Unity Software (NYSE:U) is pivoting its ads business toward AI, positioning the Vector ad platform as its primary growth driver. The company is sunsetting the legacy ironSource Ads Network and is exploring a sale of its Supersonic publishing unit. Management expects Vector to reach a billion dollar annual run rate, with recent trends supporting upgrades to company guidance.

Unity Software enters this shift with a share price of $21.62 and a mixed return profile, including a 51.1% decline year to date but a 12.4% gain over the past year. For investors, that combination of sharp drawdown and more recent recovery sets the backdrop for assessing how meaningful the AI-led ads focus could be to the NYSE:U story.

The move toward Vector and away from ironSource Ads and possibly Supersonic changes where Unity’s growth and risks are concentrated. The rest of this article looks at what this transition could mean for revenue mix and margins, and how you might think about Unity within a portfolio that already has exposure to advertising and AI themes.

Stay updated on the most important news stories for Unity Software by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Unity Software.

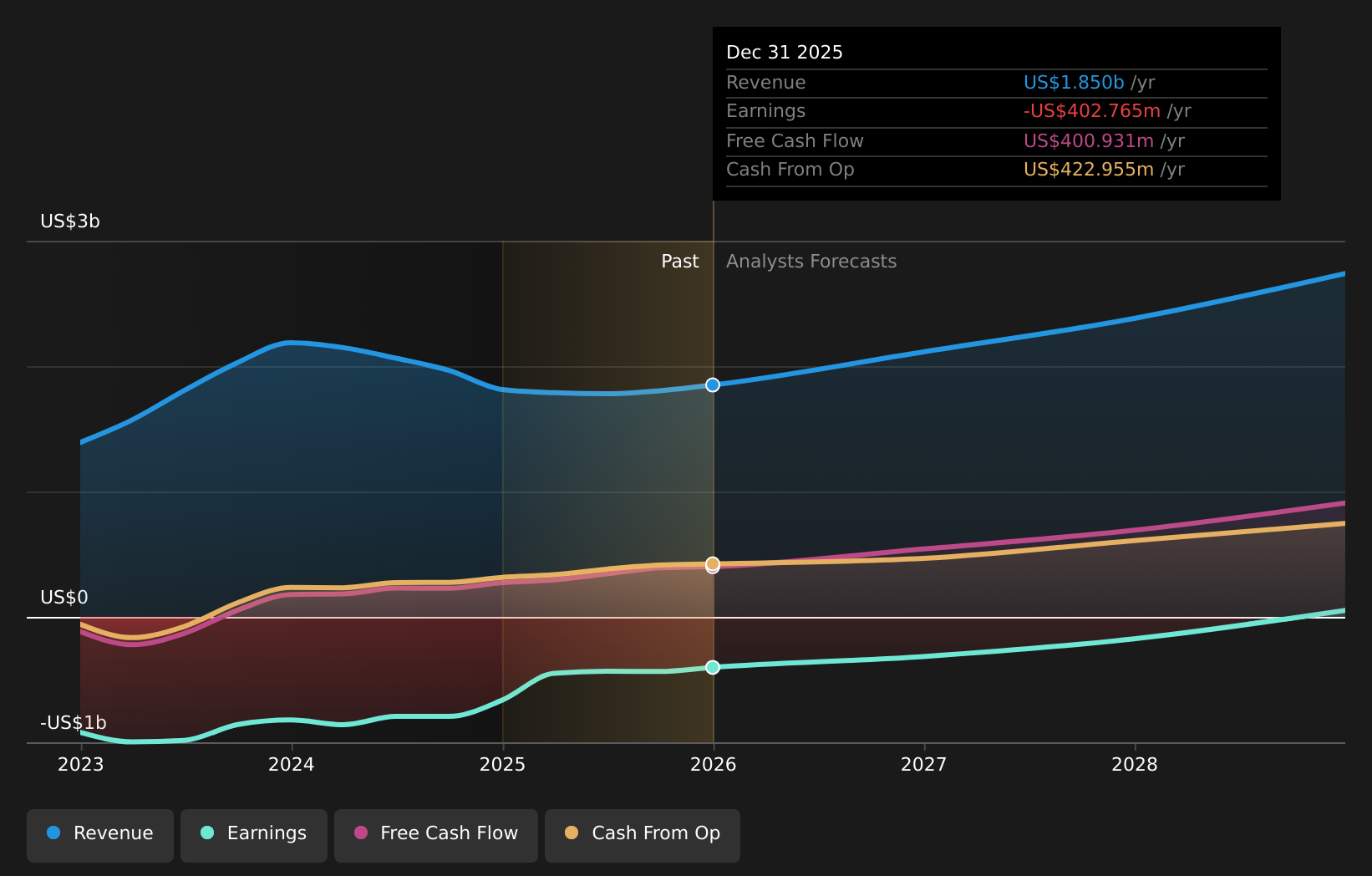

NYSE:U Earnings & Revenue Growth as at Apr 2026

NYSE:U Earnings & Revenue Growth as at Apr 2026

2 things going right for Unity Software that this headline doesn’t cover.

Unity’s push toward the Vector AI-powered ad platform, combined with the exit from the ironSource Ads Network and potential Supersonic sale, concentrates its growth thesis in higher automation and data driven advertising. The extended multi year VR agreement with Meta pulls in the other side of the story, where Unity’s engine and tools remain tightly linked to a large hardware ecosystem. Together, these moves shift Unity closer to being a focused tools and ads platform that leans on AI models trained on in engine and runtime data, rather than running a broad mix of ad and publishing assets with different risk profiles. For you as an investor, the key question is whether Unity can execute this pivot while keeping large customers engaged and monetizing that data advantage faster than costs rise.

How This Fits Into The Unity Software Narrative The emphasis on Vector and deeper Meta VR alignment supports the narrative that AI-driven products and immersive content tools can expand Unity’s addressable market and support more stable, recurring revenue from both Create and Grow segments. Shutting down a legacy ad network and exploring a publishing sale tests the assumption that diversification alone reduces volatility, because Unity is giving up some revenue streams in order to prioritize higher conviction areas. The extended Meta agreement and the specific focus on monetizing runtime data through Vector do not appear fully reflected in a general AI and subscription growth narrative, which may understate how tied Unity’s fortunes are to a few large partners.

Knowing what a company is worth starts with understanding its story.

Check out one of the top narratives in the Simply Wall St Community for Unity Software to help decide what it’s worth to you.

The Risks and Rewards Investors Should Consider ⚠️ Execution risk in retiring ironSource Ads and potentially selling Supersonic, which could disrupt existing advertiser and developer relationships if the transition to Vector is slower or more complex than planned. ⚠️ Competitive pressure from large platforms such as Alphabet, Apple and Tencent in mobile ads, and from engines such as Epic’s Unreal, which may limit Unity’s ability to differentiate its AI-powered ad tools and maintain pricing. 🎁 Vector’s track record of several quarters of strong quarter on quarter growth suggests Unity may be gaining traction with performance focused advertisers that value AI driven optimization and access to in game behavioral data. 🎁 The extended Meta VR partnership reinforces Unity’s role at the center of VR content creation, which can support higher usage of Create tools and provide more data inputs for ad and monetization products over time. What To Watch Going Forward

From here, it makes sense to watch how quickly revenue from Vector offsets any drop off from ironSource and Supersonic, and whether management continues to raise or maintain guidance tied to this pivot. Monitor updates around the Meta VR relationship and any new major partners that validate Unity’s tools in non gaming uses. Competitive comments from peers such as Epic Games, Roblox, or large ad networks can also give clues about how differentiated Unity’s AI-led ads offering really is.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for Unity Software, head to the

community page for Unity Software to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com