The UK markets have recently faced challenges, with the FTSE 100 index experiencing a downturn due to weak trade data from China, highlighting global economic interdependencies. Amid such fluctuations, investors often seek opportunities in less conventional areas like penny stocks. While the term may seem outdated, these smaller or newer companies can offer growth potential and affordability when backed by strong financial fundamentals.

Name

Share Price

Market Cap

Financial Health Rating

Foresight Group Holdings (LSE:FSG)

£4.11

£468.41M

★★★★★★

Warpaint London (AIM:W7L)

£2.10

£169.65M

★★★★★★

AJ Bell (LSE:AJB)

£4.254

£1.7B

★★★★★★

Ingenta (AIM:ING)

£1.08

£16.31M

★★★★★★

System1 Group (AIM:SYS1)

£2.04

£25.89M

★★★★★★

Integrated Diagnostics Holdings (LSE:IDHC)

$0.665

$386.58M

★★★★★☆

Impax Asset Management Group (AIM:IPX)

£1.538

£186.27M

★★★★★★

Spectra Systems (AIM:SPSY)

£1.40

£67.59M

★★★★★☆

BTG Consulting (AIM:BTG)

£1.185

£190.7M

★★★★★☆

ME Group International (LSE:MEGP)

£1.402

£547.13M

★★★★★★

Click here to see the full list of 284 stocks from our UK Penny Stocks screener.

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Impax Asset Management Group Plc is a publicly owned investment manager with a market cap of £186.27 million.

Operations: The company generated £141.87 million in revenue from its segment Impax LN.

Market Cap: £186.27M

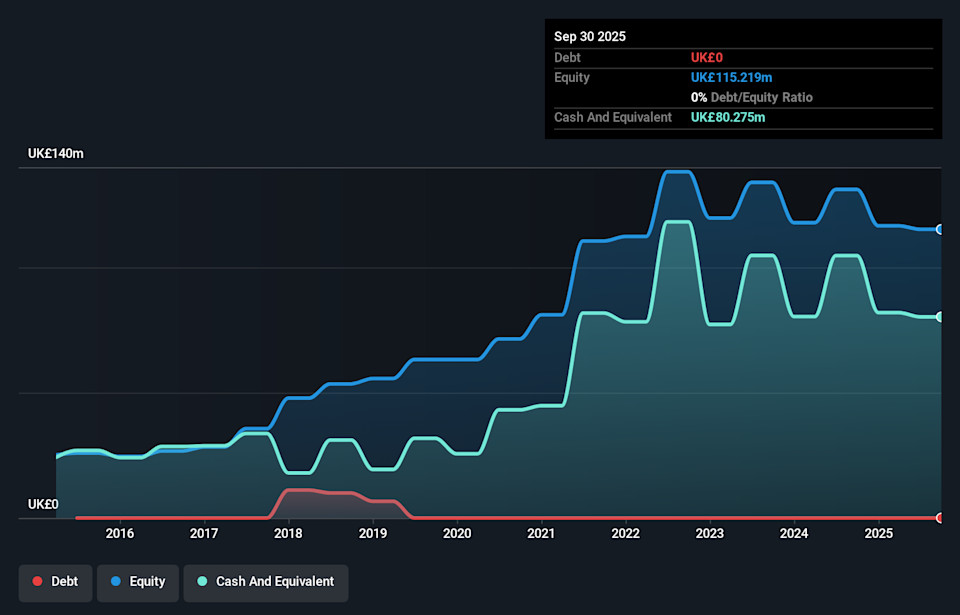

Impax Asset Management Group Plc, with a market cap of £186.27 million, has demonstrated financial stability through its strong asset position, covering both short and long-term liabilities without debt concerns. Despite recent negative earnings growth and reduced profit margins from 21.4% to 14.3%, the company maintains high-quality earnings and has not diluted shareholders recently. However, its dividend track record remains unstable with a significant reduction in payouts for 2025 compared to the previous year. The company also completed a share buyback program worth £4.64 million, enhancing shareholder value amidst challenging market conditions.

AIM:IPX Debt to Equity History and Analysis as at Feb 2026

AIM:IPX Debt to Equity History and Analysis as at Feb 2026

Simply Wall St Financial Health Rating: ★★★★★★

Overview: The Pebble Group plc operates by providing technology solutions, products, and services to the promotional merchandise industry across the UK, Continental Europe, North America, and other international markets with a market cap of £75.89 million.

Story Continues

Operations: The company generates its revenue from two main segments: Facilis Group, contributing £17.29 million, and Brand Addition, accounting for £105.82 million.

Market Cap: £75.89M

Pebble Group, with a market cap of £75.89 million, showcases financial resilience by maintaining a debt-free status and having short-term assets (£56.7M) that exceed both short-term (£31.9M) and long-term liabilities (£5.9M). The company has experienced management and board teams, with average tenures of 5.1 years and 4.5 years respectively, contributing to its stable operations despite low return on equity (7.2%). Earnings growth over the past year was modest at 5.9%, surpassing the media industry’s decline but below its five-year average growth rate of 18.7%. Future earnings are forecasted to decline by an average of 7% annually over the next three years, indicating potential challenges ahead for sustained profitability in this sector.

AIM:PEBB Debt to Equity History and Analysis as at Feb 2026

AIM:PEBB Debt to Equity History and Analysis as at Feb 2026

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Castings P.L.C. is involved in iron casting and machining operations across the UK, Europe, the Americas, and internationally, with a market cap of £116.52 million.

Operations: The company’s revenue is derived from £195.57 million in foundry operations and £31.21 million in machining operations.

Market Cap: £116.52M

Castings P.L.C., with a market cap of £116.52 million, operates debt-free and has sufficient short-term assets (£86.0M) to cover both short-term (£31.0M) and long-term liabilities (£9.8M). Despite a low return on equity (3.9%) and decreased net profit margins (2.8% from 6%), the company maintains high-quality earnings with no shareholder dilution over the past year. While it trades at 48.6% below estimated fair value, its dividend yield of 6.87% is not well supported by earnings or cash flows, indicating potential sustainability concerns despite forecasted earnings growth of 25.28% per year.

LSE:CGS Financial Position Analysis as at Feb 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AIM:IPX AIM:PEBB and LSE:CGS.

This article was originally published by Simply Wall St.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com