The FTSE 100 tumbled as oil raced higher as hopes of a de-escalation in the Middle East faded once again.

On another bleak day for investors, London’s blue chip index closed down 134.67 points or 1.33 per cent at 9972.17.

Crude topped $109 a barrel as Iran dismissed reports of direct talks with Iran.

‘Investors look like they’re fed up with the hot and cold messages around Iran peace talks,’ said Dan Coatsworth, head of markets at AJ Bell. ‘Recent market optimism about a resolution in the Middle East is fading fast.’

Elsewhere, NS&I may face a £400million compensation bill and Next’s boss has warned on prices due to the Iran war.

If you’re reading on the This Is Money app, click here.

Another tough day on financial markets

Labour is pushing up energy bills, says M&S

‘I always forget the last one’: Minister’s investment gaffe

‘I always forget the last one’: Minister’s investment gaffe

Chancellor’s house is ‘built on sand’

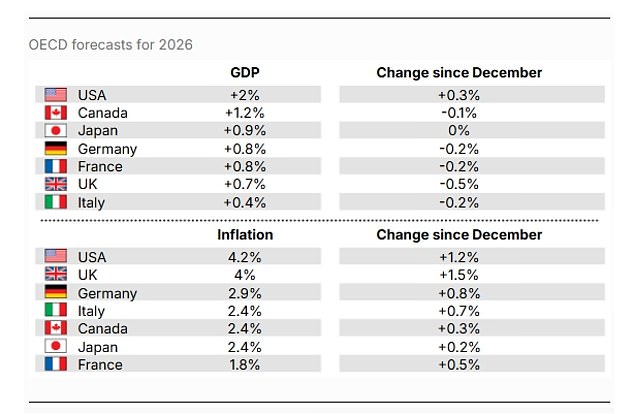

Those OECD forecasts in full

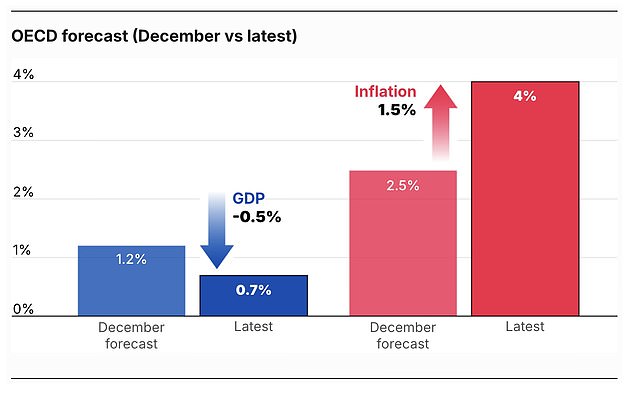

Growth down and inflation up…

Growth down and inflation up…

OECD’s bleak verdict on UK economy

OECD’s bleak verdict on UK economy

FTSE 100 crashes back below 10,000

FTSE 100 crashes back below 10,000

Consumer confidence ‘collapses’

FTSE opens in the red

FTSE opens in the red

Share or comment on this article:

FTSE closes down 134 points as oil rebounds; NS&I in turmoil – MARKETS CLOSE