The higher the home price, the more likely an adjustable-rate mortgage is used.

My trusty spreadsheet found another symbol of housing affordability pressures when it peeked at Cotality stats tracking the share of variable-rate mortgages. The yearly stats, dating back to 2019, covered all states and the District of Columbia – except Vermont.

When you rank the states by borrowers’ use of adjustable loans, then slice the scorecard into three groups, you find that adjustable mortgages are most common in 17 states where the median price averages $454,300 median price.

The fewest ARMs are in 17 states, with an average median price of $310,100. That’s a 46% gap.

And adjustable loans were also found where appreciation is stronger: Prices rose 52% over six years in those states with the largest share of adjustable loans, vs. rising 42% since 2019 in states where adjustables are less common.

Plus, contemplate this nugget from Cotality: Nearly half of the mortgages above $1 million in December 2025 had adjustable rates.

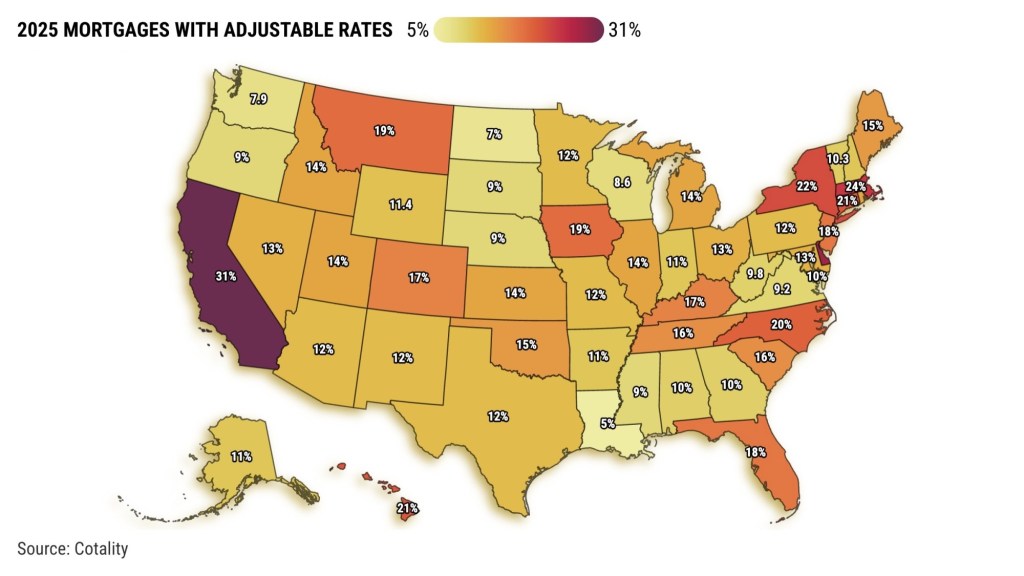

State of adjustment

At 31%, California had the nation’s largest share of adjustable-rate mortgages in 2025.

These borrowers were likely willing to forgo the stability of fixed-rate loans to manage the financial strain of California’s median home price of $759,200, according to Zillow. That price, No. 2 nationally, is up 43% over six years.

Ponder the potential savings an adjustable loan might provide.

Financing that median home with 2025’s average 30-year fixed-rate mortgage, as tracked by Freddie Mac – and assuming a 20% down payment – would cost a hypothetical borrower $3,880 per month.

But last year’s 5.9% average adjustable mortgage rate, as tracked by the California Association of Realtors, created a a $3,600 payment for the same residence.

That’s a $280 a month savings, or 7%.

Price matters

Heavy use of adjustable mortgages was also found in Delaware at 28% ($391,600 median), Massachusetts at 24% ($630,100), Washington state at 24% ($583,500), New York at 22% ($485,400) and Wyoming at 22% ($351,200).

Conversely, adjustable financing was used least frequently in Louisiana, at only 5% of purchases, with a median purchase price of $206,600.

Other adjustable rarities were North Dakota at 7% ($266,000 median) plus four at 9%: Mississippi ($185,900), Nebraska ($261,600), Oregon ($487,500), and South Dakota ($302,200).

Old story

California’s comfort with variable financing is nothing new.

Between 2019 and 2024, California’s adjustable loan usage averaged 21% a year, also tops in the nation. That was followed by Wyoming and Delaware at 18%, New York and Connecticut at 17% and Massachusetts at 16%.

Louisiana had the lowest average use at 4%, followed by South Dakota at 6%, and Georgia, Oregon, Nebraska, and North Dakota at 7%.

So last year’s adjustable loan usage was a sharp increase over the 2019-24 norms in the Golden State.

The 10-percentage-point share growth in California and Delaware topped the nation. Then came Washington state and Hawaii, up 9 points,Massachusetts, up 8 points, and New Jersey, up 7 points.

Conversely, North Dakota was flat, Mississippi and Louisiana were up only a percentage point, and Nebraska, Illinois, and Missouri rose just 2.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com