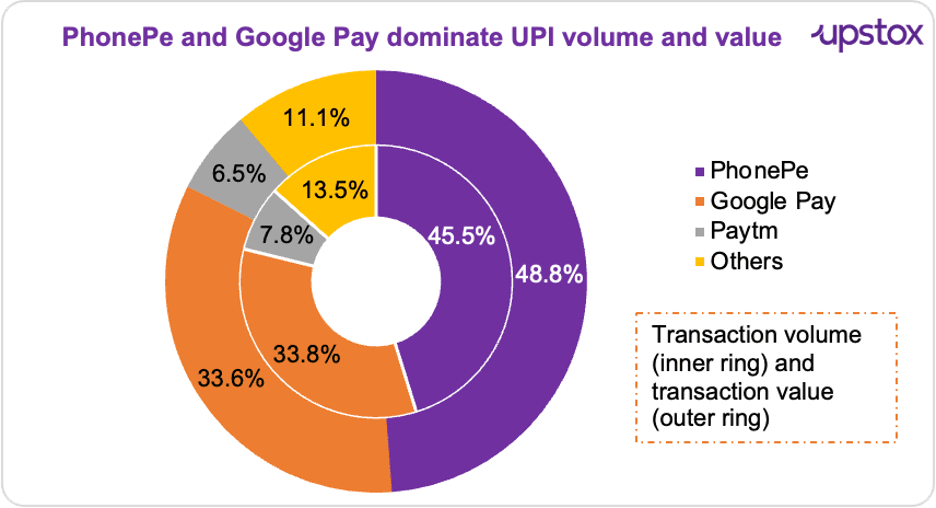

This doesn’t mean existing players like PhonePe and Google Pay will have to give up their current business overnight. Instead, it limits how much more they can grow from here. Currently, both PhonePe and Google Pay have more than 30% share each in terms of both value and volume.

Over time, as the ecosystem expands, this cap is likely to gradually redistribute incremental market share, creating room for newer players to scale up.

Then, there are other strengths Apple Pay brings along:

Apple Pay’s biggest edge lies in its ecosystem control, payments are not just app-based, but deeply embedded into the iPhone, Apple Watch, and Wallet, enabling a more seamless, device-native experience.

-It also uses a dedicated hardware component called the Secure Element, a chip within the device that securely stores payment credentials in an isolated environment.

-It also follows global EMVCo standards (used by Visa and Mastercard), using tokenisation to send a one-time payment token and dynamic security code instead of actual card details, ensuring intercepted data cannot be reused.

So, could it disrupt India’s payments landscape? Possibly. By shifting from app-based UPI to a more seamless, device-native ecosystem built into iPhones and Apple Watch.

With its strong focus on security, it could also set higher data protection benchmarks, nudging Indian players to level up their frameworks.

Where it gets tricky

The pricing challenge

Despite the favourable timing, the economics in India are very different from global markets.

Payment systems in India operate on extremely thin margins. Credit card transactions typically see blended rates of around 5 basis points, while Unified Payments Interface (UPI) transactions are processed at zero cost. In contrast, Apple Pay globally earns around 0.15–0.20% (15–20 basis points) per transaction.

This raises a key question – will Apple adapt to India’s low-margin structure?

It likely has to. Instead of relying on transaction fees, Apple may need to compress pricing and lean on ecosystem driven value. After all, India’s payments market is built on scale and volume, not high per-transaction margins.

UPI-first reality

Apple is expected to support both card payments and UPI in India.

But India isn’t a card-first market. It’s a UPI-first one. Most daily transactions, especially small-ticket payments under ₹500, happen through QR scans and peer-to-peer transfers.

Apple Pay has traditionally been stronger in card-linked payments, while UPI drives the bulk of everyday transactions. Even though Apple plans to support UPI, making it work seamlessly will require approvals from the NPCI and integration with a large network of over 600 banks.

Source: PIB

So even if Apple enters with both, success will depend on how well it adapts to a system that isn’t built around cards.

Competition is pretty strong

In February 2026, PhonePe stayed firmly ahead with ~9.3 billion transactions, accounting for nearly half of all UPI volumes. Google Pay followed with ~6.7 billion transactions, holding about a third of the market. Together they still hold over 80%.

These apps have become super-apps with bills, investments, rewards – the full package. Apple Pay, living inside the Wallet, might feel simpler at first, especially outside the premium iOS crowd (still about 10% of phones).

Source: PIB, data as of Feb 2026

Is it a boom or threat to Indian markets?

It can be seen as both.

On one hand, Apple Pay’s entry could strengthen the ecosystem in India—better security through biometrics, improved user experience, and stronger competition, especially in premium segments.

On the other hand, it is not entering for scale, but for value. iPhones account for roughly 10% of the smartphone base, yet this segment contributes a higher share of transaction value. Any shift here could affect existing players where monetisation is more concentrated.

Structural realities, however, remain. UPI dominates everyday payments, Android leads in user share, and transaction fees are minimal.

For Apple, success will depend on differentiation.

At the same time, as we discussed above, execution may not be straightforward. According to Bloomberg, Apple’s ongoing discussions with Indian banks have already seen pricing emerge as a key bottleneck, with the possibility of an initial rollout through a smaller banking partner where negotiations could be more flexible.

As a result, the impact may not be about scale, but about where value sits, shaping the premium layer of the market rather than the entire payments ecosystem.

Disclaimer: Views and opinions expressed in the article are the author’s own and do not reflect those of Upstox.