Canadian Highlights

January’s jobs report surprised with a decline in the unemployment rate. However, the details paint a less positive picture, with the economy losing jobs, and a tighter job market driven by an even larger decline in the labour force.

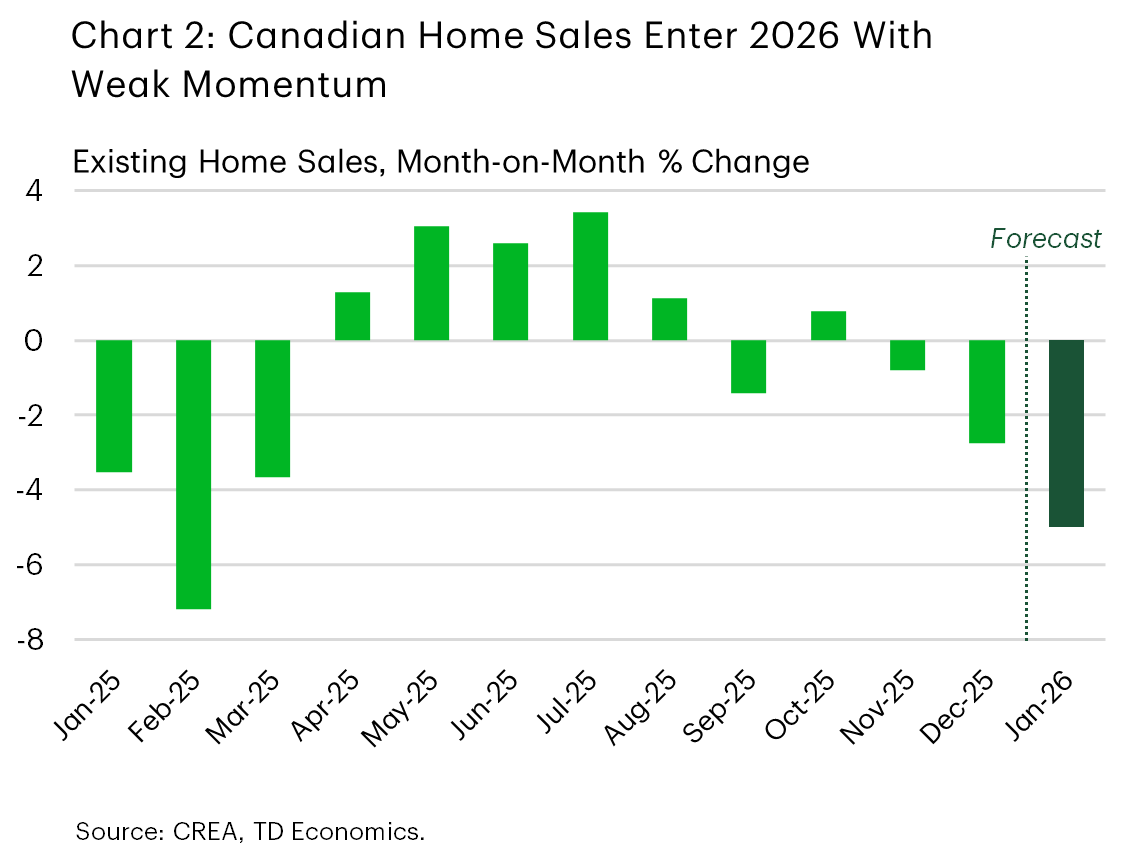

Preliminary home sales and price growth data for January sent a chill through key Canadian markets, putting the housing market on weak footing to start the year.

Prime Minister Carney introduced a new plan to reduce emissions from transportation and boost Canada’s EV industry.

U.S. Highlights

Congress passed legislation to fund most of the government through September, with a 2-week continuing resolution used for the Department of Homeland Security.

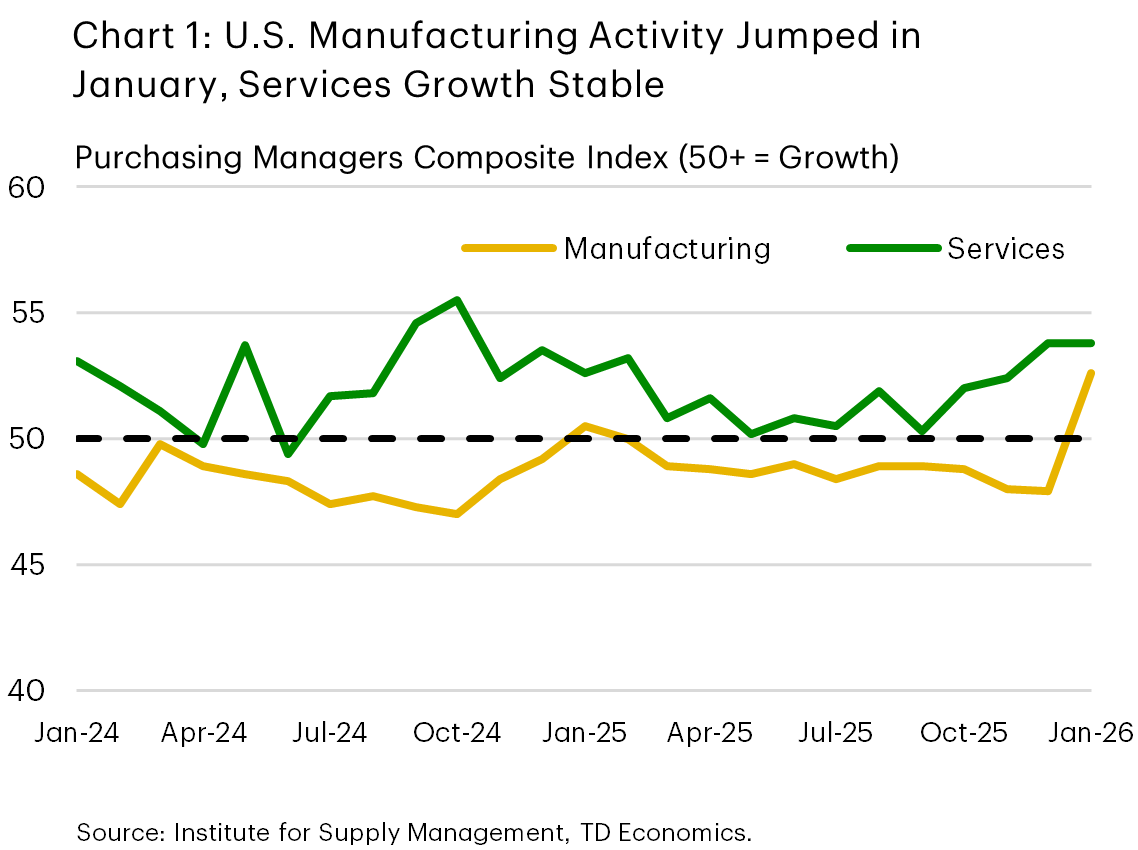

The ISM Purchasing Managers Index reports showed solid growth in manufacturing and services activity in January, suggesting the economy entered 2026 on a solid footing.

January data releases for employment and inflation next week will be closely monitored for potential risks related to the Fed’s dual mandate.

Canada – Labour Market Sending Mixed Signals

Precious metals rebounded early in the week, briefly boosting the TSX before broader market caution pushed the index lower, finishing roughly flat on the week. Canadian government bond yields were less volatile and ended the week mostly unchanged. Meanwhile, the US dollar continued to strengthen, causing the Loonie to fall to 73 cents/USD. The depreciation was limited as Bank of Canada Governor Tiff Macklem dismissed further rate cuts in his first public speech of 2026.

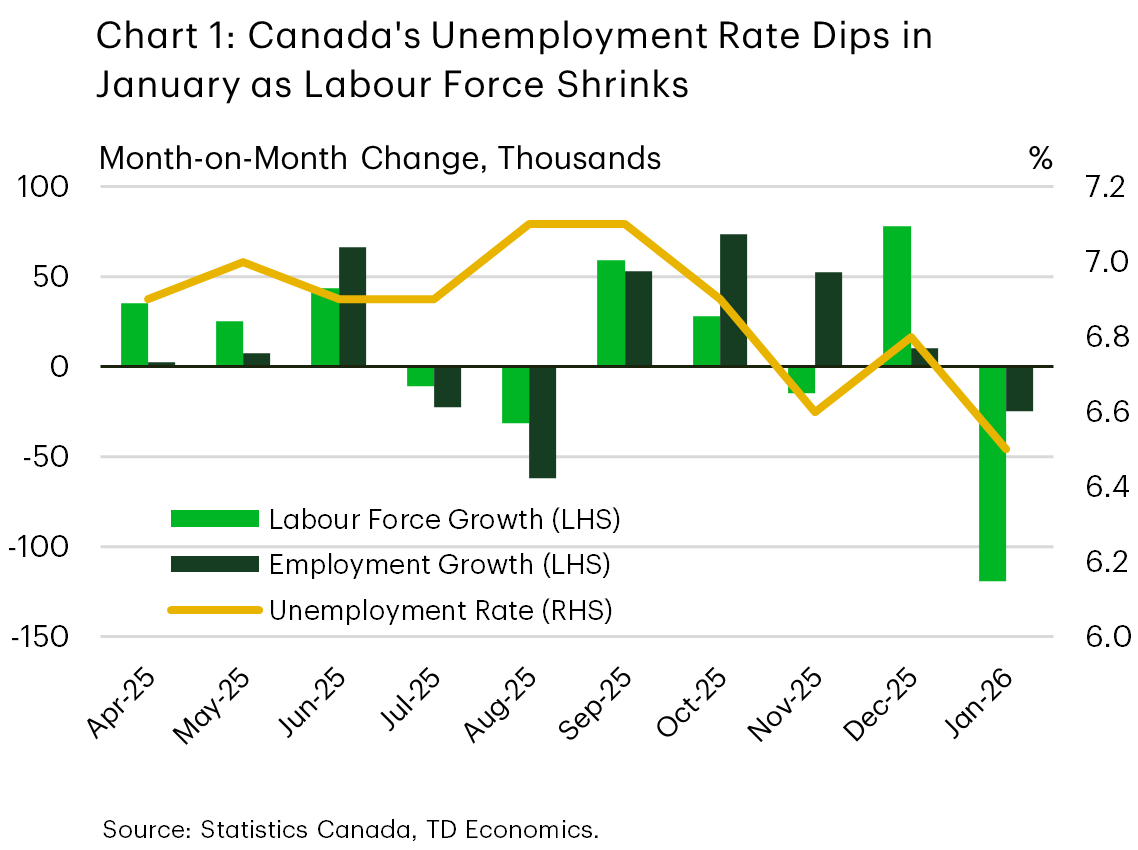

The first jobs report for 2026 was the main economic event this week. January’s jobs numbers were full of surprises. The unemployment rate dropped three ticks to 6.5%, reversing December’s increase. This occurred despite the economy losing 25k jobs in January, since the labour force contracted by a larger 120k people. Large swings in the month-to-month labour force survey numbers are common, but January was the biggest drop in the labour force since early-2021 (Chart 1). With Canada’s population projected to contract this year, the unemployment rate can continue to fall even if Canada is losing jobs.

Zooming out, the Labour Force Survey has notably outperformed its companion payrolls survey, which has given much weaker signals about the health of Canada’s job market. An objective evaluation of both readings likely puts the actual health of the labour market somewhere in the middle. The labour market entered this year on a soft note, but the gradual decline in the unemployment rate suggests that the situation is improving. We recently released a report that combs through several other job market indicators tracked by the Bank of Canada (BoC) to help make sense of some of this discrepancy.

Beyond this week’s labour market report, we have limited data to inform Canada’s early-year economic performance. Preliminary housing figures for January showed double-digit home sales declines in Toronto and Greater Vancouver, with Calgary seeing a slight increase (Chart 2). A wave of new listings eased market conditions, while average prices fell 1–2% month-over-month, continuing recent softness. Overall, Canada’s housing market is set for a subdued year, mirroring our view for tepid overall growth in Canada in 2026. Consumer spending will likely cool and investment remain weak, though government expenditures and improved exports should help offset these trends. We forecast real GDP growth to slow to about 1.0% this year before moderately accelerating to trend-like growth by 2027.

The federal government grabbed attention again this week with a shift in policies related to electric vehicles (EVs). On February 5th, Prime Minister Carney introduced a new plan to reduce emissions from transportation and boost Canada’s EV industry. The main points of the strategy feature stricter emissions rules for vehicles made between 2027 and 2032, aiming for electric vehicles to make up 75% of sales. Additionally, the plan includes a $2.3 billion rebate program for EVs and allocates $1.5 billion toward expanding EV charging stations. Full details can be found in our coverage here.

U.S. – Shutdown Ended, Labor Market Concerns Linger

The first week of February was eventful on several fronts. The partial government shutdown, which began over the weekend, ended on Tuesday as the House managed to pass the requisite spending bills. Funding for the Department of Homeland Security was provided by a 2-week continuing resolution – which expires on February 13th – as both parties continue to negotiate the details of the department’s funding. Despite the positive news, financial markets had a tough week, with the S&P 500 down 0.7% as of the time of writing, owing in part to investor concerns regarding the impact of AI on existing business models.

On the economic data front, the ISM Purchasing Manager Index (PMI) reports showed a substantial uptick in manufacturing activity in January (Chart 1). However, survey respondents noted that this was at least partly owing to post-holiday inventory replenishment and front-loading activity ahead of potential new tariffs on Europe and other nations. The services PMI also pointed to growth in activity in January, although the acceleration recorded in recent months eased. On aggregate, these reports suggest economic activity remained on a solid footing to start the new year.

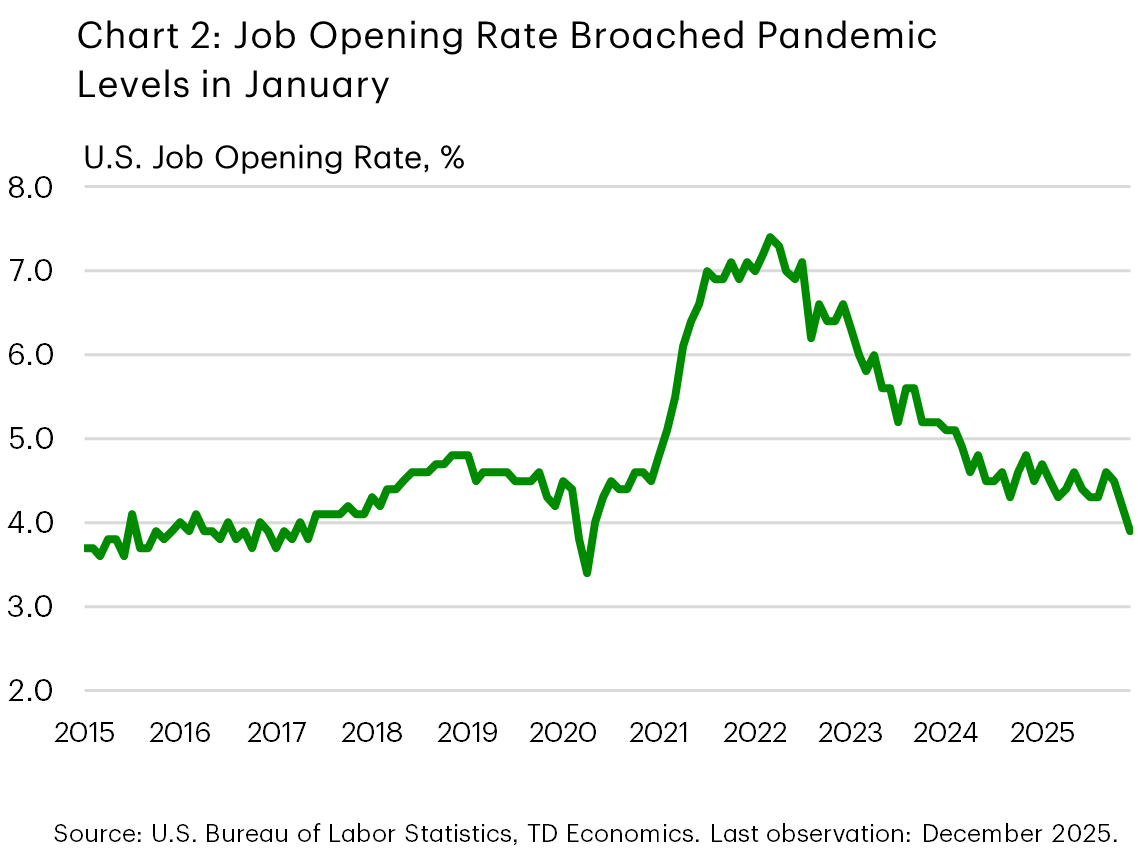

Our ability to see if this translated to the labor market in January was delayed by a week owing to the shutdown, with the Bureau of Labor Statistics pushing the release of the employment report to next Wednesday (originally scheduled for February 6th). However, we did receive the Job Opening & Labor Turnover report on Thursday, which showed a sharp drop in the job opening rate in December (Chart 2), particularly among white-collar sectors. The slowdown in the labor market has been a key concern for the Federal Reserve and provided the main rationale for the three “risk management” rate cuts implemented by the FOMC last year. Next week’s employment report will be watched closely, with a healthy addition of 70k jobs currently expected by consensus forecasters.

Although the next Fed meeting is still six weeks away, the Fed officials we heard from this week – including Atlanta Fed President Bostic, Richmond Fed President Barkin, and Fed Governor Lisa Cook – were broadly consistent in their view of the balance of risks between the Fed’s dual mandate. Most believed that risks to the labor market have eased, and that the persistent deviation of inflation from the 2% target is currently the greater risk. All speakers this week stated that patience was warranted to ensure that recent disinflation progress was sustained, but Governor Cook also noted that the FOMC was cognizant of the lingering risks to the labor market and would respond accordingly to the evolving risk environment.

Core CPI inflation sat at 2.6% in December, but price growth momentum dropped materially in the aftermath of the October government shutdown disruption. Further information will be available with next week’s CPI report for January, which is expected to show a modest drop in core CPI to 2.5%.