In recent weeks, CBRE Group has moved to foreclose on two loan‑backed Oakland apartment properties after borrower defaults, while its latest quarterly results showed revenue and core EPS growth but a slight revenue shortfall versus analyst expectations. This mix of distressed multifamily exposure and solid, yet imperfect, quarterly performance has sharpened attention on how CBRE balances sector risks with its broader services and investment platform. We’ll now examine how concerns about commercial real estate fundamentals, especially in troubled multifamily pockets like Oakland, may influence CBRE’s investment narrative.

The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

CBRE Group Investment Narrative Recap

To own CBRE, you need to believe its diversified services and investment platform can offset pockets of commercial real estate stress and interest rate sensitivity. The Oakland multifamily foreclosures highlight localized credit and asset quality risks, but they do not appear to alter the main near term catalyst, which remains the company’s execution on its realignment toward more resilient, fee based businesses. The biggest current risk still centers on weaker transaction volumes if commercial real estate fundamentals deteriorate further.

The most relevant recent announcement is CBRE’s Q4 2025 report, which showed full year revenue of US$40,550 million and earnings of US$1,157 million, but a slight quarterly revenue miss versus analyst expectations. Against the backdrop of distressed Oakland assets and softer sector sentiment, that mix of growth and minor underperformance puts more weight on CBRE’s plan to lean into resilient segments like project management and building operations as key drivers of the next phase of earnings progress.

Yet behind that broader story, investors should also be aware of the risk that weaker capital markets and leasing activity could…

Read the full narrative on CBRE Group (it’s free!)

CBRE Group’s narrative projects $50.0 billion revenue and $2.3 billion earnings by 2028. This requires 9.5% yearly revenue growth and roughly a $1.2 billion earnings increase from $1.1 billion today.

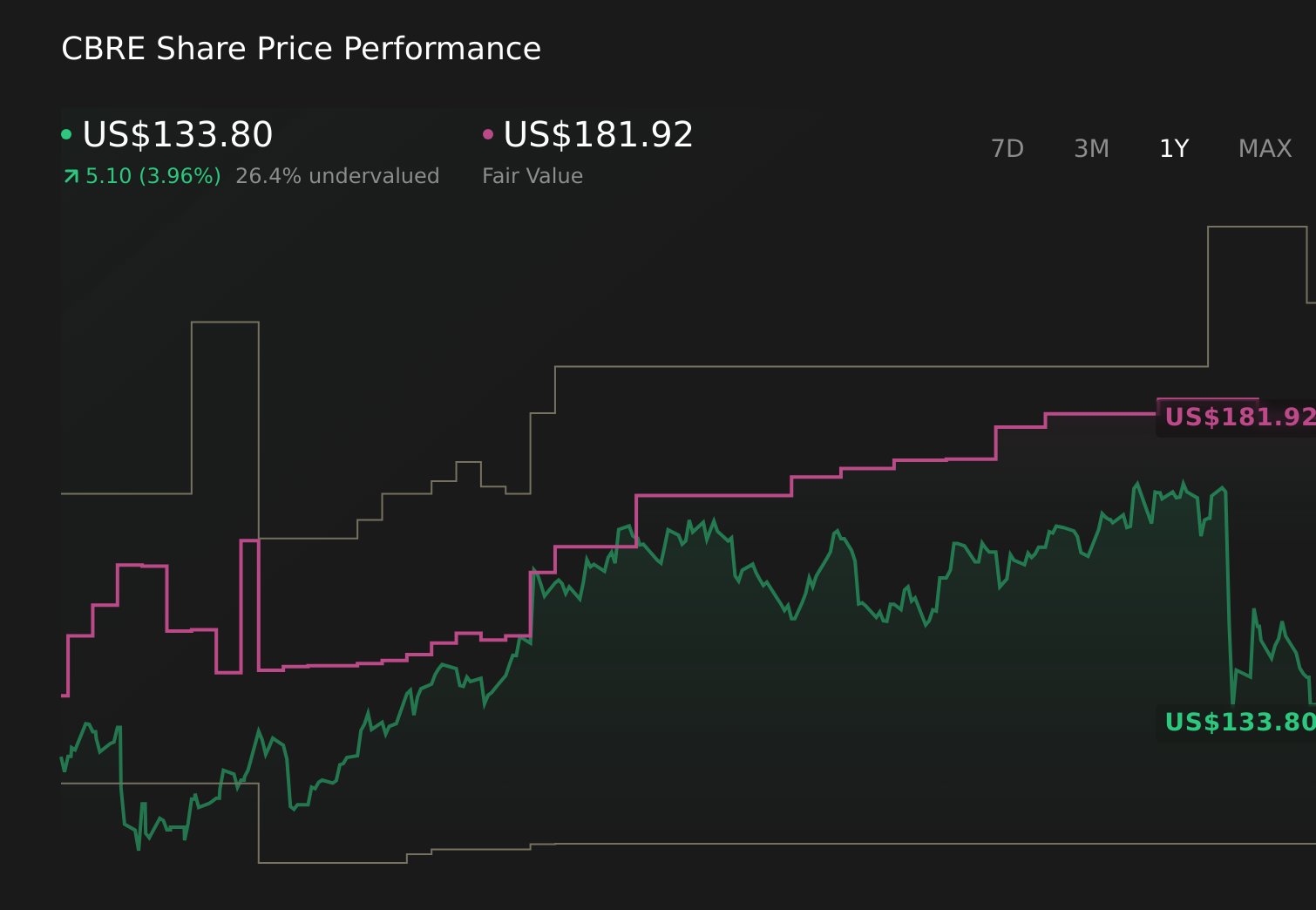

Uncover how CBRE Group’s forecasts yield a $181.92 fair value, a 36% upside to its current price.

Exploring Other Perspectives CBRE 1-Year Stock Price Chart

CBRE 1-Year Stock Price Chart

While consensus focuses on CBRE’s shift toward resilient fees, the most pessimistic analysts already assumed only about 7.4 percent annual revenue growth and roughly US$2.1 billion of earnings by 2028, reminding you that views on how distressed markets and softer transaction volumes could reshape the story can differ sharply and may need updating after news like the Oakland foreclosures.

Explore 2 other fair value estimates on CBRE Group – why the stock might be worth just $157.14!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

Searching For A Fresh Perspective?

The market won’t wait. These fast-moving stocks are hot now. Grab the list before they run:

Capitalize on the AI infrastructure supercycle with our selection of the 35 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.Uncover the next big thing with 32 elite penny stocks that balance risk and reward.Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com