The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines amid weak trade data from China, highlighting concerns over global economic recovery. In such a climate, identifying undervalued stocks can be crucial for investors looking to capitalize on potential growth opportunities that may arise as market conditions stabilize.

Name

Current Price

Fair Value (Est)

Discount (Est)

Yü Group (AIM:YU.)

£16.85

£30.76

45.2%

XP Power (LSE:XPP)

£12.58

£23.37

46.2%

Taylor Wimpey (LSE:TW.)

£0.8856

£1.60

44.5%

Pinewood Technologies Group (LSE:PINE)

£2.135

£4.08

47.6%

Morgan Advanced Materials (LSE:MGAM)

£2.07

£3.71

44.1%

Lords Group Trading (AIM:LORD)

£0.1725

£0.31

44.3%

James Fisher and Sons (LSE:FSJ)

£4.62

£9.13

49.4%

Eurocell (LSE:ECEL)

£1.10

£2.10

47.5%

Entain (LSE:ENT)

£5.792

£10.67

45.7%

Airtel Africa (LSE:AAF)

£3.516

£6.35

44.7%

We’ll examine a selection from our screener results.

Overview: Mitie Group plc, with a market cap of £2.22 billion, provides facilities management and professional services in the United Kingdom and internationally through its subsidiaries.

Operations: The company’s revenue is primarily derived from Business Services (£2.43 billion) and Technical Services (£2.04 billion).

Estimated Discount To Fair Value: 25.6%

Mitie Group appears undervalued based on discounted cash flow analysis, trading at £1.73, below the estimated future value of £2.33. With earnings forecasted to grow at 30.1% per year, surpassing the UK market average, Mitie is positioned for significant profit growth despite its high debt levels and unstable dividend history. Recent executive changes aim to strengthen operational leadership as the company anticipates double-digit revenue and operating profit growth for 2026 driven by public sector projects and winter services.

LSE:MTO Discounted Cash Flow as at Apr 2026

LSE:MTO Discounted Cash Flow as at Apr 2026

Overview: S&U plc operates in the United Kingdom offering motor, property bridging, and specialist finance services with a market cap of £252.74 million.

Operations: The company generates revenue from motor finance (£70.07 million) and property bridging finance (£15.82 million) segments in the UK.

Estimated Discount To Fair Value: 27.5%

S&U is trading at £20.80, significantly below its estimated future cash flow value of £28.70, suggesting it may be undervalued. Earnings are forecast to grow at 17.6% annually, outpacing the UK market’s average growth rate, while revenue is expected to increase by 22.4% per year. Despite a high debt level and an unstable dividend history, S&U recently announced a higher interim dividend of 35 pence per share for March 2026 distribution.

LSE:SUS Discounted Cash Flow as at Apr 2026

LSE:SUS Discounted Cash Flow as at Apr 2026

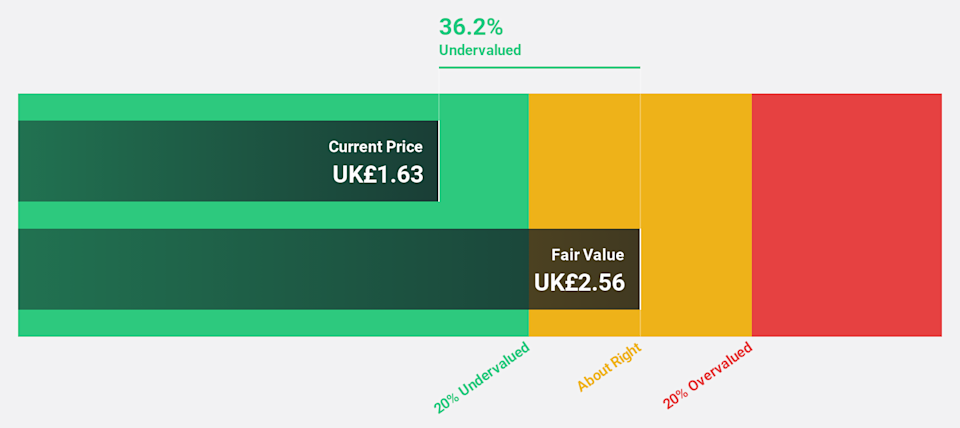

Overview: Trustpilot Group plc operates an online review platform for businesses and consumers across the United Kingdom, North America, Europe, and internationally, with a market cap of £815.95 million.

Operations: The company generates revenue of $261.05 million from its Internet Information Providers segment.

Estimated Discount To Fair Value: 38.2%

Trustpilot Group is trading at £2.07, well below its estimated future cash flow value of £3.35, indicating potential undervaluation. Earnings are projected to grow significantly at 50.4% annually, surpassing the UK market’s average growth rate, with revenue expected to rise by 15.3% per year. Despite recent regulatory challenges in Italy and a volatile share price, Trustpilot’s strategic share buyback program and leadership changes may enhance financial stability and investor confidence moving forward.

LSE:TRST Discounted Cash Flow as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LSE:MTO LSE:SUS and LSE:TRST.

This article was originally published by Simply Wall St.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com