(Bloomberg) — China’s economic growth rebounded more than expected in the first quarter, suggesting limited spillovers so far from the war in Iran but revealing few signs of turnaround in weak consumer spending.

Powered by strong manufacturing and exports, gross domestic product expanded 5% from a year ago, the fastest in three quarters, according to a statement from the National Bureau of Statistics on Thursday. GDP also saw the quickest sequential growth since the final three months of 2024, with a gain of 1.3% from the prior quarter on a seasonally adjusted non-annualized basis.

Highlighting the divergence between major parts of the economy, industrial output grew a more-than-forecast 5.7% in March from a year ago. By contrast, retail sales fell short of expectations with an increase of 1.7%, down from a 2.8% expansion in the first two months.

“The manufacturing side of the economy remains resilient and is still a key near-term growth anchor,” said Hao Zhou, chief economist at Guotai Junan International in Hong Kong. “Looking ahead, China’s macro agenda is likely to center on two intertwined priorities: reflation and boosting domestic demand.”

The war, now in its seventh week, has yet to threaten the momentum that built at the start of 2026, thanks in part to China’s moves in past years to strengthen energy security and insulate its economy from global turmoil. Years of deflationary pressure have also blunted the potential for an immediate impact on consumer prices from higher oil costs.

Despite little evidence of improvement in domestic demand, the latest official assessment of the economy will likely reduce the urgency for additional stimulus, especially after Beijing adopted a more flexible approach toward growth by lowering its GDP goal to a range of 4.5% to 5% — the lowest since 1991.

The upside surprise prompted Deutsche Bank AG and Barclays Plc to upgrade their forecasts for real growth in China’s GDP this year to 4.9% and 4.6%, respectively.

The GDP expansion pace stands out especially because growth was particularly strong a year ago due to a rush of exports before US tariffs kicked in. That created a high base of comparison, and prompted Mao Shengyong, deputy commissioner at the NBS, to describe the result as “precious” given the “severe” external environment.

“Overall, the main macro indicators rebounded in the first quarter, and new drivers are growing rapidly,” Mao said at a briefing in Beijing. “But we also need to see that the external situation is more complex and volatile, and the imbalance between strong domestic supply and weak demand is still stark.”

Rapid growth in tech sectors continued to drive industrial production as well as exports, which surged 15% in the first quarter from a year ago.

High-tech output expanded 12.5% in the first quarter, much faster than the 6.4% gain in manufacturing as a whole. Industrial robots and integrated circuits surged 33% and 24% respectively.

Overall, manufacturing contributed nearly a third of economic growth in the quarter, according to Mao.

What Bloomberg Economics Says …

“The good news in China’s GDP report — a sharp acceleration in growth marks a strong start to the year. Less good — it’s on a shaky foundation. Domestic drivers sputtered, with retail sales and investment slowing.”

— Chang Shu and David Qu; click here to read the full report

In a sign of ripples from the energy crisis stemming from the war in Iran, the output of refined oil fell 2.2% in March. That showed refiners cut run rates to conserve supplies snarled by conflict in the Middle East.

Contrasting with the strong gains made by factories, consumer spending and private investment continued to cool, resulting in an increasingly lopsided economy. The surveyed urban jobless rate unexpectedly climbed in March to 5.4%, the highest in a year.

Household spending per capita only grew 2.6% in price-adjusted terms, its worst pace of year-to-date expansion since the final quarter of 2022. Wage incomes also increased the slowest since late 2022.

Fixed-asset investment gained 1.7% in the first three months of the year, slightly weaker than the 1.8% increase in the first two months. Property investment slumped 11.2%. Private investment declined in the period for the first time on record, outside the pandemic year of 2020.

“It’s too soon to call China out of the doldrums,” said Carlos Casanova, senior Asia economist at Union Bancaire Privee in Hong Kong. “Weakness in the private sector is feeding into rising unemployment — an increasingly sensitive political issue likely to prompt targeted stimulus, especially given the private sector’s outsized role in job creation.”

A major drag on retail sales came from purchases of cars, furniture and home appliances, which led declines in March by dropping 12%, 9% and 5%, respectively. That reflected a diminishing impact of the government’s trade-in subsidies, a program that was scaled back for cars this year.

The Communist Party’s ruling Politburo is set to hold a meeting focusing on the economy at the end of April, where it will provide clues about future policies.

Some economists are expecting only targeted policy help. Officials will likely hold off on major stimulus until the economy encounters a major speed bump.

“We expect the policymakers to focus on implementing existing policy easing measures,” said Xiaojia Zhi, an economist at Credit Agricole CIB. “They will likely introduce targeted fiscal support and relief measures to manage the energy price shocks and alleviate cost pressures.”

Zhi also expects public spending on strategic investment projects to accelerate, since the Iran conflict will reinforce China’s determination to strengthen national security. This would also help cushion any near-term growth pressures if external demand deteriorates, she added.

A rising number of economists is forecasting the People’s Bank of China won’t cut interest rates this year, because the oil shock pushed up inflation expectations.

Still, Bloomberg Economics predicts the PBOC will loosen policy this quarter by lowering the reserve requirement ratio by 25 basis points, followed by additional fiscal stimulus from the government later in the year, in an effort to “turn up support” and maintain China’s easing stance.

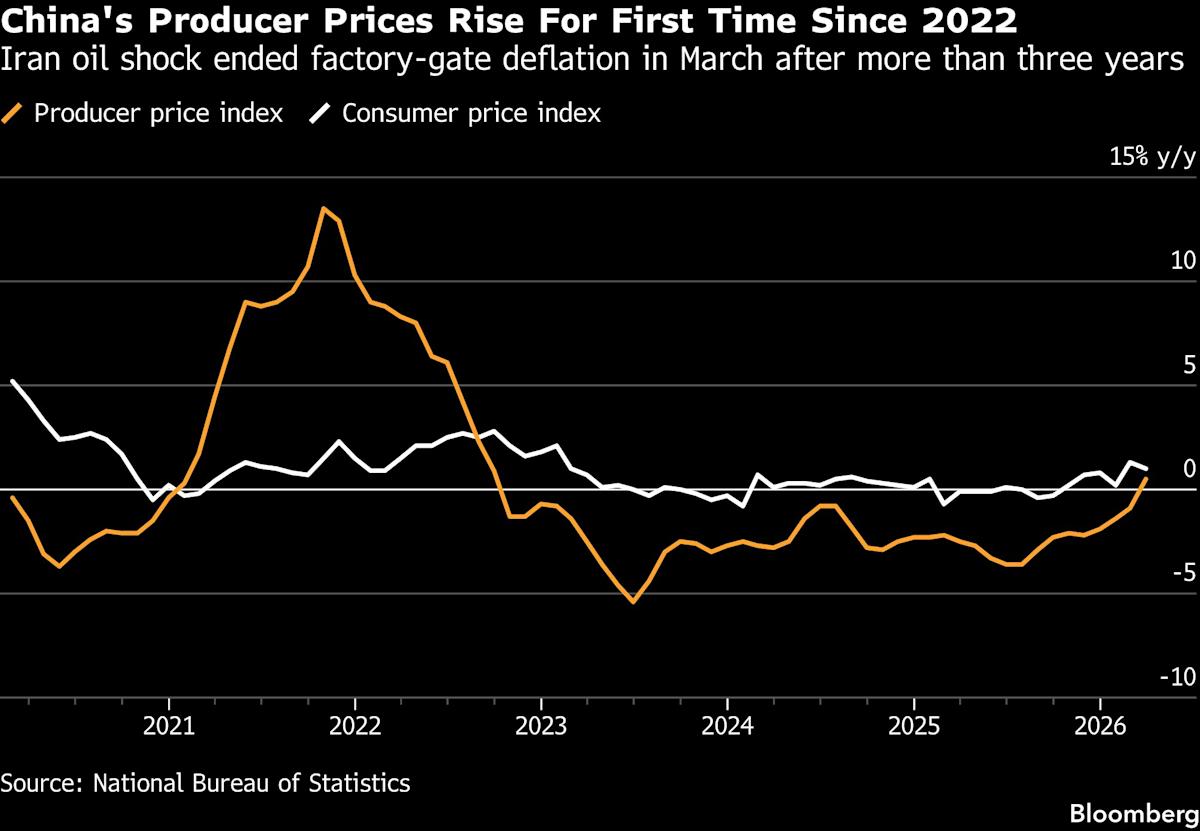

Economy-wide prices didn’t rise in the first quarter as some analysts had expected, even though their decline narrowed as a result of the oil shock. Producer prices turned positive in March for the first time after three and a half years of deflation.

The GDP deflator, a measure of price changes across the economy, fell 0.1% in the first quarter, according to calculations by Bloomberg based on official nominal and real growth numbers. That’s the 12th straight quarter of decline.

But as Chinese companies emerge from deflation, Deutsche Bank’s Yi Xiong and Deyun Ou expect the benefits from a “sustained improvement” in their sales and profits to flow through to the economy. The German lender’s upgraded estimate for this year’s real GDP implies its forecast for nominal economic growth rises to 6.5% — which would be its highest level since 2022.

“Today’s first-quarter GDP release delivered another important message: this is not stagflation, as China’s economy is also expanding in quantity amidst price increases,” the Deutsche Bank economists said. “Higher nominal growth could improve Chinese corporates’ revenue and profitability, further supporting the recovery of investment and household income.”

–With assistance from Jacob Gu, Jing Li and Qianwei Zhang.

(Updates with forecast upgrades in seventh paragraph, adds economist comments in final two.)

More stories like this are available on bloomberg.com

©2026 Bloomberg L.P.