For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

In contrast to all that, many investors prefer to focus on companies like California BanCorp (NASDAQ:BCAL), which has not only revenues, but also profits. Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

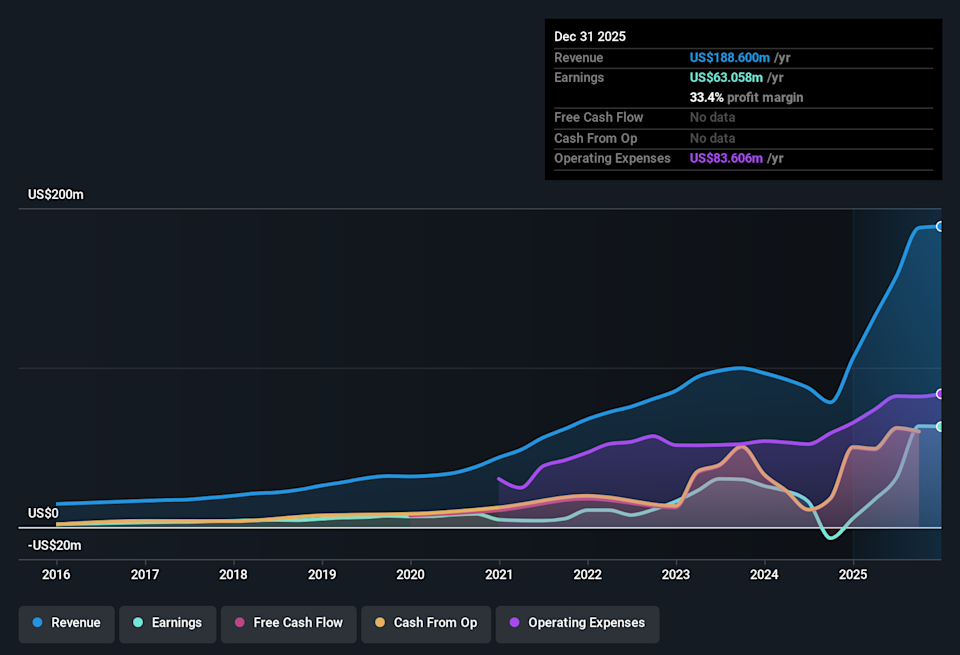

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. That means EPS growth is considered a real positive by most successful long-term investors. It certainly is nice to see that California BanCorp has managed to grow EPS by 29% per year over three years. If growth like this continues on into the future, then shareholders will have plenty to smile about.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it’s a great way for a company to maintain a competitive advantage in the market. Not all of California BanCorp’s revenue this year is revenue from operations, so keep in mind the revenue and margin numbers used in this article might not be the best representation of the underlying business. EBIT margins for California BanCorp remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 78% to US$189m. That’s progress.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

NasdaqCM:BCAL Earnings and Revenue History February 13th 2026

NasdaqCM:BCAL Earnings and Revenue History February 13th 2026

View our latest analysis for California BanCorp

Fortunately, we’ve got access to analyst forecasts of California BanCorp’s future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That’s because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don’t know the exact thinking behind their acquisitions.

Story Continues

First and foremost; there we saw no insiders sell California BanCorp shares in the last year. But the really good news is that Independent Director David Volk spent US$503k buying stock, at an average price of around US$18.64. Purchases like this can offer an insight into the faith of the company’s management – and it seems to be all positive.

The good news, alongside the insider buying, for California BanCorp bulls is that insiders (collectively) have a meaningful investment in the stock. Notably, they have an enviable stake in the company, worth US$107m. That equates to 18% of the company, making insiders powerful and aligned with other shareholders. Looking very optimistic for investors.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That’s because California BanCorp’s CEO, Dave Rainer, is paid at a relatively modest level when compared to other CEOs for companies of this size. For companies with market capitalisations between US$400m and US$1.6b, like California BanCorp, the median CEO pay is around US$3.3m.

California BanCorp offered total compensation worth US$1.7m to its CEO in the year to December 2024. That seems pretty reasonable, especially given it’s below the median for similar sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it’s reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of a culture of integrity, in a broader sense.

You can’t deny that California BanCorp has grown its earnings per share at a very impressive rate. That’s attractive. Better still, insiders own a large chunk of the company and one has even been buying more shares. These things considered, this is one stock worth watching. However, before you get too excited we’ve discovered 1 warning sign for California BanCorp that you should be aware of.

The good news is that California BanCorp is not the only stock with insider buying. Here’s a list of small cap, undervalued companies in the US with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.