Demand for Collapsible Rigid Containers in United Kingdom

The demand for collapsible rigid containers in the United Kingdom is gaining consistent momentum as industries reassess how packaging assets influence logistics efficiency, storage economics, and sustainability outcomes. Unlike disposable packaging formats, collapsible rigid containers offer long-term value by balancing durability with space efficiency.

Between 2026 and 2036, the market is expected to evolve steadily rather than explosively, reflecting its role as a utility-driven packaging solution embedded within supply chain operations rather than a trend-led product category.

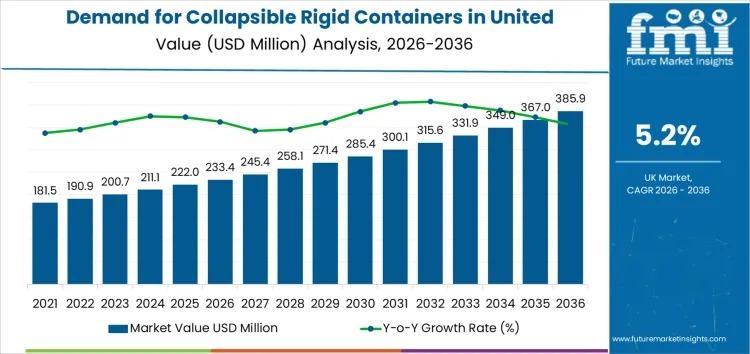

The UK market is forecast to expand from USD 233.4 million in 2026 to USD 385.9 million by 2036, registering a CAGR of 5.2%, supported by widespread adoption across logistics, manufacturing, retail, and food distribution ecosystems.

Discover Growth Opportunities in the Market – Get Your Sample Report Now

https://www.futuremarketinsights.com/reports/sample/rep-gb-31321

Meaning and Market Overview

Collapsible rigid containers are reusable packaging systems designed to maintain structural strength during use while folding flat when empty. This dual functionality allows businesses to reduce return transport costs, minimize storage footprints, and improve asset utilization. In the UK, these containers are widely deployed in closed-loop supply chains where returnable packaging is economically viable and operationally essential.

Market value creation is less about volume throughput and more about lifecycle efficiency. Buyers evaluate containers based on load-bearing capacity, foldability performance, durability over multiple cycles, and compatibility with automated handling systems.

Market Outlook Through 2036

The outlook for collapsible rigid containers in the United Kingdom remains stable and predictable. Growth is expected to be driven by gradual penetration across industries rather than short-term spikes in demand. As companies build container fleets and integrate collapsible designs into standardized logistics processes, replacement cycles and incremental fleet expansion will sustain long-term value accumulation.

Key characteristics shaping the outlook include:

• Strong alignment with reusable transit packaging strategies

• Low exposure to demand volatility compared to consumable packaging

• Consistent replacement demand driven by wear-and-tear cycles

• Long-term contracts favoring established suppliers

Growth and Demand Drivers

Demand growth is anchored in operational efficiency rather than aesthetic or branding considerations. UK manufacturers and logistics operators increasingly prioritize total cost of ownership when evaluating packaging investments.

Key drivers include:

• Rising logistics costs, encouraging reduced empty-return volumes

• Warehouse space constraints, especially in high-density distribution hubs

• Expansion of returnable packaging programs across automotive, electronics, and retail

• Sustainability commitments, replacing single-use packaging with durable systems

• Improved asset control, reducing loss and dependency on disposable alternatives

Historically, rigid containers were used primarily for static storage or long-haul transport. The shift toward collapsible designs reflects broader supply chain restructuring in response to fluctuating freight rates and storage limitations.

Key Market Segments

By Material Type

Plastic dominates the UK market, accounting for 53.4% of total demand. Its popularity stems from its balance of strength, weight efficiency, and resistance to corrosion.

Plastic containers

• Lightweight and easy to handle

• Suitable for food, retail, and general logistics

• Cost-effective across multiple use cycles

Metal containers

• Preferred for heavy-duty and bulk applications

• Common in chemicals, pharmaceuticals, and agriculture

• Higher upfront cost but superior durability

Other materials

• Composite pallet boxes and specialty containers

• Designed for niche or regulated applications

By Product Type

Crates represent the largest product segment with 42.8% market share, driven by their versatility and compatibility with standard handling systems.

• Crates for retail, food, and warehouse operations

• Foldable IBCs for bulk liquids and powders

• Pallet boxes for industrial-scale storage

• Jerry cans for smaller-volume liquid transport

Market Dynamics and Trends

The market is shaped by supply chain optimization goals rather than discretionary purchasing behavior. Procurement decisions are closely tied to manufacturing output, seasonal activity, and warehouse throughput requirements.

Key trends include:

• Integration of RFID and barcode tracking to reduce asset loss

• Standardized container pooling across logistics networks

• Modular container designs adaptable to multiple SKUs

• Compatibility with automation, conveyors, and robotics

• Circular economy alignment, prioritizing reuse over disposal

Logistics service providers increasingly collaborate with manufacturers to standardize container formats, lowering total system costs and improving asset visibility.

Regional Demand Outlook

England leads the UK market, supported by dense logistics infrastructure and manufacturing clusters. However, demand growth is visible across all regions.

• England: CAGR 5.7%

• Scotland: CAGR 5.1%

• Wales: CAGR 4.7%

• Northern Ireland: CAGR 4.1%

While England remains dominant, growth in Scotland and Wales reflects expanding retail logistics and sustainability-led procurement strategies. Northern Ireland, though smaller in scale, shows steady adoption driven by cost efficiency and storage optimization.

Get the Complete Story-Read More About Our Latest Report!

https://www.futuremarketinsights.com/reports/united-kingdom-collapsible-rigid-containers-market

Competitive Landscape

Competition in the UK collapsible rigid containers market is shaped by documented performance metrics rather than branding alone. Buyers assess suppliers based on load ratings, lifecycle durability, fold-flat efficiency, and integration with existing storage systems.

Key competitive characteristics include:

• Emphasis on technical documentation and compliance

• Focus on long-term supply reliability and lead times

• Alignment with automation and warehouse systems

• Strong preference for suppliers supporting closed-loop logistics

Leading players operating in the United Kingdom include:

• Brambles Limited

• Supreme Industries Limited

• Schoeller Allibert Services B.V.

• DS Smith plc

• SSI Schäfer AG

Larger players benefit from economies of scale, allowing better pricing control and innovation investment, while smaller suppliers face margin pressure as buyers consolidate sourcing.

Why FMI: https://www.futuremarketinsights.com/why-fmi

Have a Look at Related Research Reports on the Packaging Domain:

Paint Cans Market https://www.futuremarketinsights.com/reports/paint-cans-market

Tarpaulin Sheets Market https://www.futuremarketinsights.com/reports/tarpaulin-sheets-market

Industrial Electronics Packaging Market https://www.futuremarketinsights.com/reports/industrial-electronics-packaging-market

Contact Us:

Future Market Insights Inc.

Christiana Corporate, 200 Continental Drive,

Suite 401, Newark, Delaware – 19713, USA

T: +1-347-918-3531

For Sales Enquiries: sales@futuremarketinsights.com

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.

This release was published on openPR.