The UK market has recently faced challenges, with the FTSE 100 index closing lower due to weak trade data from China, highlighting global economic interdependencies. In such a climate, investors often look beyond established giants to explore opportunities in smaller companies. While the term “penny stocks” may seem outdated, these investments can offer compelling possibilities for those seeking affordability and potential growth by focusing on firms with solid financial foundations.

Name

Share Price

Market Cap

Financial Health Rating

Foresight Group Holdings (LSE:FSG)

£3.545

£399.88M

★★★★★★

On the Beach Group (LSE:OTB)

£1.634

£236.77M

★★★★★★

Keystone Law Group (AIM:KEYS)

£4.70

£149.07M

★★★★★★

Focusrite (AIM:TUNE)

£1.70

£97.27M

★★★★★☆

Ingenta (AIM:ING)

£0.90

£13.36M

★★★★★★

Integrated Diagnostics Holdings (LSE:IDHC)

$0.56

$319.73M

★★★★★☆

Spectra Systems (AIM:SPSY)

£1.30

£62.04M

★★★★★☆

BTG Consulting (AIM:BTG)

£1.185

£190.7M

★★★★★☆

Churchill China (AIM:CHH)

£2.931

£32.99M

★★★★★★

ME Group International (LSE:MEGP)

£1.364

£532.3M

★★★★★★

Click here to see the full list of 293 stocks from our UK Penny Stocks screener.

Here’s a peek at a few of the choices from the screener.

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Panthera Resources PLC focuses on the exploration and development of gold projects in India and West Africa, with a market cap of £54.21 million.

Operations: Panthera Resources PLC has not reported any revenue segments.

Market Cap: £54.21M

Panthera Resources PLC, a pre-revenue company with a market cap of £54.21 million, focuses on gold exploration in India and West Africa. Recent drilling at the Bido Project in Burkina Faso showed promising results, highlighting potential growth prospects despite past delays due to equipment issues. Financially, Panthera remains debt-free but faces challenges with less than one year of cash runway and ongoing unprofitability, reporting a net loss of US$1.35 million for the half-year ending September 2025. The company’s experienced board provides stability; however, its negative return on equity reflects current operational struggles typical in early-stage mining ventures.

AIM:PAT Financial Position Analysis as at Mar 2026

AIM:PAT Financial Position Analysis as at Mar 2026

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Cornish Metals plc focuses on acquiring, evaluating, exploring, and developing mineral properties in the United Kingdom with a market cap of £132.99 million.

Story continues

Operations: Cornish Metals plc does not report any specific revenue segments.

Market Cap: £132.99M

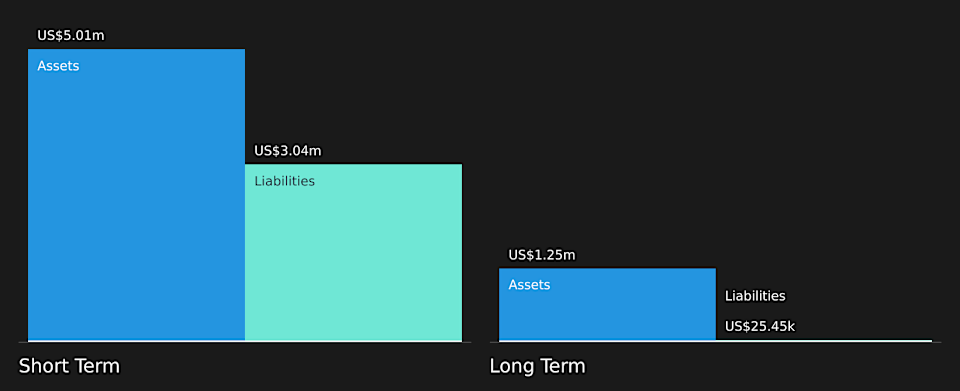

Cornish Metals plc, with a market cap of £132.99 million, is pre-revenue and focuses on mineral exploration in the UK. Despite past earnings declines, the company maintains a strong financial position with CA$64.5M in short-term assets exceeding its liabilities and no debt burden. Recent updates highlight significant progress at South Crofty, including shaft refurbishments and mine dewatering efforts scheduled for completion by early 2027. The first tin production remains on track for mid-2028. While volatility persists in its share price, Cornish Metals benefits from an experienced management team navigating complex project developments effectively without recent shareholder dilution concerns.

AIM:TIN Financial Position Analysis as at Mar 2026

AIM:TIN Financial Position Analysis as at Mar 2026

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Watches of Switzerland Group PLC is a retailer specializing in luxury watches and jewelry across the United Kingdom, Europe, and the United States, with a market cap of £1.06 billion.

Operations: The company’s revenue segments include £872.4 million from the UK & Europe.

Market Cap: £1.06B

Watches of Switzerland Group PLC, with a market cap of £1.06 billion, has shown robust earnings growth of 68.6% over the past year, surpassing industry averages. Despite a large one-off loss impacting recent results, its financial health remains solid with short-term assets exceeding both short and long-term liabilities. The company’s debt management is commendable, evidenced by a reduced debt to equity ratio from 61.6% to 29.7% over five years and strong cash flow coverage of debt at 117.8%. Recent board changes include the appointment of Paul Edgecliffe-Johnson as Non-Executive Director, enhancing governance expertise amidst strategic expansions like acquiring Deutsch & Deutsch.

LSE:WOSG Debt to Equity History and Analysis as at Mar 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AIM:PAT AIM:TIN and LSE:WOSG.

This article was originally published by Simply Wall St.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com