What Banc of California’s Recent Share Performance Signals for Investors

Banc of California (BANC) has drawn fresh attention after a recent pullback, with the stock down about 4% over the past day and 15% over the past month. This decline is prompting investors to reassess its current valuation.

See our latest analysis for Banc of California.

While the 30 day share price return of negative 15% and year to date share price return of negative 12.03% point to fading near term momentum, the 1 year total shareholder return of 27.24% shows that longer term holders have still seen a positive outcome from the current US$17.11 level.

If recent banking volatility has you rethinking where you look for opportunities, it could be a good time to broaden your search with our screener of 20 top founder-led companies.

With Banc of California trading at US$17.11 and sitting at what looks like a sizeable discount to some valuation estimates, you have to ask: is this a genuine mispricing, or is the market already factoring in future growth?

Most Popular Narrative: 28% Undervalued

With Banc of California last closing at $17.11 and the most followed narrative pointing to a fair value of about $23.77 using a 7.8% discount rate, the gap between price and narrative value is front and center for investors.

The successful merger integration with Pacific Western Bank is unlocking cost synergies, revenue cross sell opportunities, and scale benefits, which are already contributing to tangible book value expansion and margin improvement and are likely to further boost future profitability.

Curious what kind of revenue lift, margin profile, and future earnings power would need to line up to support that higher fair value? The most followed narrative runs through a detailed set of growth and profitability assumptions, plus the valuation multiple required for those numbers to make sense. The full piece connects those moving parts into one clear story around that $23.77 mark.

Result: Fair Value of $23.77 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still real swing factors here, especially if Southern California commercial real estate weakens or deposit competition squeezes margins harder than analysts currently assume.

Find out about the key risks to this Banc of California narrative.

Another Angle On Banc of California’s Valuation

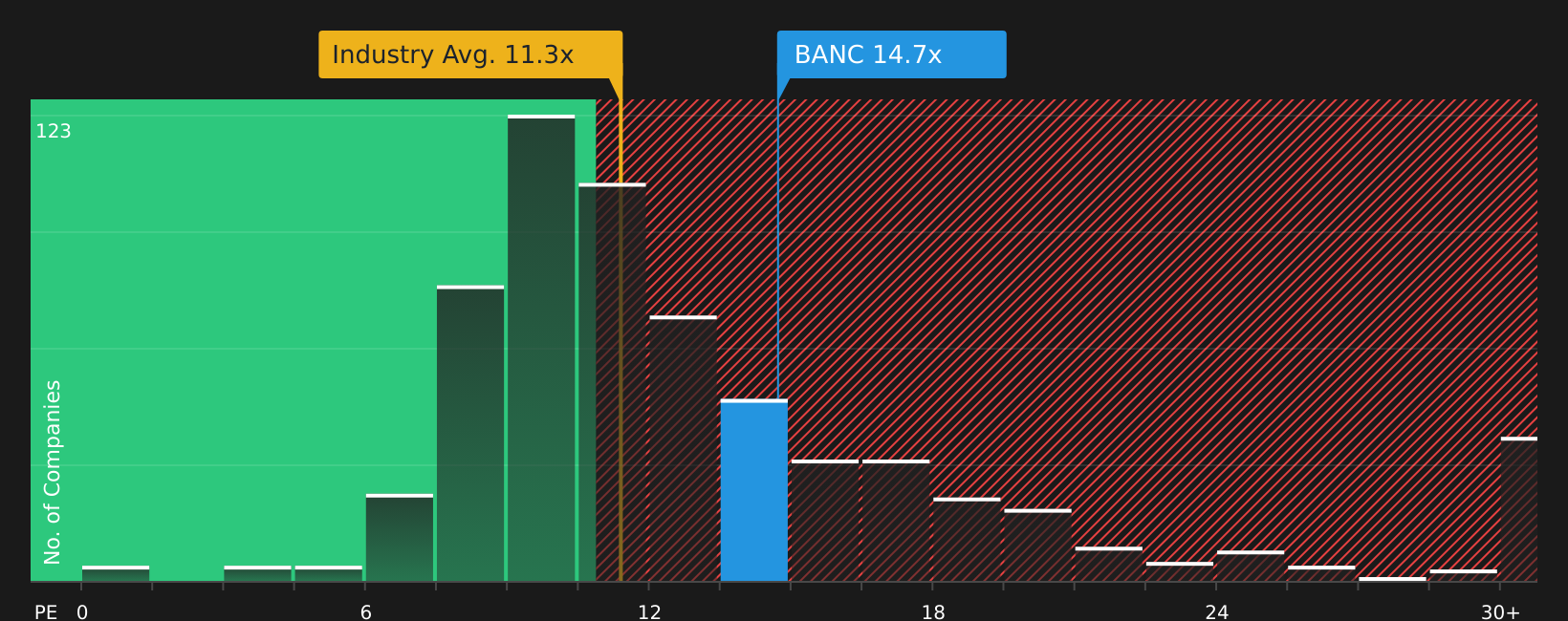

While the narratives and price targets suggest BANC looks undervalued, the simple P/E comparison tells a tighter story. The current P/E of 14.1x sits above both the US Banks industry at 11.4x and peers at 12.2x, yet below a fair ratio estimate of 16x. Is that a valuation cushion or a warning sign if sentiment cools?

See what the numbers say about this price — find out in our valuation breakdown.

NYSE:BANC P/E Ratio as at Mar 2026Next Steps

NYSE:BANC P/E Ratio as at Mar 2026Next Steps

If this mix of caution and optimism leaves you undecided, do not wait for the crowd to tell you what to think. Instead, review the 4 key rewards and decide whether those positives justify a closer look for your own portfolio.

Looking for more investment ideas?

If you are on the fence about BANC, do not sit on your hands. Use this moment to line up a few fresh ideas before the next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Banc of California might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com