Products featured in this article are independently selected by This is Money’s specialist journalists. If you open an account using links which have an asterisk, This is Money will earn an affiliate commission. We do not allow this to affect our editorial independence.

You could benefit from one-off financial advice to help with an aspect of your finances, and this doesn’t have to tie you into a long-term relationship with a financial adviser.

Advisers were banned from taking payments from financial providers for pushing their products a decade ago. Many have changed their practice to charging upfront fees for initial help, plus levying an annual percentage of your funds for their services.

But paying ongoing fees isn’t compulsory and might not be value for money unless you’re getting a substantial level of ongoing advice in exchange each year.

It’s perfectly acceptable to get expert assistance from a financial adviser on a single concern on the basis it will be one transaction, pay up, then walk away.

So what kind of issues can you get advice on? And if you approach a professional for one-off financial advice, what should you ask for and what can you expect to receive in return?

And importantly – how much will it all cost? We explain more in this guide.

We also cover investing a pension, because living off the income over many decades means that ongoing advice may very much be worth your money. We look into what you should weigh up before deciding how much help you need.

> Find a financial adviser in your area with Unbiased*

Seeing a professional adviser: Many people could benefit from one-off expert help over some aspect of their finances

When is it useful to get one-off financial advice?

Getting one-time help for a pre-agreed fee can be appropriate in the following situations.

Setting up a plan to reach a certain level of income by the time you retire

In these circumstances, someone in their 30s or 40s now might be looking ahead to a retirement age of 68 and want to generate a decent income over and above their state pension.

For a one-off fee, an adviser could create a cash flow report which tells them how much they need to save and offer a practical plan to reach this goal.

Arranging a plan to help you retire early

If someone hopes to retire at 50, 55 or 60, an adviser can help them find out what level of income they need in retirement.

An adviser will tease out your objectives and tell you whether your goal is achievable and what you need to do to make it happen. If you’re already on course, they can also tell you how you can further improve your situation.

Dealing with fallout from the abolition of the lifetime allowance

The previous chancellor, Jeremy Hunt, ditched the £1,073,100 total limit people can have in their pension pot without facing tax penalties.

But for people with large pension pots, there can be longer term implications, especially regarding tax-free lump sums.

If your pension is worth this much, an adviser will help you avoid costly mistakes.

> How to defend your pension from the taxman

Buying life assurance

This means setting up cover to last until you die, as opposed to life insurance which will only be in effect for a set period.

This could be suitable for someone who doesn’t have enough disposable income to save big sums but wants enough cover to get their mortgage paid off and protect their family’s financial position if they die.

Wanting to know what to do with an inheritance

People coming into money, especially if their means were relatively modest beforehand, often need help deciding what to do with a large lump sum, and how to mitigate any future inheritance tax liability for their own heirs.

> 10 ways to avoid inheritance tax (legally)

Creating a plan to financially assist your child in later life

Having a child often prompts people to rethink their finances. They might want to put aside funds to help their offspring in later life, pre-empting major expenses such as university fees.

Reorganising your finances after a divorce

Splitting household assets and property also makes people reset their goals. They often want to seek help when putting their finances on a new path.

HEATHER ROGERS ANSWERS YOUR TAX QUESTIONS

> How to split pensions in a divorce: The three main options explained

Starting to take an income from a pension fund

Some people want help deciding whether to buy an annuity that provides a guaranteed income for life – and how to proceed if they do want to go ahead.

There’s also the option of investing a pension pot to fund retirement instead. Alternatively there’s also a hybrid solution where you buy an annuity to cover essential expenses and invest the rest, or you can invest to start with and then buy an annuity in later life.

Just choosing an annuity is a one-off transaction, and you can walk away from your adviser afterwards.

But investing your pension involves setting up a portfolio that needs to be managed, so you might want an ongoing relationship with an adviser – and they’re likely to encourage this.

You may or may not want to agree to this, and you should check your contract with a financial adviser for any restrictions or lock-in periods.

Getting advice on a final salary pension transfer

Pension savers are often tempted away from final salary schemes to invest in the financial markets instead, but this can mean giving up valuable benefits.

Whether this is a sensible idea will rest on your individual circumstances. As a safeguard, it’s compulsory to pay for financial advice before transferring a final salary pension worth £30,000-plus.

If you decide to stay put, you’ll only need one-time help. But if you decide to transfer into a drawdown scheme, then as in the scenario above, you may want ongoing help.

> The best self-invested personal pensions (Sipps)

Could financial advice make you wealthier?

Financial advice – and its sibling, financial planning – can help you grow your wealth, sort your pensions, or make sure your finances are as tax efficient as possible.

Many people choose to take financial advice around building wealth for retirement and for inheritance tax planning.

We’ve partnered with the financial advice firm, Flying Colours, to help you understand whether financial planning could help you:

> Are you retirement ready? Take the quiz and find out*

> Inheritance tax: Use this calculator to find out how much tax will be due*

Services such as Unbiased can also match you with a financial professional according to your needs:

> Find a local financial adviser*

<!- – ad: https://mads.dailymail.co.uk/v8/us/money/none/article/other/mpu_factbox.html?id=mpu_factbox_1 – ->

Should you get ongoing advice if you invest your pension in retirement?

Getting ongoing help from a financial adviser involves handing over a percentage of your pension pot every year – many people baulk at this.

Retirement can last decades. This is a long time to fork over big sums, when not much about your circumstances or your portfolio might change from year to year.

It also means that your investment returns must ideally be good enough over time to justify the ongoing adviser fee, in addition to absorbing investment charges and beating inflation.

One option could be to pay an adviser to set up a portfolio that you’re comfortable monitoring and managing yourself at the outset of retirement. Then you can get your investments and financial circumstances reviewed at intervals.

You could aim for a review every five years, or when there’s a significant development like receiving an inheritance. You could even use a new adviser each time, which would have the advantage of getting fresh eyes on your finances.

That said, there are important benefits to getting ongoing advice, which may turn out to be invaluable depending on your situation.

You should certainly question an adviser closely about what services they’ll offer that could make this worth your while, listening with an open mind.

It’s also the case that rules and taxes change over the years, and input from an adviser can keep you on the right track and help you avoid expensive mistakes.

You might consider yourself well-informed, but the rules are complex, and you won’t know how an adviser could help until you pay up and find out.

But one other thing to bear in mind is the risk of getting tied to an adviser’s ‘own funds’ and having to use their in-house platform. Watch out for any exit penalties – you can read more on this below.

One-off versus ongoing financial advice: What else to consider

Justin Modray, director of Candid Financial Advice, thinks it can be sensible for people to get ongoing help in retirement but it’s their decision.

‘We don’t thrust it down their throats. It’s up to them,’ he says. ‘If it seems they will struggle we would tell them they need advice, but we would never pressure them.’

Which pension and Isa platforms are open to both advisers and direct to consumers?

Justin Modray says choosing one of these is sensible, because if you decide to change adviser or start looking after things yourself, you shouldn’t have to move platform.

But bear in mind that all these firms will charge you an annual percentage fee.

AJ Bell

Aviva

Fidelity

Scottish Widows

<!- – ad: https://mads.dailymail.co.uk/v8/us/money/none/article/other/mpu_factbox.html?id=mpu_factbox_2 – ->

He warns that some advisers will ‘harvest’ pension investment business by putting clients in their own in-house funds and on their own platforms and then get a cut from the fees they generate, as well as for ongoing advice.

‘They get as much money into their platform or fund as possible, and charge an annual fee. There are two big risks to this – high fees, and being tied to their funds and/or platform if you decide to leave.’

Modray says to avoid this, people should take one-off or ongoing advice from a firm that’s willing to use an investing platform that’s available across the market, both direct to consumers and to other advisers – see the fact box for more.

That way, if you decide you don’t like your adviser, or simply want to look after your investments yourself, you won’t be tied to your original firm and their platform. Making your investments portable, and accessible by other advisers, means you won’t be limiting your future choices.

Modray says this applies to people using financial advisers to set up investing in Isas, as well as managing investments in retirement.

‘Ask at the beginning and say you don’t want a tied platform and funds. Usually the only reason advisers do this is because it’s more profitable for them. It’s not done for the benefit of a client.’

> Read more: The best investment platforms: How to choose an investment account

How do you find an adviser willing to give you one-off advice?

Ask upfront, and if an adviser tries to sign you up to an ongoing deal instead, you don’t have to agree just because it might be their usual practice with other clients.

If they set something up for you, like an investment portfolio, that doesn’t mean you’re obliged to hand over a percentage of your fund forever.

Hear them out, just in case they have valid reasons for believing it will be for your benefit and can make a strong case for the services they can offer you in exchange. But keep in mind you’re the customer and can walk away.

Decide what level of service you’ll be comfortable with – for example remote, such as by phone or email, or face to face.

Also, are you happy to see a ‘restricted’ adviser, offering a smaller range of products from a provider to which they’re probably tied? Otherwise, you might prefer a fully ‘independent’ adviser, who will look at the whole market when trying to meet your needs.

Modray warns it could be tricky to find an adviser who will provide cost-effective help as a one-off.

‘Advice is tightly regulated, so the adviser will need to spend time collecting and documenting information, even if what you’re asking for is relatively straightforward,’ he says.

‘And being blunt, it will likely be less profitable for them versus taking on a client they will look after long term, so you may struggle to find one who will oblige.

‘Some employers provide access to pension guidance or advice for their employees, so it is well worth asking them if this is an option.’

Modray gives the following general pointers about approaching financial advisers: ‘Tell an adviser what you want. They can say no. If it’s unreasonable, you will soon know as they will all say no.

‘People can feel intimidated and scared to ask questions. Costs can be taboo. People don’t challenge costs. Never ever be afraid to challenge costs. Don’t proceed unless you understand the charges.

‘If they seem high, stop, think about it. Don’t proceed until you feel happy about it. Never be afraid to walk away if you don’t think you are getting a fair deal.’

Beware financial advice that costs more than 2.5%

Modray says people should be wary of charges of 2.5 per cent plus. He says one rule of thumb for whether costs are fair is to ask how many hours an adviser expects to spend helping you, then work out the equivalent hourly rate. He adds that advisers might normally spend 20-30 hours tops on your case.

Modray suggests another test is to look at the adviser’s website and see if they publish their fees, with ballpark figures for different scenarios. Those who are expensive could be avoiding putting people off by not publishing the figures.

What does financial advice cost?

Henry Tapper is a retired financial adviser and founder of the Pension Playpen professional network and AgeWage, which analyses whether pensions are value for money.

‘I would expect to pay £200 per hour for high quality financial advice and I would expect my adviser to advertise an hourly rate as well as quote fixed fees,’ he says regarding the cost of financial advice.

‘You must make it clear that this is project work and not an annual contract.

‘Good advisers should be able to quote you a fixed price for a one-off project which won’t commit you to ongoing advice. Do not skimp on this. You should expect to pay a four-figure fee for this work and pay VAT on top.

‘A good financial adviser’s fees will typically compare favourably to those of solicitors and tax-advisers. Professional advice, regulated by the FCA and backed by professional indemnity insurance is worth paying for.

As a general tip, Tapper reckons you should be careful about letting advisers take their fees from your investments.

‘The fee may not sound very much but even 0.5 per cent to 1 per cent of your wealth can work out as expensive compared with a fixed fee.

‘Your adviser may explain that it is more efficient for them to take their fees this way (it is true that it helps you avoid VAT) but it may be better to pay VAT than find yourself locked into a long-term contract.

‘Some advice firms have a lock-in period, which is fine where you use an adviser for life but is not value for money if you just want occasional advice.’

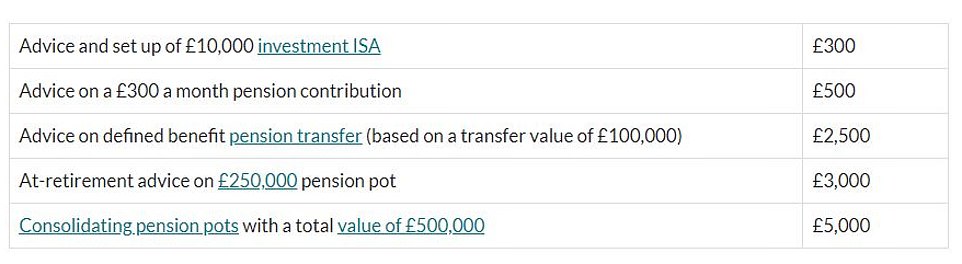

Comparison site Unbiased carriers out surveys of its financial adviser members about charges and calculates the averages below as a guide.

Average fees for typical adviser services based on Unbiased.co.uk research

Get your financial planning question answered

Financial planning can help you grow your wealth and ensure your finances are as tax efficient as possible.

A key driver for many people is investing for or in retirement, tax planning and inheritance.

If you have a financial planning or advice question, our experts can help answer it. Email: financialplanning@thisismoney.co.uk.

Please include as many details as possible in your question in order for us to respond in-depth.

We will do our best to reply to your message in a forthcoming column, but we won’t be able to answer everyone or correspond privately with readers. Nothing in the replies constitutes regulated financial advice. Published questions are sometimes edited for brevity or other reasons.

<!- – ad: https://mads.dailymail.co.uk/v8/us/money/none/article/other/mpu_factbox.html?id=mpu_factbox_3 – ->

SAVE MONEY, MAKE MONEY

Sipp cashback

Sipp cashback

£200 when you deposit or transfer £15,000

![]()

4.51% cash Isa

![]()

4.51% cash Isa

Trading 212: 0.66% fixed 12-month bonus

£20 off motoring

£20 off motoring

This is Money Motoring Club voucher

Up to £100 free share

Up to £100 free share

Get a free share worth £10 to £100

No fees on 30 funds

No fees on 30 funds

Potentially zero-fee investing in an Isa or Sipp

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence. Terms and conditions apply on all offers.