The UK market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, highlighting global economic uncertainties. Despite these broader market pressures, investors may find opportunities in smaller or newer companies often referred to as penny stocks. Although the term “penny stock” might seem outdated, these investments can still offer potential growth when backed by solid financials. In this article, we explore three such stocks that present promising opportunities for those looking beyond traditional blue-chip investments.

Name

Share Price

Market Cap

Financial Health Rating

Foresight Group Holdings (LSE:FSG)

£4.115

£469.18M

★★★★★★

Warpaint London (AIM:W7L)

£2.15

£173.69M

★★★★★★

AJ Bell (LSE:AJB)

£4.274

£1.71B

★★★★★★

Ingenta (AIM:ING)

£1.06

£16M

★★★★★★

System1 Group (AIM:SYS1)

£2.04

£25.89M

★★★★★★

Integrated Diagnostics Holdings (LSE:IDHC)

$0.615

$357.52M

★★★★★☆

Impax Asset Management Group (AIM:IPX)

£1.546

£187.24M

★★★★★★

Spectra Systems (AIM:SPSY)

£1.42

£68.56M

★★★★★☆

BTG Consulting (AIM:BTG)

£1.185

£190.7M

★★★★★☆

ME Group International (LSE:MEGP)

£1.44

£561.95M

★★★★★★

Click here to see the full list of 285 stocks from our UK Penny Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

Simply Wall St Financial Health Rating: ★★★★★★

Overview: CAP-XX Limited develops, manufactures, and sells supercapacitors across the Asia Pacific, Europe, and the Americas with a market cap of £14.49 million.

Operations: The company generates A$5.16 million from its development, manufacturing, and sales activities in the supercapacitor sector.

Market Cap: £14.49M

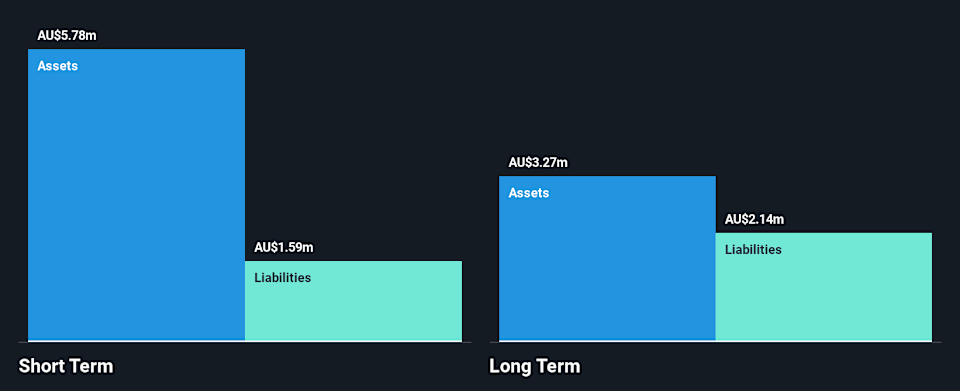

CAP-XX Limited, with a market cap of £14.49 million, operates in the supercapacitor sector and reported A$2.63 million in sales for H1 2026, showing slight growth from the previous year. Despite this revenue, the company remains unprofitable with a net loss of A$1.53 million for the period. CAP-XX’s management and board are relatively inexperienced with an average tenure of 1.7 years, which may impact strategic direction and stability. The company’s share price has been highly volatile recently; however, it maintains sufficient cash runway to support operations for over a year without debt concerns as short-term assets cover liabilities comfortably.

AIM:CPX Financial Position Analysis as at Feb 2026

AIM:CPX Financial Position Analysis as at Feb 2026

Simply Wall St Financial Health Rating: ★★★★★★

Story Continues

Overview: hVIVO plc is a pharmaceutical service and contract research company operating in the United Kingdom, Europe, and North America with a market cap of £57.83 million.

Operations: The company’s revenue is derived from its medical and scientific research services, amounting to £54.47 million.

Market Cap: £57.83M

hVIVO plc, with a market cap of £57.83 million, is experiencing challenges in earnings growth, having reported negative earnings growth over the past year. Despite this, the company maintains a debt-free balance sheet and is trading at an attractive price-to-earnings ratio of 10.9x compared to the UK market average. Recent corporate guidance suggests revenue for 2025 aligns with expectations at approximately £46.7 million, while high single-digit revenue growth is anticipated for 2026. The company’s management team and board are experienced, providing stability amid its volatile share price environment over recent months.

AIM:HVO Revenue & Expenses Breakdown as at Feb 2026

AIM:HVO Revenue & Expenses Breakdown as at Feb 2026

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Luceco plc is a company that manufactures and distributes wiring accessories, LED lighting, and portable power products across various regions including the United Kingdom, the Americas, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of £268.40 million.

Operations: The company’s revenue is derived from three main segments: Wiring Accessories (£121 million), LED Lighting (£78.8 million), and Portable Power (£58.8 million).

Market Cap: £268.4M

Luceco plc, with a market cap of £268.40 million, faces mixed prospects as a penny stock. Despite its attractive price-to-earnings ratio of 18.8x below the industry average, the company grapples with negative earnings growth and declining profit margins from 8.4% to 5.5%. Luceco’s high debt level is counterbalanced by strong asset coverage and interest payment capabilities, though its dividend track record remains unstable. Recent corporate guidance indicates optimism for exceeding revenue and profit expectations in 2026 due to momentum in energy transition sectors, while a seasoned board provides strategic oversight amidst financial volatility challenges.

LSE:LUCE Financial Position Analysis as at Feb 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AIM:CPX AIM:HVO and LSE:LUCE.

This article was originally published by Simply Wall St.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com