Jonathan Gilmour’s articles from Travers Smith LLP are most popular:

Travers Smith LLP are most popular:

within Environment topic(s)

The EMIR clearing thresholds and calculation methodology are

being changed.

On 25 February 2026, ESMA published the long-awaited final draft

regulatory technical standards on the revised clearing

thresholds.

Below we outline all you need to know about the proposed changes

–why they are important; what the new calculation

methodologies are;the revised thresholds and how they differ from

those proposed in ESMA’s earlier consultation; timelines for

compliance; and whether firms will likely consider the changes

beneficial.

For a breakdown of the jargon, please see the definitions box at

the bottom of the page.

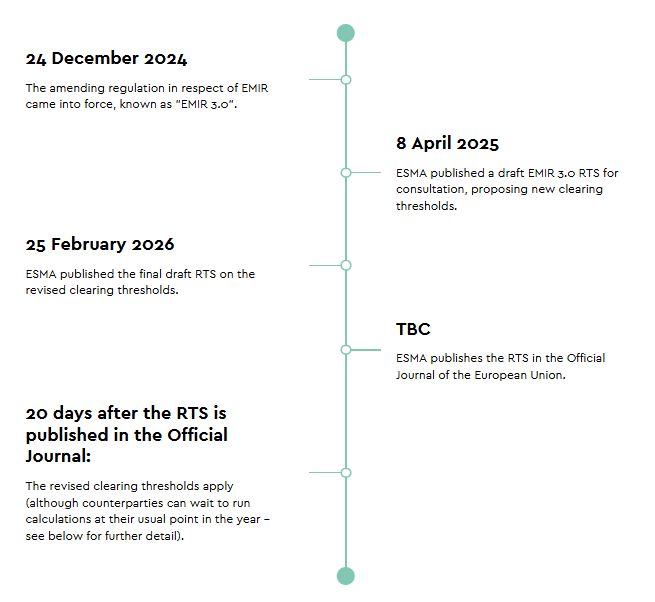

Timeline

Why is this important?

What are the key changes for NFCs?

What are the key changes for FCs?

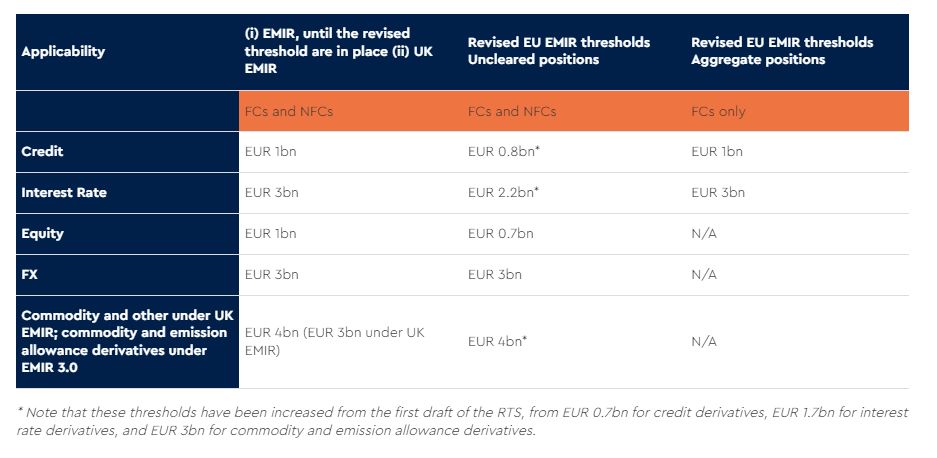

The proposed clearing thresholds (measured in gross notional

value)

Do counterparties need to conduct calculations on day 1 of the

revised thresholds coming into force?

Are the changes helpful to market participants?

1. Timeline

2. Why is this important?

Optimised treatment under EMIR for market participants relies on

counterparties remaining below the clearing thresholds.

FCs and NFCs that exceed the clearing thresholds become subject

to the EMIR clearing obligation. NFCs which exceed the clearing

thresholds become subject to other EMIR obligations – most

importantly, the obligation to exchange daily variation margin.

Please note that these changes apply only to counterparties

within scope of EMIR. The equivalent clearing thresholds under UK

EMIR have not changed.

3. What are the key changes for NFCs?

Currently:

When conducting clearing threshold calculations, NFCs include

non-risk-reducing (“speculative”) over-the-counter

(“OTC”) derivatives transactions only.

Hedging transactions entered into to reduce risks relating to

commercial or treasury financing activity of the NFC’s group

are excluded from these calculations.

Calculations include the nominal values of speculative

derivatives transactions to which an NFC is the counterparty,

as well as those carried out by any other NFCs

which are in the same “group” as the NFC.

Changes going forward:

The parameters of the hedging carve-out were helpfully, and

intentionally, unchanged – although ESMA had a mandate to

reconsider the conditions for this hedging carve-out, it elected

not to change the existing criteria.

Calculations will include only the nominal values of the

NFC’s speculative derivatives transactions which are not

cleared through an authorised CCP. Speculative transactions of

other group NFCs and any cleared speculative transactions

will no longer be included.

4. What are the key changes for FCs?

Currently:

When conducting clearing threshold calculations, FCs include

the gross notional value of all OTC derivatives transactions

(regardless of whether they are speculative or risk-reducing)

entered into by the FC and other entities within the same

“group” as the FC.

Changes going forward:

FCs will be required to look at two measures when conducting

clearing threshold calculations:

The first is the uncleared positions of the FC and all entities

in its group.

The second measure is the aggregate of its cleared and

uncleared OTC derivatives entered by the FC or entities in its

group.

Exceeding either of these thresholds will trigger the clearing

obligation.

5. The proposed clearing thresholds (measured in gross notional

value)

6. Do counterparties need to conduct calculations on day 1 of

the revised thresholds coming into force?

No.

ESMA has confirmed that counterparties do not need to run the

revised clearing threshold calculations on the day of entry into

force of the RTS – counterparties can recalculate their

positions, based on the new methodology, at the time of the year

they usually do so. For many market participants, this will be in

June.

For counterparties that wish to conduct revised calculations

earlier, this remains an option. Counterparties are able to re-do

their calculation earlier than the standard twelve months (and then

again every twelve months).

7. Are the changes helpful to market participants?

This will be fact dependent.

For market participants trading predominantly FX out of EU NFCs,

these changes are very likely to be favourable and simplify annual

EMIR clearing threshold calculations.

However, for market participants which:

Trade out of FCs; or

Trade out of UK entities (noting that UK EMIR clearing

threshold calculations have not changed); or

Trade with UK banks (which typically require a representation

as to the counterparty’s UK EMIR classification),

these changes may add another complication.

As always with regulatory changes, there are potential routes to

further optimisation. To understand how these changes may impact

your structures, please reach out to one of our team members.

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.