![]() Company Logo

Company Logo

The UK quick commerce market presents opportunities for growth through integration with supermarket chains, leveraging delivery platform partnerships, enhancing omnichannel strategies, and focusing on profitability via tiered services, loyalty programs, and retail media. Consolidation and logistics efficiency are pivotal.

United Kingdom Quick Commerce Market

United Kingdom Quick Commerce Market · GlobeNewswire Inc.

United Kingdom Quick Commerce Market · GlobeNewswire Inc.

Dublin, April 17, 2026 (GLOBE NEWSWIRE) — The “United Kingdom Quick Commerce Market Size & Forecast by Value and Volume Across 100+ KPIs by Product Type, Payment Mode, Age Group, Location, Business Model, and Delivery Time – Databook Q1 2026 Update” report has been added to ResearchAndMarkets.com’s offering.

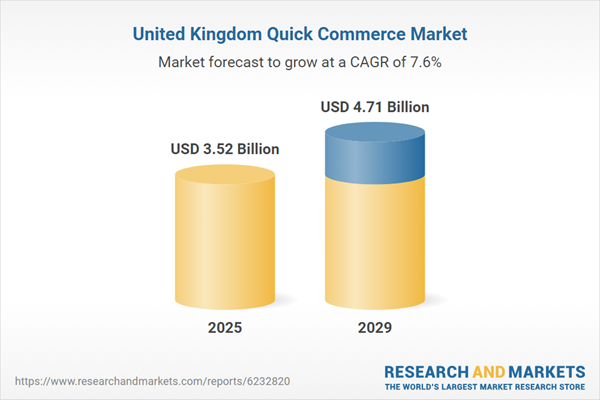

The quick commerce market in United Kingdom is expected to grow by 7.9% annually, reaching US$3.52 trillion by 2025. The quick commerce market in the region has experienced robust growth during 2020-2024, achieving a CAGR of 7.2%. This upward trajectory is expected to continue, with the market forecast to grow at a CAGR of 7.6% from 2025 to 2029. By the end of 2029, the quick commerce market is projected to expand from its 2024 value of US$3.26 trillion to approximately US$4.71 trillion.

Over the next 2-4 years, competition will be shaped by scale efficiencies, data sharing, and retail media monetisation. Quick commerce will increasingly integrate into supermarket loyalty programs and app ecosystems, blurring boundaries between e-commerce and in-store shopping. New entrants are expected mainly from logistics technology and last-mile service providers, not consumer-facing apps. Market share will consolidate around fewer, multi-service platforms that strike a balance between speed and profitability, leaving limited space for standalone startups.

Current State of the Market

The UK quick commerce sector has transitioned from rapid expansion to consolidation. Following the exit of pure-play operators such as Getir and Gorillas in 2024, the market has stabilised around established grocery retailers and multi-category delivery platforms. Rapid grocery is now positioned as a mainstream convenience channel, rather than a standalone segment, with major supermarkets such as Tesco, Co-op, Sainsbury’s, Asda, Morrisons, and Waitrose integrating same-hour delivery into their omnichannel models.

Delivery platforms such as Deliveroo, Uber Eats, and Just Eat function as aggregators, collaborating with supermarkets and convenience store chains to reach over 80% of the UK’s urban population. Competitive dynamics have moved away from network expansion toward improving operational efficiency, ensuring service reliability, and integrating more deeply with retailer loyalty programs and ecosystems.

Story continues

Key Players and New Entrants

Tesco’s Whoosh and Ocado Zoom lead the retailer-driven segment, complemented by Co-op’s multi-platform collaborations and Morrisons’ tie-up with Deliveroo. Deliveroo remains the most diversified operator, partnering with both local retailers and national chains. Uber Eats and Just Eat have extended their reach into grocery delivery through alliances with Sainsbury’s, Asda, and Co-op.

While several international players have withdrawn from the market, new domestic initiatives such as Sainsbury’s Chop Chop and regional convenience store partnerships are gaining traction in major cities. Emerging startups are increasingly focused on technology development and white-label fulfillment solutions rather than running dark-store networks, signalling a broader move toward enabling services instead of direct-to-consumer operations.

Key Trends & Drivers

Market consolidates around supermarkets and food-delivery platforms.

The UK quick commerce market has moved from a fragmented, venture-backed model to one dominated by established grocers and large delivery platforms. Pure-play rapid players are retrenching: Getir confirmed in April 2024 that it would exit the UK (along with Germany and the Netherlands) as part of a restructuring.

On-demand grocery is now a sizable but stable channel, with around 80 million orders worth more than £2 billion annually, largely fulfilled by platforms such as Deliveroo, Uber Eats, and Eat, which work with major grocers.

The UK grocery sector operates on thin margins and is highly competitive, with discounters and private-label ranges putting pressure on prices. Rising input costs and volatile food inflation have tightened profitability, forcing operators to reassess loss-making ultra-fast models.

After the pandemic-fueled boom, online grocery sales have leveled off, increasing by 3.7% to £19.6 billion in 2023. Market penetration dipped slightly to around 10%, reflecting a shift from rapid growth toward a more steady integration with traditional brick-and-mortar retail.

Established supermarkets (Tesco, Co-op, Morrisons, Sainsbury’s, Asda) have brand trust, dense store networks, and existing ecommerce operations, allowing them to absorb quick commerce into broader omnichannel strategies at lower marginal cost than standalone dark-store players.

Market concentration is likely to increase, with rapid grocery largely controlled by a handful of supermarket-platform combinations (e.g., Tesco-Whoosh, Co-op-Deliveroo/Eat/Uber Eats, Morrisons-Deliveroo, Ocado-Zoom).

Retailers deepen omnichannel partnerships to monetise store networks

UK grocers are turning existing convenience and supermarket stores into local fulfilment hubs, combining in-house quick-commerce propositions with white-label and marketplace partnerships.

Co-op has pushed rapid delivery through multiple avenues: 24-hour online grocery with Deliveroo, Eat and Uber Eats; participation in Eat’s new JET Go delivery-as-a-service offer; and most recently becoming the first grocer on Deliveroo’s white-label “Deliveroo Express” solution, with a stated aim to reach 86% of the population online and target around 30% of the rapid grocery market. Morrisons is expanding its Deliveroo-based delivery service from the Morrisons Daily network, promising under-30-minute deliveries from 500 convenience stores.

Store networks remain the core asset base in the UK grocery. As growth in traditional weekly online shops slows, retailers are seeking incremental revenue from “top-up” and mission-based baskets served from nearby stores.

Delivery promise normalises from ‘ultra-fast’ to ‘reliably quick’ and same-day

The initial “10-minute delivery” proposition has given way to more pragmatic service levels: 20-60-minute rapid delivery from local stores and a growing layer of same-day slots from central fulfilment. Tesco Whoosh markets same-day delivery “from as little as 20 minutes” for a curated range of essentials, while operational details typically refer to deliveries in around 30 minutes.

Ocado has layered on “Express It” same-day slots that customers can book by late morning for delivery later that same day, alongside its faster Ocado Zoom offer, which delivers a narrower range of items in under 60 minutes. On-demand grocery as a channel has reached scale but is no longer positioned solely as ultra-fast; it is part of a broader spectrum from sub-hour top-ups to same-day and next-day baskets.

Ultra-fast delivery requires dense dark-store networks and high rider utilisation, which proved hard to sustain in the UK’s cost and demand environment, especially once pandemic-era growth normalised and investor capital tightened. UK consumers are highly price-sensitive in the current inflationary environment; they will pay a premium for convenience, but not at any cost, which favors slightly slower, batched delivery models with lower fees.

Report Scope

United Kingdom Quick Commerce Market Size and Growth Dynamics

Gross Merchandise Value

Gross Merchandise Volume

Average Order Value

Order Frequency per Year

United Kingdom Quick Commerce Market Segmentation by Product Type

United Kingdom Quick Commerce Market Segmentation by Payment Mode

United Kingdom Quick Commerce Market Segmentation by Age Group

Gen Z (15-25)

Millennials (26-39)

Gen X (40-55)

Baby Boomers (Above 55)

United Kingdom Quick Commerce Market Segmentation by Location Tier

Tier 1 Cities

Tier 2 Cities

Tier 3 Cities

United Kingdom Quick Commerce Market Segmentation by Business Model

United Kingdom Quick Commerce Market Segmentation by Delivery Time

Delivery in 30 Minutes

Delivery 30-60 Minutes

Delivery in 3 Hours

United Kingdom Quick Commerce Consumer Behavior and Demographics

Average Subscription Uptake by Age Group

Average Subscription Uptake by Location Tier

Average Subscription Uptake

Average Delivery Time

United Kingdom Quick Commerce Revenue Structure and Composition

Advertising Revenue

Delivery Fee Revenue

Subscription Revenue

United Kingdom Quick Commerce Operational Metrics by Product Type

Gross Merchandise Value by Product Type

Gross Merchandise Volume by Product Type

Average Order Value by Product Type

Order Frequency by Product Type

United Kingdom Quick Commerce Operational Metrics by Payment Mode

Gross Merchandise Value by Payment Mode

Gross Merchandise Volume by Payment Mode

Average Order Value by Payment Mode

United Kingdom Quick Commerce Operational Metrics by Age Group

Gross Merchandise Value by Age Group

Gross Merchandise Volume by Age Group

Average Order Value by Age Group

United Kingdom Quick Commerce Operational Metrics by Location Tier

Gross Merchandise Value by Location Tier

Gross Merchandise Volume by Location Tier

Average Order Value by Location Tier

Order Frequency by Location Tier

United Kingdom Quick Commerce Operational Metrics by Business Model

Gross Merchandise Value by Business Model

Gross Merchandise Volume by Business Model

Average Order Value by Business Model

United Kingdom Quick Commerce Operational Metrics by Delivery Time

Gross Merchandise Value by Delivery Time

Gross Merchandise Volume by Delivery Time

Average Order Value by Delivery Time

Order Frequency by Delivery Time

Key Attributes:

Report Attribute

Details

No. of Pages

140

Forecast Period

2025 – 2029

Estimated Market Value (USD) in 2025

$3.52 Billion

Forecasted Market Value (USD) by 2029

$4.71 Billion

Compound Annual Growth Rate

7.6%

Regions Covered

United Kingdom

For more information about this report visit https://www.researchandmarkets.com/r/n7ii6d

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900