Earlier this month, the California Public Utilities Commission issued a proposed decision on California Water Service’s 2024 General Rate Case, outlining rate increases in 2026, 2027, and 2028, updated cost-recovery mechanisms, and a new sales reconciliation framework for its largest subsidiary.

This proposed decision would give California Water Service Group clearer multi-year visibility on regulated revenues and more tools to recover fixed costs regardless of water demand volatility.

We’ll now examine how the proposed multi-year rate increases and cost-recovery mechanisms could reshape California Water Service Group’s investment narrative.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

To own California Water Service Group, you need to be comfortable with a regulated utility that relies on predictable rate cases to fund heavy infrastructure and water quality investment. The CPUC’s proposed decision materially reduces near term regulatory uncertainty by setting out specific rate hikes and revenue mechanisms, though the final vote and potential changes still represent the most important short term catalyst and a remaining regulatory risk for the business.

Among recent announcements, the CPUC’s proposed decision on the 2024 General Rate Case stands out because it directly addresses earlier concerns about delays and uncertainty in California rate relief. By outlining multi year rate increases and reaffirming revenue adjustment and cost balancing tools, it speaks to the same issues that have been central to investors’ expectations around Cal Water’s ability to recover rising PFAS and infrastructure costs through regulated returns.

But investors should also be aware that the same regulatory framework reducing revenue uncertainty could still limit how quickly Cal Water recovers rising treatment and capital costs if…

Read the full narrative on California Water Service Group (it’s free!)

California Water Service Group’s narrative projects $1.1 billion revenue and $187.9 million earnings by 2028. This requires 3.9% yearly revenue growth and an earnings increase of about $52.1 million from $135.8 million today.

Uncover how California Water Service Group’s forecasts yield a $52.00 fair value, a 18% upside to its current price.

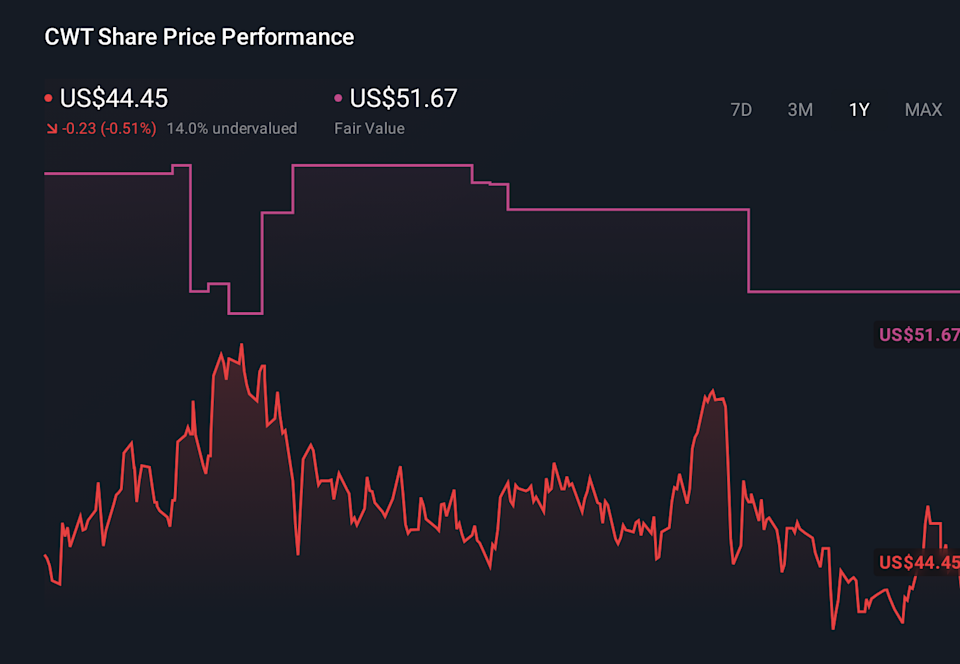

CWT 1-Year Stock Price Chart

CWT 1-Year Stock Price Chart

Four members of the Simply Wall St Community value California Water Service Group between US$40.05 and US$60.39 per share, showing a wide spread of expectations. When you compare that with the proposed multi year rate plan in California, it underlines how differently people weigh regulatory clarity against ongoing cost pressures and why it can be useful to review several viewpoints before forming your own view.

Explore 4 other fair value estimates on California Water Service Group – why the stock might be worth 9% less than the current price!

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include CWT.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com