BNY’s John Bailer explains why the real money in artificial intelligence will be made by companies using the technology, not those building the infrastructure.

The artificial intelligence (AI) boom is creating a bubble in infrastructure spending that will eventually benefit a very different set of companies from those currently dominating markets, according to John Bailer, manager of the BNY Mellon US Equity Income fund.

“I’m a big believer that artificial intelligence is transforming the world,” he said. “One of the reasons it transforms the world is because everybody believes in it. They invest in it. They borrow money to invest more in that technology. You just invest too much, and then prices collapse because there’s too much competition.”

Bailer covered telecoms during the dot-com bubble and watched fibre-optic infrastructure spending create fortunes for equipment makers before collapsing. The real winners were companies like Amazon, Google and Facebook that used the infrastructure to build businesses.

“I think the same thing is going to happen now,” he said.

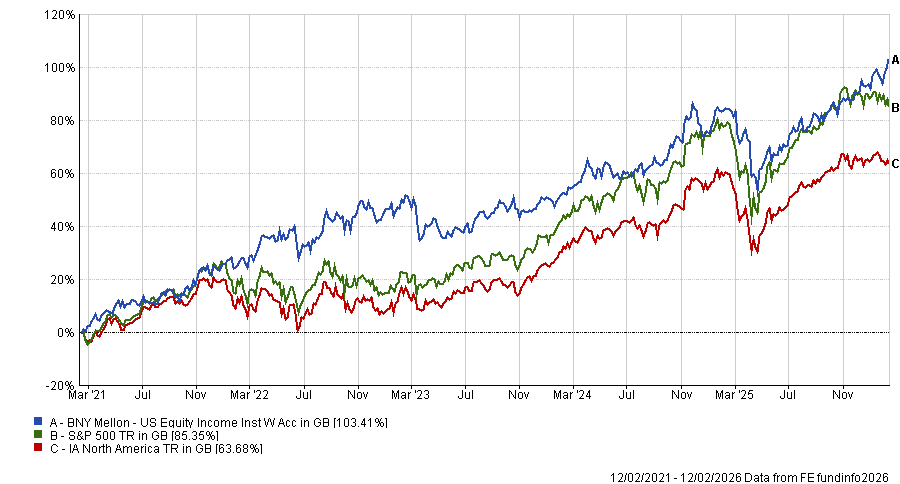

The £1.2bn fund has attracted significant inflows since delivering a 4% return in 2022 when the S&P 500 fell 18%. Early signs of rotation are already visible. The fund’s top seven holdings are up 8% this year while the Magnificent Seven as a group are down 4%.

Below, Bailer explains why productivity beneficiaries of AI will outperform infrastructure plays and how financials are positioned to gain without disruption risk.

Performance of fund against sector and benchmark over 5yrs

Source: FE Analytics

What’s the philosophy behind this fund?

You need to combine value with business momentum and quality fundamentals – you can’t just focus on one factor. If you focus on one factor, your performance tends to be very volatile because factors go in and out of favour.

This three-circle approach means we’re looking for companies that look like they have intrinsic value but tend to be out of favour. What the momentum circle does is focus on the stocks that are down but maybe something is happening that’s turning their fortunes around. That helps us avoid the value trap.

This fund is benchmarked to the S&P 500, but our tracking is much closer to the Russell 1000 Value. If we can beat that value index, we feel like we’re doing our job. Over long periods of time, our belief is value can outperform growth. That hasn’t been the case for the past 16 years.

Why do you keep the S&P 500 as your benchmark if it looks expensive?

The majority of our funds benchmark the Russell 1000 Value. It’s only the funds we sell outside the US that use the S&P 500. We thought outside the US it was more about investors looking at beating the overall US market.

I made this very clear to our clients: we’re going to track much closer to the Russell 1000 Value. Ideally we’d like to beat the S&P 500 as well.

The S&P 500 multiple looks relatively expensive to an income investor. It looks relatively expensive versus small-cap stocks in the US, versus value stocks and versus stocks outside the US.

There are plenty of stocks within the US market that we think are incredibly attractive. They just tend to be a little bit on the smaller end of large-cap. That’s where we’re finding real opportunities.

What’s your view on the S&P 500?

There’s been a ton of spending, much more than I would have thought, on data centre infrastructure. It’s just hard for me to see that even growing from 2026 levels.

We saw this back in the tech bubble with fibre deployment. I covered telecom stocks back then. This is how bubbles get created in the market.

We’re not invested in any of the hyperscalers. I think we’re going to move from all the infrastructure beneficiaries to the companies that utilise AI and get productivity benefits from AI. Those tend to be the older type of companies.

Which sectors that you invest in are best positioned for AI gains?

A lot of the banks are in a really good position. A lot of financials are in a really good position to benefit from productivity savings without getting disrupted by artificial intelligence. I think that’s going to be the way investors make money going forward.

The other thing I like about the US is we think regulation is moving lower. We think there’s going to be a big merger and acquisition cycle because this administration believes that to compete, you need bigger companies.

What was your best call recently?

Cisco was up 35% in the year. Chuck Robbins has been running the business incredibly well. It’s on the other side of infrastructure spending, benefiting a little from hyperscalers but mostly from enterprise spending picking up. We think we’re seeing signs of that happening.

It also acquired Splunk for cybersecurity, which won’t be disrupted as much as other software areas. We’ve got a hardware product cycle going on, which is very bullish.

This company is managed conservatively – we call it sandbagging. They under-promise, and over-deliver – it has been beating estimates for a long time.

And your worst?

Omnicom is one of the world’s largest advertising agencies; it’s down 16% and we know management well. Their decision to merge with Interpublic Group caused consternation, with investors worried about client losses and AI disruption.

We believe AI’s impact is underappreciated; productivity benefits could push margins much higher than expected. Combining their data sets creates scale that differentiates them to clients.

We’ve been adding to the stock – it’s a top 10 position. The key is understanding the merger and whether secular disruption is real.

What do you do outside of fund management?

We’ve got a veterans centre right across from our building and we serve lunch there on the first Monday of the month. I’m also very involved in my college, Babson College. I’m an executive in residence. I tutor about 20 students that run $6m of the endowment.

I have three kids. My son and I are going to be doing a 100-mile bike ride next summer.