Summary

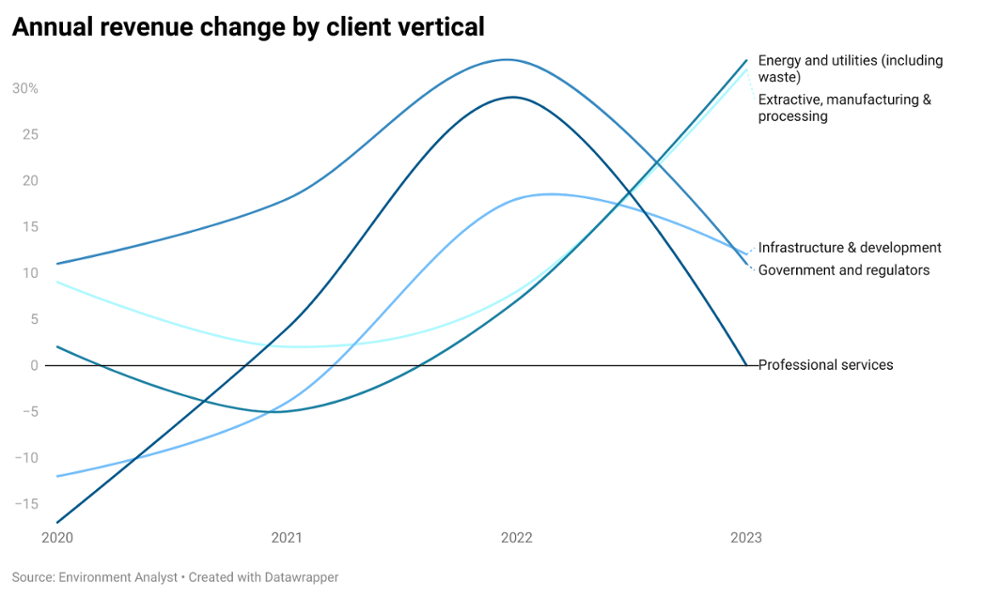

Energy and utilities was the fastest growing sector in 2023.

Revenue from government and regulator clients grew by 11% in 2023 but is projected to contract by 2028.

Infrastructure and development client spending rebounded after the pandemic and is forecast to grow the fastest through to 2028.

The US environmental and sustainability (E&S) consulting market expanded by 20% in 2023, according to Environment Analyst’s latest US Environmental & Sustainability Consulting Market Assessment.

Growth in 2023 was almost three times larger than in previous forecasts, which projected a mere 7%.

This was largely driven by federal investment in the energy transition and infrastructure resilience, accelerated by rapid advances in AI and the subsequent emergence of energy- and resource-intensive technologies.

Energy utilities, industrial operations and infrastructure clients led this surge, each recording double-digit spending growth.

Fastest growing sectors

The energy and utilities (including waste) client sector became the largest contributor to the E&S market in 2023, growing by 33%, gaining well over a third of the market share.

Work for energy transmission clients (a subsection of the wider energy and utilities sector) rose sharply, increasing its market share by four percentage points.

This was driven by soaring power demand linked to AI expansion, large-scale renewable integration and generous federal clean energy funding from 2020, through programmes like the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA).

Yet, the buildout of transmission infrastructure still lags behind clean energy targets.

And the energy sector more broadly faces uncertainty as Trump’s administration shifts focus to domestic fossil fuel production, affecting future project pipelines for certain technologies, like wind farms.

Despite this, the energy and utilities client sector is projected to grow at an 8% compound annual growth rate (CAGR) by 2028, as energy demand, regardless of source, is set to increase.

The extractive, manufacturing and processing industries recorded the second-fastest growth in US E&S advisory spending in 2023. With a 32% increase versus 2022, the sector now accounts for the market share of 14%.

The sector is forecast to grow at 10% CAGR through to 2028, supported by policies favouring domestic manufacturing and mining.

Infrastructure and development ranked third in growth, with client spending rising 12% in 2023, gaining just over a tenth of the total market.

This rebound follows pandemic-induced contractions in 2020 and 2021. Federal stimulus and green economy initiatives like the IIJA and IRA reignited spending, particularly in rail, aviation and public transport projects.

Environment Analyst forecasts this sector will see the fastest growth over the next five years, with an 11% CAGR by 2028, as consultancies report strong proposal activity.

Government and regulator spending at risk

In 2023, work for government and regulatory clients made up almost a third of the US E&S consulting market. This is slightly lower when compared with 2022, as most of this funding stemmed from Biden-era federal programmes enacted earlier in his term.

With Trump’s administration cutting these funds and shifting focus away from green policies, the sector’s spending on E&S advisory is expected to decline at a -2% CAGR through to 2028. That said, it is forecast to remain the second largest market contributor after energy and utilities.

Consultancies heavily reliant on federal projects face increased business uncertainty, but many maintain long-standing relationships with public sector clients. Ongoing and new multi-year contracts offer a degree of stability despite shifting political priorities.

Tetra Tech is a great example, recently adding over $1bn of new contract capacity. This covered water supply and flooding infrastructure projects, through partnerships with the US Army Corps of Engineers and the Office of Land and Emergency Management.

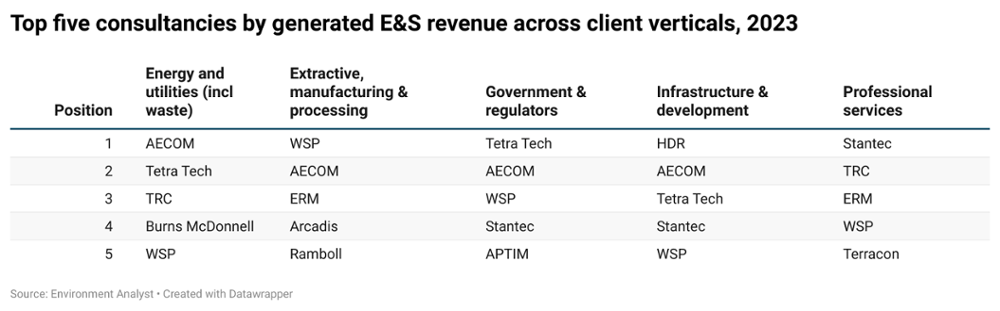

Big players strengthen dominant positions

The largest client vertical, energy and utilities (including waste), is primarily dominated by AECOM and Tetra Tech. These two companies account for 15% and 13%, respectively, of the total revenue generated by the top 27 US consultancies in this sector.

Alongside TRC, Burns & McDonnell and WSP, these firms accounted for nearly 63% of the total US 27 generated revenue from this client sector in 2023.

Tetra Tech also leads the second largest client vertical – government and regulators – holding alone almost a third of the US top 27 generated revenue from this client vertical.

AECOM is the second largest player, with under a fifth market share in this segment.

WSP’s dominant position in the US E&S consulting market is driven by the extractive, manufacturing and processing sector. It holds 30% of revenue generated by the US top 27 from this segment through high-value, multi-year contracts. This growth reflects a 40% expansion in the company’s Earth and Environment division.

HDR secured almost a fifth of the US top 27 infrastructure and development revenue in 2023, largely by winning $1.6bn in federal grants under the IIJA for projects in freight rail, aviation, public transit, highways and maritime sectors.

Stantec led the professional services segment, contributing around 30% of the total revenue generated by the top firms.

© Environment Analyst. You may circulate web links to our articles, but you may not copy our articles in whole or in part without permission

CORRECTIONS: We strive for accuracy, but with deadline pressure, mistakes can happen. If you spot something, we want to know, please email us at: news@environment-analyst.com

We also welcome YOUR NEWS: Send announcements to news@environment-analyst.com