The United Kingdom’s stock market has faced recent challenges, with the FTSE 100 index experiencing a decline amid weak trade data from China, highlighting global economic interdependencies. In such uncertain times, identifying undervalued stocks can provide opportunities for investors seeking value in companies that may be trading below their intrinsic worth.

Name

Current Price

Fair Value (Est)

Discount (Est)

Yü Group (AIM:YU.)

£16.65

£30.88

46.1%

XP Power (LSE:XPP)

£12.28

£23.35

47.4%

Victorian Plumbing Group (AIM:VIC)

£0.644

£1.25

48.4%

Topps Tiles (LSE:TPT)

£0.346

£0.68

48.8%

Pinewood Technologies Group (LSE:PINE)

£2.085

£4.09

49%

Morgan Advanced Materials (LSE:MGAM)

£2.01

£3.70

45.7%

Eurocell (LSE:ECEL)

£1.05

£2.08

49.5%

Entain (LSE:ENT)

£5.61

£10.78

48%

Airtel Africa (LSE:AAF)

£3.446

£6.39

46%

Accsys Technologies (AIM:AXS)

£0.61

£1.16

47.3%

We’re going to check out a few of the best picks from our screener tool.

Overview: Experian plc is a data and technology company operating across multiple regions, including North America, Latin America, the UK, Europe, and Asia Pacific, with a market cap of approximately £23.39 billion.

Operations: The company generates revenue through its Consumer Services segment, which accounts for $2.15 billion, and its Business-To-Business segment, contributing $5.81 billion.

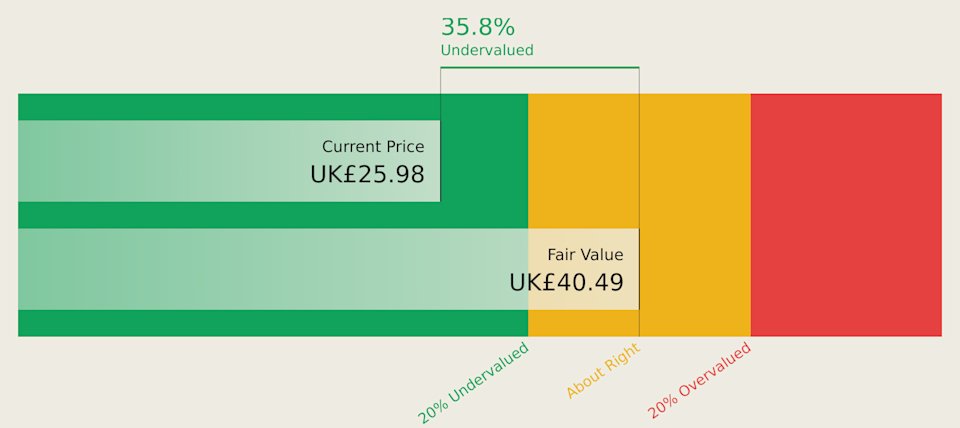

Estimated Discount To Fair Value: 35.8%

Experian is trading at £25.98, significantly below its estimated future cash flow value of £40.49, suggesting it may be undervalued based on cash flows. Recent product enhancements, such as the integration of VantageScore 4.0 into rental screening and mortgage decisions, highlight its commitment to modernizing credit evaluation processes. Despite a high level of debt, Experian’s earnings are forecast to grow by 12.17% annually, outpacing the UK market growth rate of 12.1%.

LSE:EXPN Discounted Cash Flow as at Apr 2026

LSE:EXPN Discounted Cash Flow as at Apr 2026

Overview: Kainos Group plc provides digital technology services across the United Kingdom, Ireland, the Americas, Central Europe, and other international markets with a market cap of £854.98 million.

Operations: The company generates revenue through three main segments: Digital Services (£203.43 million), Workday Products (£76.28 million), and Workday Services (£100.56 million).

Estimated Discount To Fair Value: 27%

Kainos Group, trading at £7.3, is undervalued relative to its future cash flow value of £10. Analysts concur on a potential 59.1% stock price increase, with earnings expected to grow significantly at 25.4% annually over the next three years—outpacing the UK market’s growth rate of 12.1%. However, profit margins have decreased from last year and its dividend yield of 3.96% is not well covered by earnings, highlighting some financial pressure despite robust growth forecasts.

LSE:KNOS Discounted Cash Flow as at Apr 2026

LSE:KNOS Discounted Cash Flow as at Apr 2026

Overview: Taylor Wimpey plc is a homebuilder operating in the United Kingdom and Spain with a market cap of £3.13 billion.

Operations: The company generates revenue from its homebuilding operations with £3.65 billion from the United Kingdom and £192.60 million from Spain.

Estimated Discount To Fair Value: 44.6%

Taylor Wimpey, trading at £0.89, is significantly undervalued compared to its future cash flow value of £1.6. Analysts project earnings growth of 26.3% annually over the next three years, surpassing the UK market’s growth rate of 12.1%. Despite this potential, profit margins have declined from 6.5% to 2.6%, and a high dividend yield of 8.59% remains poorly supported by earnings or free cash flows—posing financial challenges amid expansion plans and share buyback activities.

LSE:TW. Discounted Cash Flow as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LSE:EXPN LSE:KNOS and LSE:TW..

This article was originally published by Simply Wall St.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com