The United Kingdom’s financial markets have recently been influenced by global economic developments, with the FTSE 100 experiencing a downturn following weak trade data from China. In such times, investors often look for opportunities that offer potential growth at lower price points. Penny stocks, though an older term, still highlight smaller or newer companies that can provide value and growth potential when supported by solid financials.

Name

Share Price

Market Cap

Financial Health Rating

BRCK Group (AIM:BRCK)

£0.536

£172.78M

★★★★★☆

Foresight Group Holdings (LSE:FSG)

£4.07

£459.55M

★★★★★★

Keystone Law Group (AIM:KEYS)

£4.775

£151.45M

★★★★★★

Hollywood Bowl Group (LSE:BOWL)

£2.67

£447.58M

★★★★☆☆

Ingenta (AIM:ING)

£1.14

£17.21M

★★★★★★

System1 Group (AIM:SYS1)

£3.00

£38.07M

★★★★★★

Integrated Diagnostics Holdings (LSE:IDHC)

$0.61

$354.61M

★★★★★☆

Gulf Keystone Petroleum (LSE:GKP)

£1.842

£400.53M

★★★★★★

BTG Consulting (AIM:BTG)

£1.185

£191.03M

★★★★★☆

Norman Broadbent (AIM:NBB)

£2.21

£4.07M

★★★★★★

Click here to see the full list of 274 stocks from our UK Penny Stocks screener.

Let’s uncover some gems from our specialized screener.

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: BTG Consulting plc offers business recovery, financial advisory, and property services consultancy in the United Kingdom, with a market cap of £191.03 million.

Operations: The company’s revenue is derived from two main segments: Property Advisory, which contributes £48 million, and Business Recovery and Advisory, generating £111.4 million.

Market Cap: £191.03M

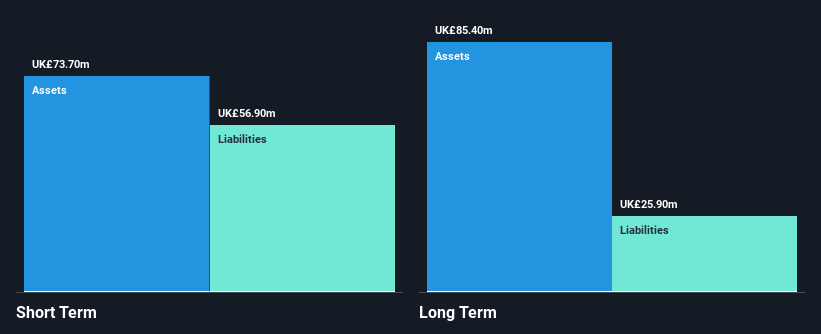

BTG Consulting plc, formerly Begbies Traynor Group plc, presents a mixed picture in the penny stock arena. With a market cap of £191.03 million and revenue from Property Advisory (£48M) and Business Recovery (£111.4M), its financial health is underscored by short-term assets exceeding both short- and long-term liabilities. Despite a low return on equity (12.2%), BTG offers a stable dividend yield of 3.71% and demonstrates strong debt management with interest payments well-covered by EBIT (13.1x). Recent earnings growth of 296% outpaces industry averages, though impacted by an £8.5M one-off loss last year, highlighting volatility concerns amidst favorable analyst expectations for future price appreciation.

AIM:BTG Financial Position Analysis as at Apr 2026

AIM:BTG Financial Position Analysis as at Apr 2026

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Michelmersh Brick Holdings plc, with a market cap of £71.52 million, manufactures and sells bricks and brick prefabricated products in the United Kingdom and Europe.

Operations: Michelmersh Brick Holdings generates revenue through its manufacturing and sales operations in the United Kingdom and Europe.

Market Cap: £71.52M

Michelmersh Brick Holdings plc, with a market cap of £71.52 million, shows mixed signals in the penny stock landscape. Recent earnings reveal a decline in net income to £3.65 million from £6.1 million last year, reflecting challenges despite stable revenue generation (£68.9M). The company’s financial stability is bolstered by short-term assets exceeding liabilities and satisfactory debt management (net debt to equity at 0.8%). However, low return on equity (3.9%) and declining profit margins (5.3% from 8.7%) raise concerns about profitability sustainability, while experienced board leadership contrasts with an inexperienced management team averaging 1.3 years tenure.

AIM:MBH Debt to Equity History and Analysis as at Apr 2026

AIM:MBH Debt to Equity History and Analysis as at Apr 2026

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: M&C Saatchi plc is a global advertising and marketing communications company operating in the UK, Europe, the Middle East, Asia Pacific, and the Americas with a market cap of £144.99 million.

Operations: The company does not report specific revenue segments.

Market Cap: £144.99M

M&C Saatchi plc, with a market cap of £144.99 million, presents a complex picture in the penny stock domain. Despite reducing its debt-to-equity ratio significantly over five years and having short-term assets exceed liabilities, the company remains unprofitable with a negative return on equity (-5.77%). Recent earnings show sales of £347.4 million but a net loss of £2.23 million for 2025, contrasting with last year’s profit. The board’s inexperience (1.8 years average tenure) and leadership changes add uncertainty, while ongoing share repurchases and strategic focus on growth could offer potential upside amidst volatility concerns.

AIM:SAA Financial Position Analysis as at Apr 2026

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AIM:BTG AIM:MBH and AIM:SAA.

This article was originally published by Simply Wall St.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com