In recent months, the United Kingdom’s financial markets have faced challenges, with the FTSE 100 and FTSE 250 indices experiencing downturns due to weaker trade data from China and declining commodity prices affecting major sectors. Amid these broader market pressures, discerning investors are increasingly seeking out smaller companies that exhibit resilience and potential for growth despite global economic uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals In The United KingdomNameDebt To EquityRevenue GrowthEarnings GrowthHealth RatingGoodwin24.30%12.58%22.87%★★★★★★Andrews Sykes GroupNA2.01%5.12%★★★★★★BioPharma CreditNA5.72%5.22%★★★★★★Georgia CapitalNA13.71%21.08%★★★★★★Vectron SystemsNA2.48%28.82%★★★★★★Nationwide Building Society282.42%9.69%21.24%★★★★★☆FW Thorpe2.19%9.09%11.33%★★★★★☆Foresight Environmental InfrastructureNA-24.80%-27.25%★★★★★☆Strategic MineralsNA4.81%-40.63%★★★★★☆Distribution Finance Capital Holdings12.97%42.17%59.43%★★★★☆☆

Let’s explore several standout options from the results in the screener.

Simply Wall St Value Rating: ★★★★★★

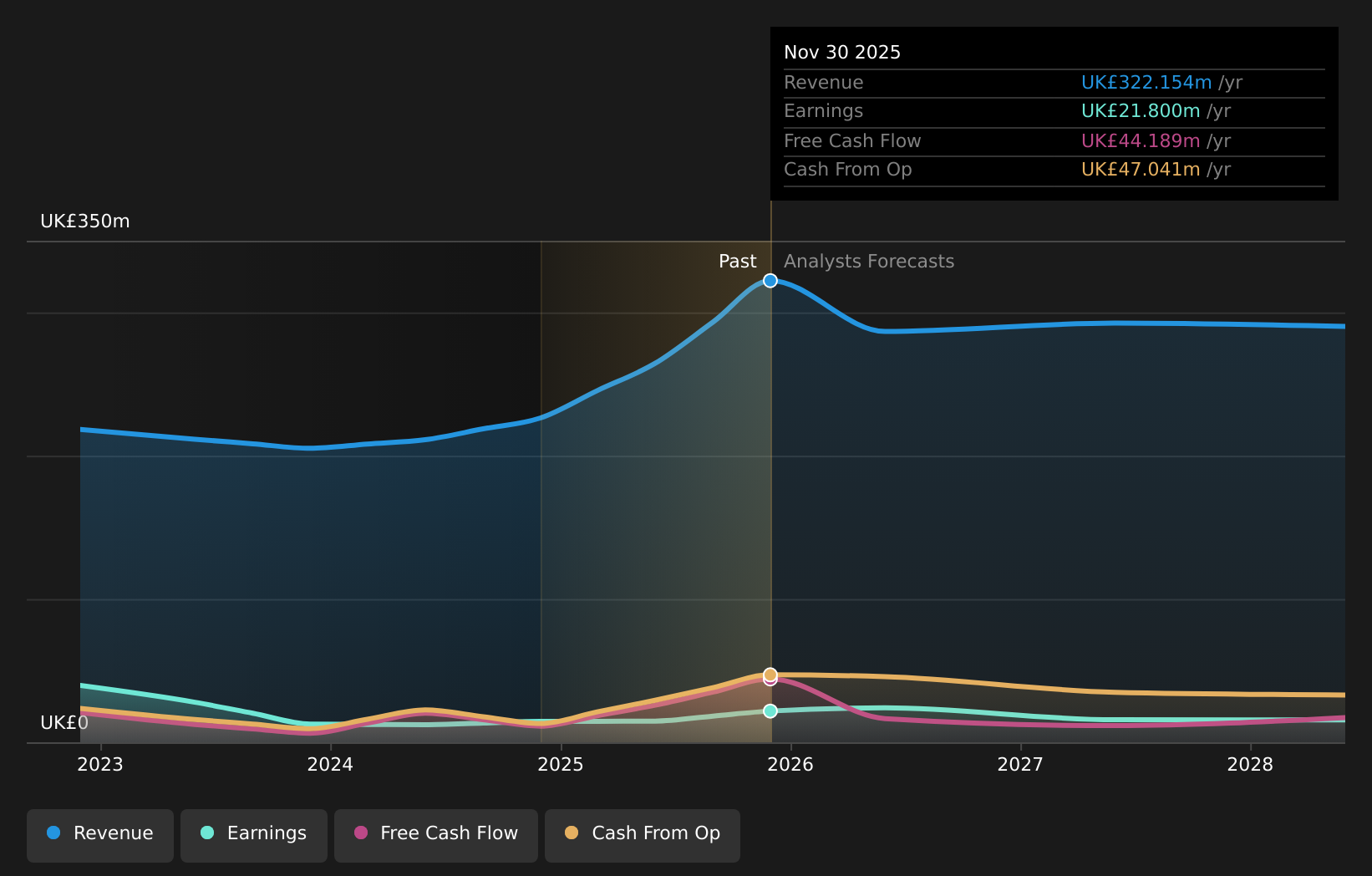

Overview: Hargreaves Services Plc offers environmental and industrial services across the United Kingdom, Europe, Hong Kong, and other international markets with a market capitalization of £249.25 million.

Operations: Hargreaves Services generates revenue primarily from its services segment, contributing £298.80 million, while Hargreaves Land adds £27.64 million to the total revenue.

Hargreaves Services, a nimble player in the UK market, has shown robust earnings growth of 49.8% over the past year, outpacing its industry peers. With a price-to-earnings ratio of 11.4x, it trades below the broader UK market average of 15.1x, suggesting potential value for investors. The company is debt-free now compared to five years ago when its debt-to-equity ratio was 12.6%. Recent strategic moves include a £20 million share repurchase program and securing contracts worth £10 million for infrastructure projects like Lower Thames Crossing, enhancing its profile in sustainable construction initiatives.

AIM:HSP Earnings and Revenue Growth as at Apr 2026

AIM:HSP Earnings and Revenue Growth as at Apr 2026

Simply Wall St Value Rating: ★★★★★☆

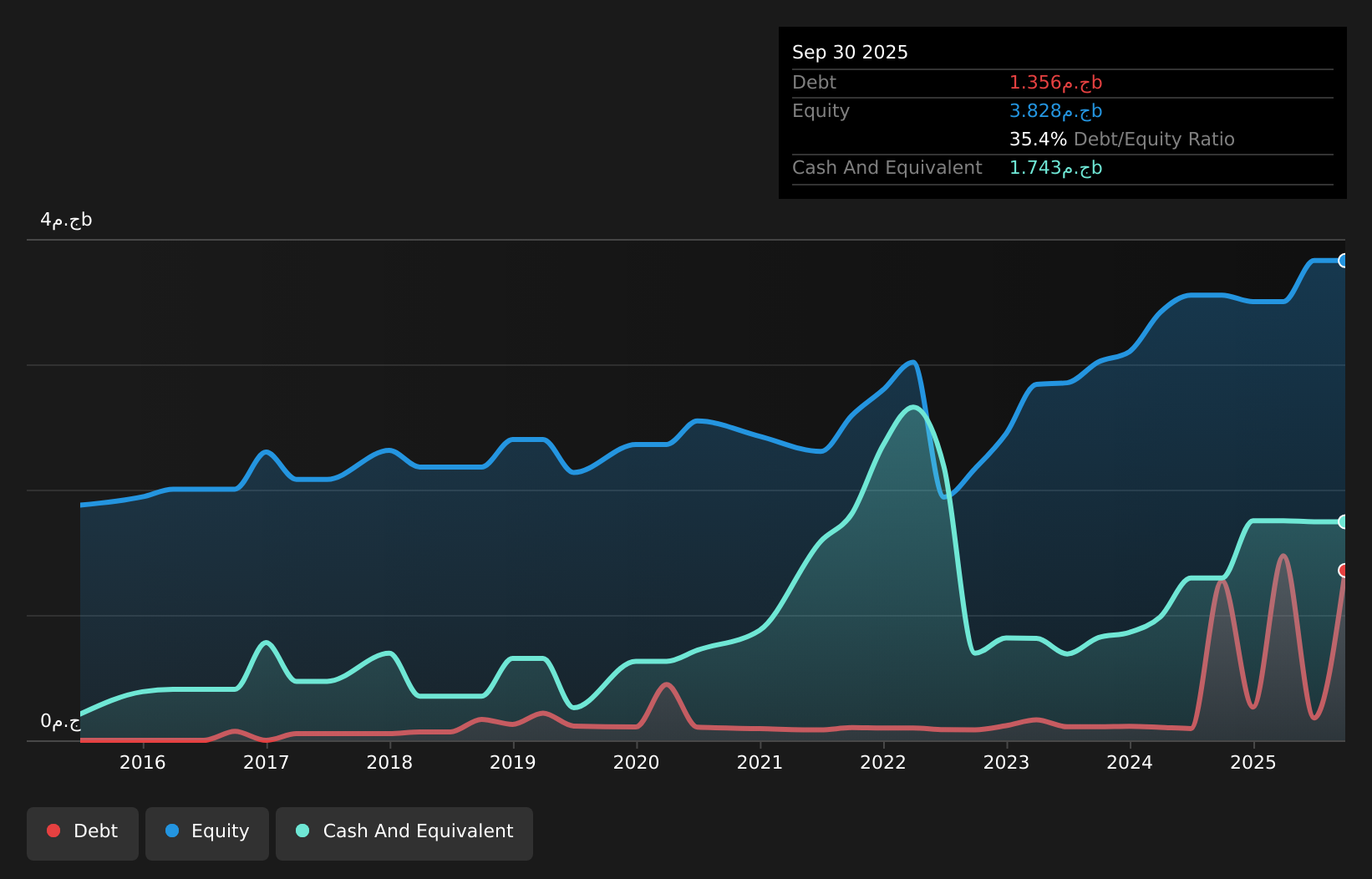

Overview: Integrated Diagnostics Holdings plc is a consumer healthcare company offering medical diagnostics services, with a market cap of $348.80 million.

Operations: The company generates revenue primarily through its medical diagnostics services. The cost structure includes expenses related to service delivery and operational activities. Its financial performance is characterized by a net profit margin of 22.5%.

Integrated Diagnostics Holdings (IDH) showcases a compelling mix of strategic growth and financial prudence, with its earnings surging 55.5% last year, outpacing the healthcare sector’s 7% growth. The company trades at 75.3% below estimated fair value, suggesting potential upside for investors. IDH’s debt-to-equity ratio has climbed from 4% to 35.4% over five years, yet it boasts more cash than total debt, ensuring stability in volatile markets like Egypt and Nigeria. With an EBIT covering interest payments by a factor of 46.3x, IDH seems well-prepared to handle future economic challenges while pursuing expansion in Saudi Arabia and Egypt’s radiology services market.

LSE:IDHC Debt to Equity as at Apr 2026

LSE:IDHC Debt to Equity as at Apr 2026

Simply Wall St Value Rating: ★★★★☆☆

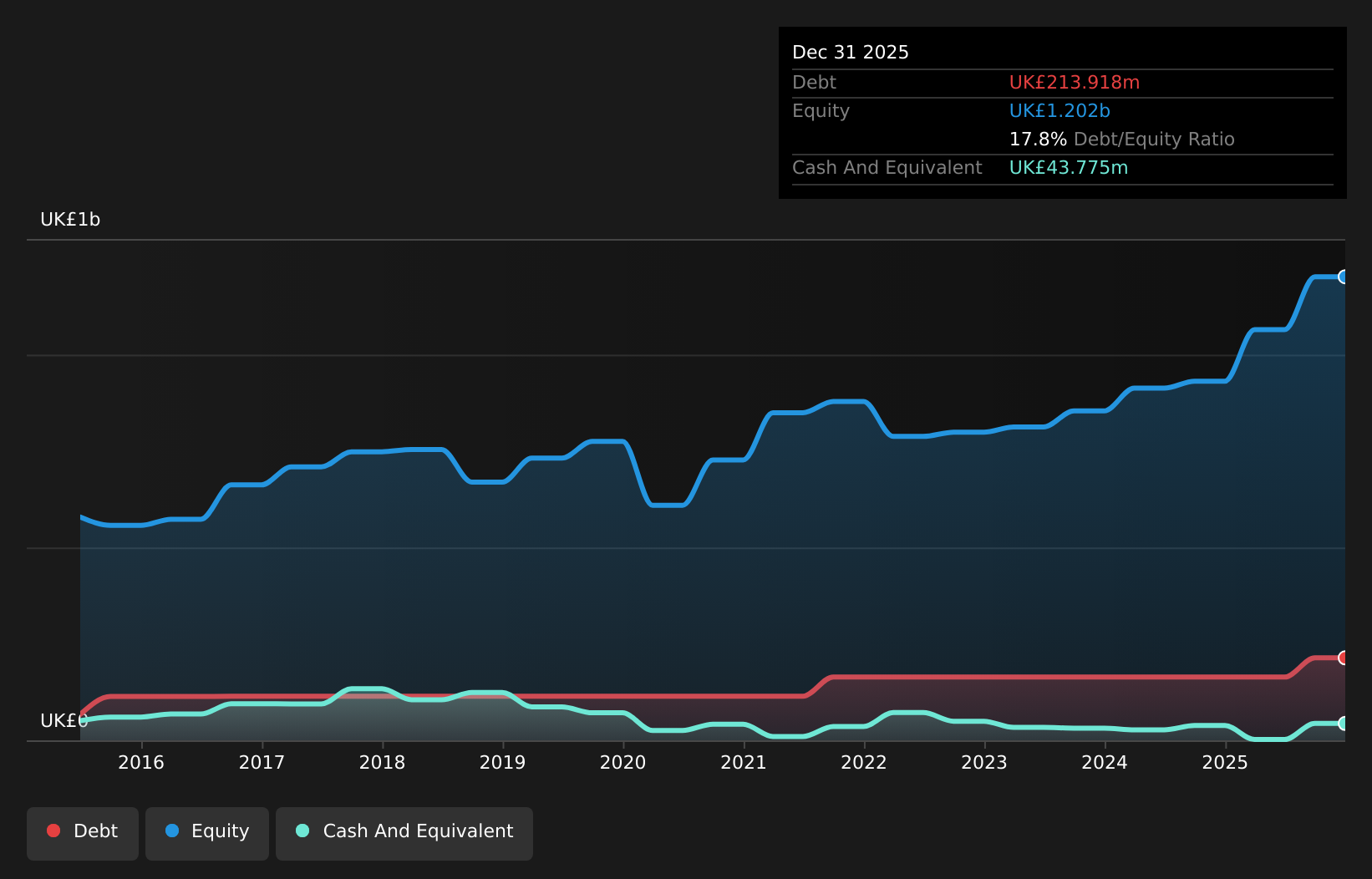

Overview: The Law Debenture Corporation p.l.c. is an investment trust that offers independent professional services globally, with a market capitalization of £1.44 billion.

Operations: Law Debenture generates revenue primarily from two segments: Investment Portfolio (£43.04 million) and Independent Professional Services (£66.70 million). The latter contributes a larger share to the company’s total revenue stream.

Law Debenture, a small player in the UK market, has shown impressive growth with earnings skyrocketing by 214% over the past year, far outpacing the Capital Markets industry average of 15.5%. Trading at 6.1% below its estimated fair value suggests potential undervaluation. The company’s net debt to equity ratio stands at a satisfactory 14.2%, indicating prudent financial management. Additionally, interest payments are well-covered by EBIT with a coverage of 42 times, reflecting robust operational performance. Recent announcements highlight significant revenue increase to £374 million from £176 million and net income jumping to £304 million from £97 million year-on-year.

LSE:LWDB Debt to Equity as at Apr 2026Key TakeawaysWant To Explore Some Alternatives?

LSE:LWDB Debt to Equity as at Apr 2026Key TakeawaysWant To Explore Some Alternatives?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com