Carbon permits in the European Union have recently climbed to their highest levels since August 2023. The rise reflects tighter supply, policy decisions, and shifting market demand under the EU Emissions Trading System (ETS).

The ETS is the world’s largest cap-and-trade system for greenhouse gas emissions. It mandates large emitters to buy allowances for the carbon dioxide they emit. These allowances are known as EU Allowances (EUAs).

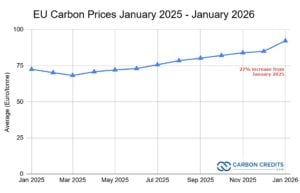

EUAs are now trading at a price over €92 per tonne — the strongest level in about 18 months. This rise shows that companies and markets expect fewer allowances to be available in the future as the EU tightens its emissions cap.

What Is the EU Emissions Trading System?

The EU ETS began in 2005 as a tool to reduce greenhouse gas emissions through market forces. It sets a cap on total emissions from major sectors such as power generation, manufacturing, and aviation. Companies must hold enough allowances to cover their emissions each year.

The cap reduces over time, meaning fewer EUAs are issued. This creates scarcity. As allowances become scarcer, their price tends to rise, which increases costs for polluters. In theory, this pushes companies to reduce emissions or invest in cleaner technology.

In 2026, the system also overlaps with the Carbon Border Adjustment Mechanism (CBAM), a tax on imported carbon-intensive goods. CBAM began to apply in January 2026 and makes carbon costs visible on imports like steel and cement. The measure aims to cut down on “carbon leakage.” This happens when industries move production to areas with cheaper carbon prices.

Recent Price Moves: Highest Since August 2023

In early January 2026, EU carbon permits climbed as high as about €91.82 per tonne on EU markets, up from lower levels earlier in 2025. Now, it’s trading at over €92 per tonne, showing 27% increase from January 2025 prices. The rise represents a fourth consecutive weekly gain in allowances for the December 2026 contract.

Data source: TradingEconomics

Data source: TradingEconomics

The price rise reflects tightening supply — fewer allowances are available through auctions and free allocations. Reduced supply increases competition among companies that must surrender EUAs to match their emissions. This dynamic pushes the price higher.

Market analysts also note that colder weather and more heating needs in winter often boost industrial energy demand. This can lead to higher carbon prices during the season.

Why Prices Have Risen?

The recent uptick in EU carbon prices is driven by several key factors:

Reduced Supply of Allowances:

The EU continues to tighten its emissions cap and reduce the number of new allowances issued. Estimates from the European Exchange auction calendar and Market Stability Reserve show that auction volumes will drop. They are expected to fall from about 588.7 million EU Allowances in 2025 to around 482.4 million in 2026. A stronger cap reduces the total pool of tradable EUAs, creating scarcity and upward pressure on prices.

Policy Signals and Reform Expectations:

Investors and companies anticipate future regulatory tightening. The EU’s long-term climate goals include cutting net emissions by 90% by 2040 compared with 1990 levels. Such policy signals can strengthen confidence that carbon costs will rise further.

Market Confidence and Funds:

Investment funds have increased their holdings of EU carbon futures. Trading positions and speculation can also influence price momentum, especially as market sentiment shifts toward tighter futures.

Industries covered by the ETS are required to surrender allowances to match their emissions by compliance deadlines. As deadlines near, buying activity can increase, adding short-term upward pressure on prices.

Carbon Border Adjustment Mechanism:

With CBAM now active, imported products from outside the EU face carbon costs similar to domestic industries. This mechanism can reduce free allowance allocations and tighten supply further.

Looking Back and Ahead: Carbon Price Trends and Forecasts

Carbon prices in the EU ETS have fluctuated over recent years. Prices surged above €100 per tonne in early 2023. Then, they eased back in 2024 and 2025. This decline was due to shifting market conditions and wider economic factors.

In 2024, the average price of EU ETS carbon permits was around €65 per tonne, down from €84 per tonne the year before. High prices in 2023 reflected strong policy signals from the Fit for 55 climate package and global energy disruptions.

Looking ahead, analysts and forecast models expect prices to continue rising over the coming decade:

A survey of market participants predicts that the average EU ETS carbon price will rise to almost €100 per tonne from 2026 to 2030. This increase will happen as demand exceeds supply.

Energy market analysts predict that the average price could hit about €126 per tonne by 2030. This rise is due to stricter caps and wider emission coverage.

Under the EU ETS II framework, starting in 2027, more sectors will be included, like buildings and transport. In some scenarios, prices might average €99 per tonne from 2027 to 2030.

BNEF’s EU ETS II Market Outlook projects carbon prices reaching €149 per metric ton ($156/t) by 2030, driving substantial emissions reductions.

Source: BNEF

Source: BNEF

Overall, these forward estimates imply that allowance prices may continue to rise as the EU strengthens its emissions targets to meet climate goals.

Emissions Reductions Under the ETS

The EU ETS has contributed to measurable emissions reductions. In 2024, emissions under the system were roughly 50% lower than in 2005. This progress is set to help the EU meet its 2030 goal of a 62% reduction from 2005 levels. The decline was driven mainly by cuts in the power sector, with increased renewable energy and a shift away from coal and gas.

Renewable energy growth, including wind and solar, played a role. Increases in renewables helped lower emissions by reducing reliance on fossil fuels.

The drop in emissions may lead to higher demand for allowances in the long run. With fewer emissions, companies will need more allowances to meet the cap.

What Higher Carbon Prices Mean for Industry

Higher carbon prices affect the European economy in many ways. For polluting industries, rising carbon costs increase operating expenses. Companies may invest more in cleaner technologies to reduce their allowance needs. This can accelerate decarbonization technology adoption.

Policy makers face the challenge of balancing climate goals with economic competitiveness. Some EU governments, like France, want price limits in the ETS. This could stop big swings in carbon costs. It would also help industries plan better.

The Market Stability Reserve (MSR), a mechanism to absorb excess allowances, also plays a role. It intends to reduce surplus permits and stabilize prices. Combined with the tightening cap, the MSR tends to push prices higher over time.

The ETS’s expansion to include more sectors — such as maritime transport and potentially buildings and road transport under EU ETS II — expands the share of emissions subject to carbon pricing. This broadening can further tighten supply and push prices up.

Why EU Carbon Prices Matter Beyond Europe

The EU ETS remains the largest carbon market in the world. According to global carbon pricing data, carbon pricing instruments currently cover about 28% of global greenhouse gas emissions, up from about 24% previously. The EU’s system is a key driver of this trend.

Source: World Bank Report

Source: World Bank Report

Many national and regional carbon markets have prices much lower than the EU’s. This shows differences in climate policies and economic situations. The ETS’s tightening emissions cap, reduced auction volumes, and shifting market sentiment all play roles in supporting higher carbon prices.

Forecasts suggest that prices may continue upward in the years to come, potentially averaging over €100 per tonne by the end of the decade. Meanwhile, the ETS continues to help reduce emissions in key sectors and supports the EU’s broader climate targets.

These price trends and policy developments make the EU carbon market a central piece of Europe’s climate strategy and an important bellwether for global carbon pricing efforts.