(Bloomberg) — Bond investors have ridden a profitable playbook this year to score big wins on Federal Reserve interest-rate cuts and tumbling short-term US yields.

Now, they’re ready to look out a little longer on the Treasury curve.

Most Read from Bloomberg

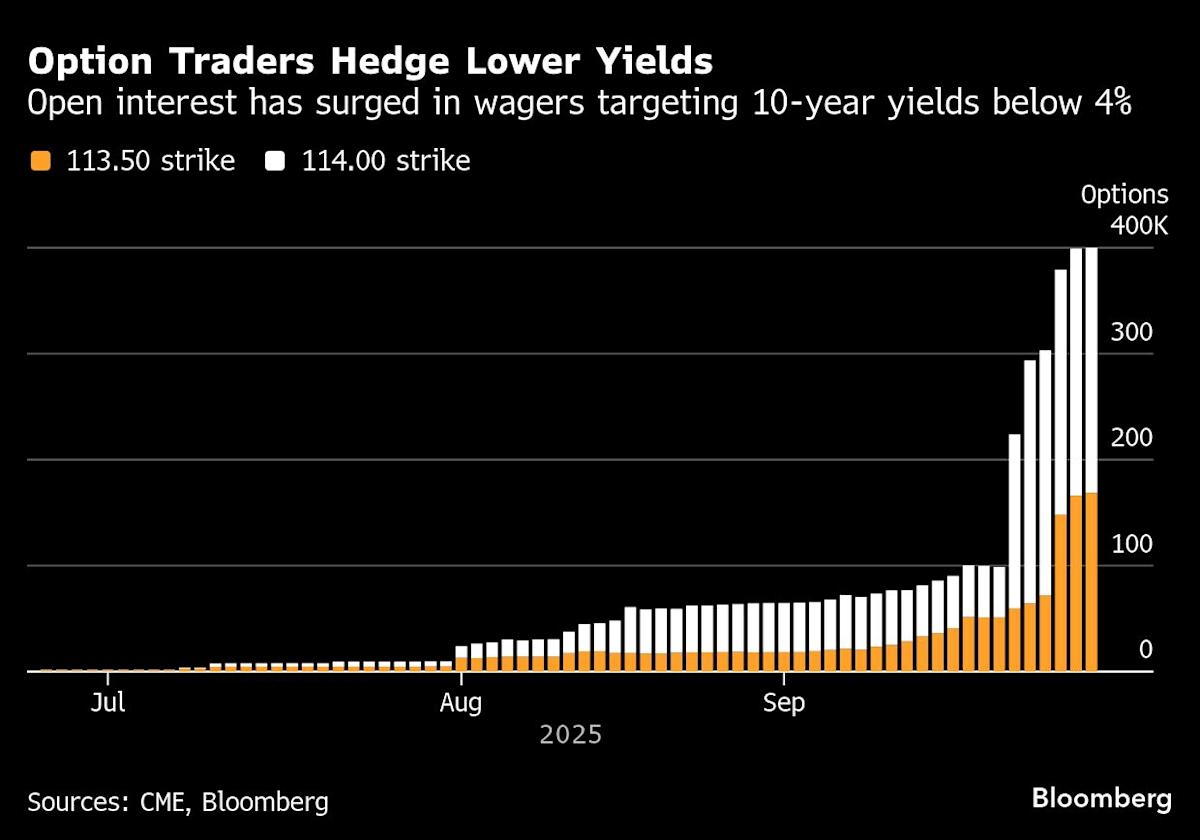

A cluster of bullish option trades has emerged over the past two weeks, wagering that a rally in 10-year US Treasuries will drive the benchmark below 4% for the first time since April. Pacific Investment Management Co. is advising clients to lock in yields while they remain attractive, just as JPMorgan Asset Management and TD Securities notice clients moving out of short-term notes and into longer, higher-yielding maturities.

“There’s still a lot of caution in markets not to jump the gun, but they are dipping their toes in,” said Gennadiy Goldberg, head of US interest rates strategy at TD Securities. “It is good to lock in these higher rates for longer, but very, very cautiously.”

Taken together, the momentum — enhanced somewhat by reaction to the US government shutdown — pushed down 10-year Treasury yields by 0.05 percentage point in the past week to near 4.1%, the lower end of the recent trading range. Thirty-year yields, seen as riskier though still benefiting from the trend, also edged down to about 4.7%.

“The bond market represents good value,” said Warren Pierson, who oversees $180 billion in fixed-income assets as co-chief investment officer at Baird Funds. “For retirees in general, pension plans, those levels of interest rates are pretty good.”

Market Shift

The renewed attention on longer-term debt is a switch for investors who have spent much of the year betting successfully that the gap between US short- and long-term yields would widen.

The so-called curve steepener paid off handsomely as expectations for renewed Fed rate cuts sent policy-sensitive short-term yields plunging, while the long end remained more elevated in part on fiscal and political concerns. The dynamics also helped the bond market turn in its best year-to-date performance in five years through September, according to a Bloomberg index.

More recently, the trade lost steam as long bonds no longer underperformed. The gap between US five- and 30-year bonds has shrunk to roughly 1 percentage point, after reaching a four-year high of about 1.26 percentage points in early September.

Investors cite a few catalysts for the shift. For one, it makes sense to take some profits on the steepener after its winning run. But also, with shorter-term securities already pricing in another percentage point of Fed cuts over the next year amid increasing signs of labor market frailty, some investors are looking further out to pick up more yield.

Adding to economic worries, the federal government shutdown threatens to stretch into a second week, causing a cascade of delays to economic indicators and potentially contributing to further job losses. And unlike past similar instances, President Donald Trump this time has threatened “a lot” of firings of federal workers, amping up the risks to the economy.

For Brij Khurana, portfolio manager at Wellington Management, this backdrop sets up a scenario for long-term bonds to outperform shorter-dated notes. That’s because in his view, the long end hasn’t adequately priced in the risk of a sharp slowdown.

“Maybe the front end is priced for it, but not the back end,” he said.

On top of all of this, prolonged shutdowns have historically boosted long-dated Treasuries, data from Citigroup Inc. strategists shows.

What Bloomberg strategists say…

The steepener, while taking a break Thursday, has a fresh catalyst in the US government shutdown — which risks denting growth and higher unemployment. Signs inflation within various economic data sets indicate pricing power at companies has declined can also support the trade.

Meanwhile, supply factors also support the trade with heavy issuance in the week ahead…November’s US Treasury refunding will also start to enter the conversation. With debt, deficits and the cost to service bonds still a concern, investors are likely to demand more risk premium further out the curve, meaning spreads between active Treasuries can steepen.

-Alyce Andres, US FX/Rates Strategist, Markets Live

Some investors aren’t ready to abandon the steepener trade. On Friday, DoubleLine Capital released a report arguing that the strategy has plenty of room to run, with the gridlock in Washington only lending support to the trend.

The combination of Fed cuts, sticky inflation and breakneck government borrowing will keep pushing the extra yield investors demand to hold long-term Treasuries higher in the coming quarters, according to Bill Campbell, global sovereign debt portfolio manager at the firm.

“Even in a downside economic shock, I still think the curve will steepen,” Campbell said in an interview on Thursday. “We have increasing fiscal deficits, rising uncertainty about inflation, rising questions about US policy — anywhere from Fed independence to what the tariff and trade outlook for the United States is going to look like.”

Guggenheim Managers Inc. Chief Investment Officer Anne Walsh also remains an adherent, as does Vineer Bhansali, founder of the Newport Beach, California-based asset-management firm LongTail Alpha. For Bhansali, the steepener trade is a “multi-year trade” that is “only halfway done.”

Auction Test

A critical test of investor demand will come at next week’s Treasury bond auctions, including the sales of $39 billions of 10-year notes and $22 billion of 30-year bonds.

For Priya Misra, portfolio manager at JPMorgan Investment Management, moving out to the 10-year sector makes sense in part because these securities could work as a hedge against risky assets at a time when stocks and credit market valuations are at historical highs.

The correlation between US 10-year notes and stocks has reverted to its traditional negative relationship after turning positive for the past two years. That means when stocks decline, bond prices will go higher, which helps lower the volatility of a diversified portfolio.

“I think people see that cross-asset correlations are back with the Fed’s focus on the labor market,” said Misra. “Given the high valuations in equities, still above 4% on the 10-year and the prospect of lower rates in the front end, moving out the curve seems prudent from a risk-reward standpoint.”

What to Watch

–With assistance from Edward Bolingbroke.

Most Read from Bloomberg Businessweek

©2025 Bloomberg L.P.