Amidst a backdrop of global economic challenges, the UK market has seen its major indices, such as the FTSE 100 and FTSE 250, falter due to weak trade data from China. This environment underscores the importance of identifying resilient small-cap stocks that can thrive despite broader market uncertainties, making them potential undiscovered gems for investors in April 2026.

Top 10 Undiscovered Gems With Strong Fundamentals In The United KingdomNameDebt To EquityRevenue GrowthEarnings GrowthHealth RatingGoodwin24.30%12.58%22.87%★★★★★★Andrews Sykes GroupNA2.01%5.12%★★★★★★BioPharma CreditNA5.72%5.22%★★★★★★Georgia CapitalNA13.71%21.08%★★★★★★Vectron SystemsNA2.48%28.82%★★★★★★Nationwide Building Society282.42%9.69%21.24%★★★★★☆FW Thorpe2.19%9.09%11.33%★★★★★☆Foresight Environmental InfrastructureNA-24.80%-27.25%★★★★★☆Strategic MineralsNA4.81%-40.63%★★★★★☆Distribution Finance Capital Holdings12.97%42.17%59.43%★★★★☆☆

Let’s dive into some prime choices out of from the screener.

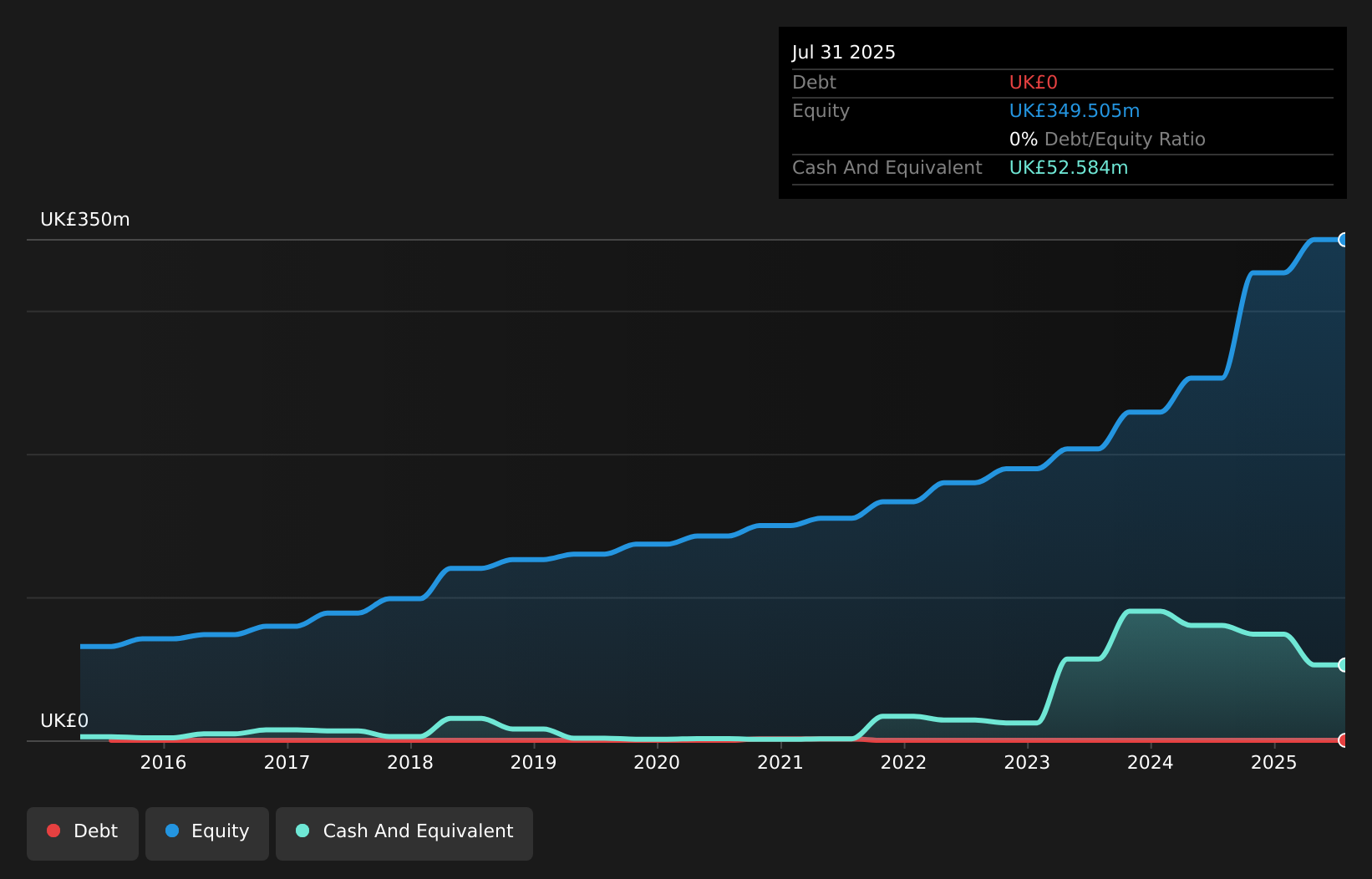

Simply Wall St Value Rating: ★★★★★★

Overview: B.P. Marsh & Partners PLC focuses on investing in early-stage and SME financial services intermediary businesses both in the United Kingdom and internationally, with a market cap of £235.11 million.

Operations: Revenue is primarily generated from consultancy services and trading investments in financial services, totaling £118.87 million.

B.P. Marsh & Partners, a nimble player in the financial sector, stands out with its impressive earnings growth of 94.8% over the past year, surpassing the Capital Markets industry’s 16.1%. Trading at a substantial discount of 66.9% below its estimated fair value, it offers intriguing potential for investors seeking undervalued opportunities. The company is debt-free and boasts high-quality non-cash earnings, enhancing its financial stability despite not being free cash flow positive currently. Looking ahead, while earnings are expected to dip by an average of 0.8% annually over the next three years, strategic dividend distributions totaling £5 million for FY2027 may offer some investor reassurance amidst these projections.

AIM:BPM Debt to Equity as at Apr 2026

AIM:BPM Debt to Equity as at Apr 2026

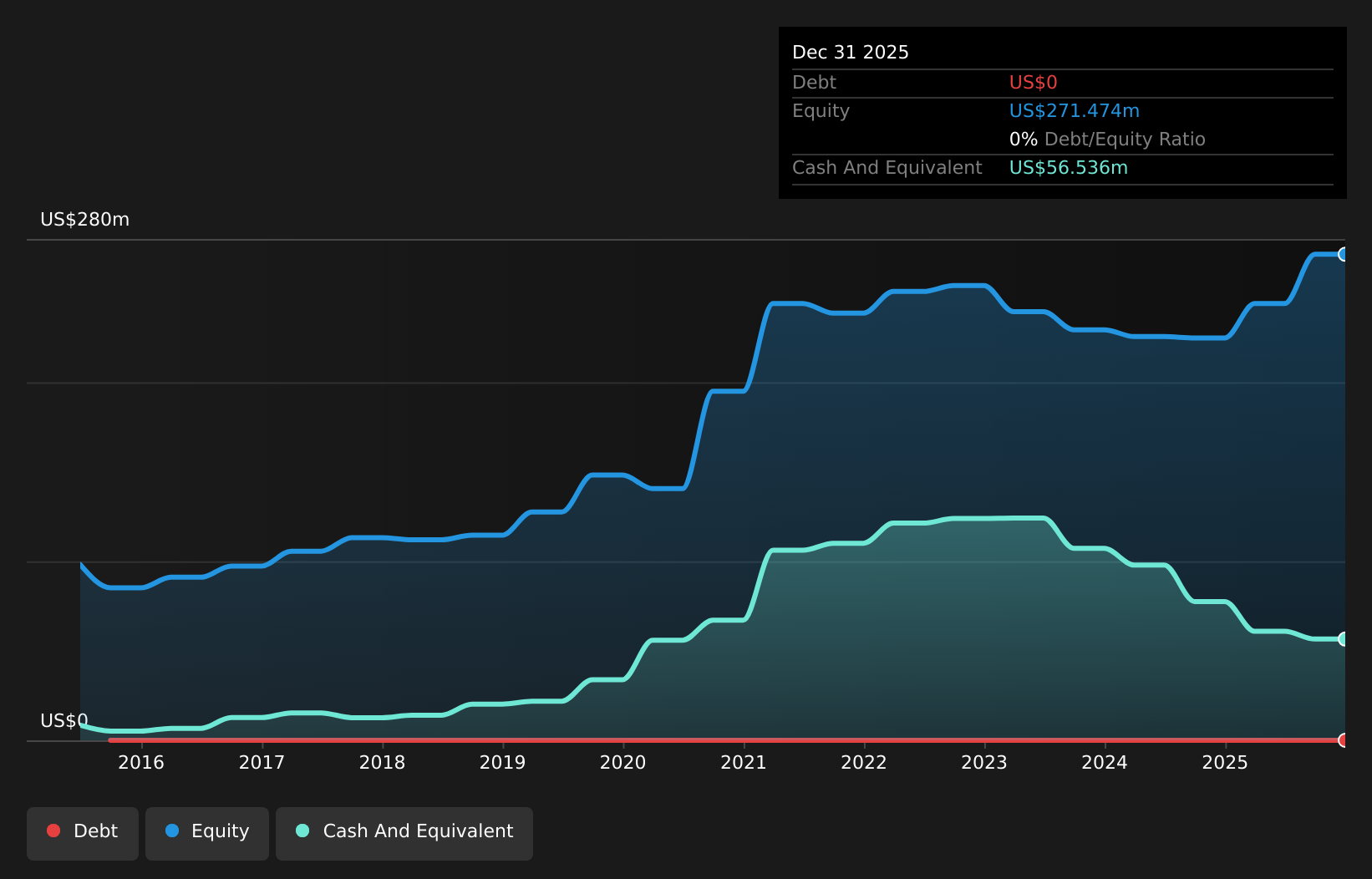

Simply Wall St Value Rating: ★★★★★★

Overview: Sylvania Platinum Limited, along with its subsidiaries, focuses on the retreatment of platinum group metals (PGM) bearing chrome tailings materials in South Africa and has a market capitalization of £238.24 million.

Operations: The primary revenue stream for Sylvania Platinum comes from its Sylvania Dump Operations (SDO), generating $155.55 million. Segment adjustments account for a minor $0.97 million in the financials, reflecting the company’s focus on efficient operations within its core business segment.

Sylvania Platinum, a dynamic player in the mining sector, has shown impressive earnings growth of 227.8%, outpacing the industry average of 126.8%. Trading at nearly 90% below its estimated fair value, it offers an intriguing prospect for investors. Despite recent insider selling and share price volatility over the past three months, Sylvania remains debt-free with high-quality earnings. The company revised its production guidance upwards to between 90,000 and 93,000 PGM ounces for fiscal year 2026 and declared an interim dividend of £0.02 per share, signaling confidence in its financial health and operational outlook.

AIM:SLP Debt to Equity as at Apr 2026

AIM:SLP Debt to Equity as at Apr 2026

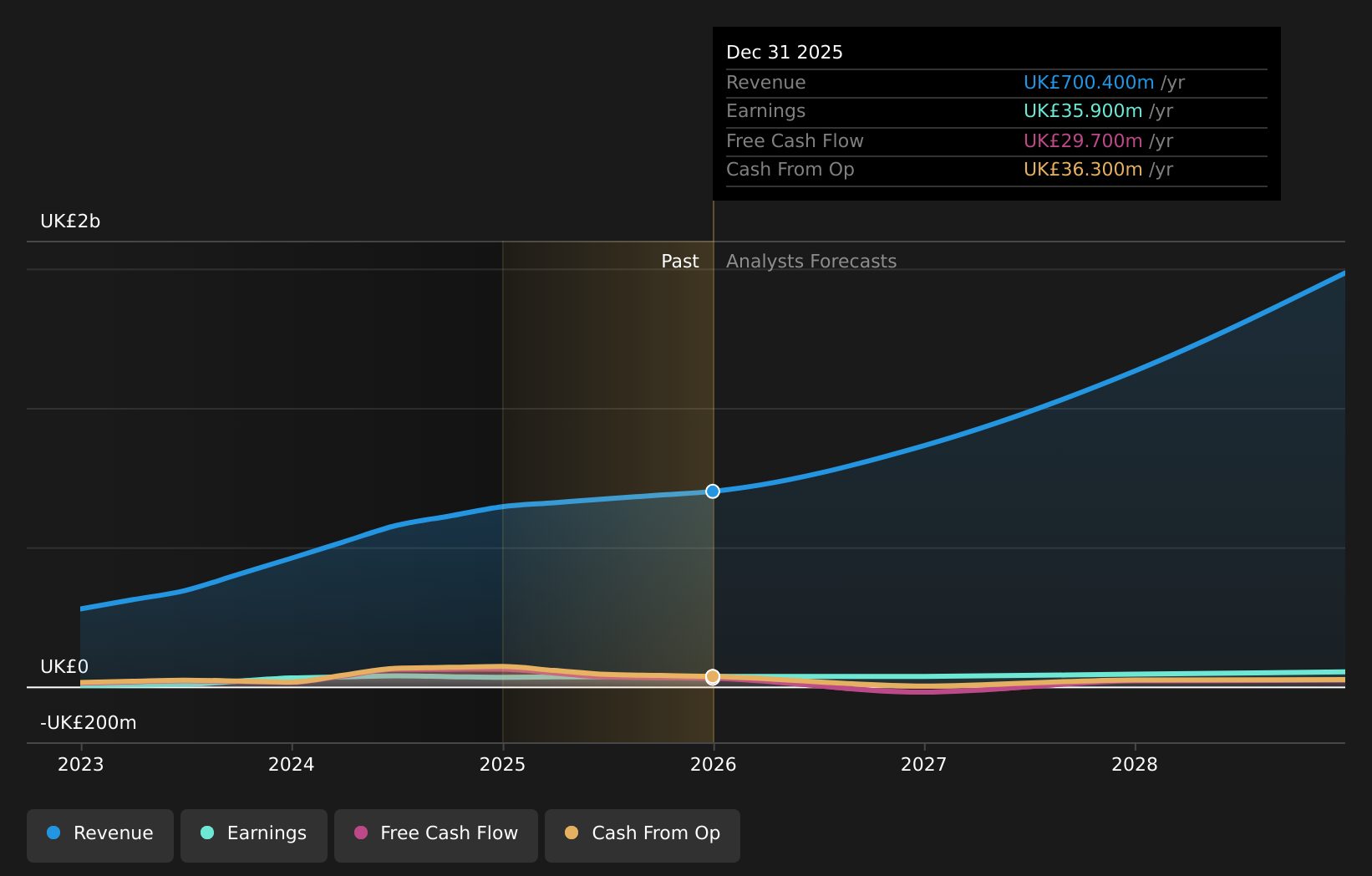

Simply Wall St Value Rating: ★★★★★☆

Overview: Yü Group PLC, with a market cap of £295.63 million, operates through its subsidiaries to supply energy and utility solutions primarily in the United Kingdom.

Operations: The company’s revenue is primarily derived from its Retail segment, which contributes £700 million, while the Smart and Metering Assets segments add £10.90 million and £1.80 million respectively. Intra-segment Trading results in a reduction of £12.30 million from the total revenue.

Yü Group, a dynamic player in the UK energy sector, has shown impressive financial resilience. Over the past five years, its debt to equity ratio rose to 10.5%, but it maintains more cash than total debt, highlighting strong fiscal health. The company reported £700.4 million in sales for 2025, up from £645.5 million the previous year, with net income reaching £35.9 million compared to £33.5 million priorly. Its earnings per share increased from GBP 2 to GBP 2.14, reflecting robust performance amidst industry challenges and positioning it well for future growth prospects with projected revenue between £850-£875 million for 2026.

AIM:YU. Earnings and Revenue Growth as at Apr 2026Make It HappenSearching for a Fresh Perspective?

AIM:YU. Earnings and Revenue Growth as at Apr 2026Make It HappenSearching for a Fresh Perspective?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com