Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

American Airlines Group (NasdaqGS:AAL) is facing higher operational risk as jet fuel prices rise in connection with ongoing conflicts in the Middle East.

The company is more exposed to fuel cost swings because it does not hedge jet fuel and carries a large debt load.

At the same time, American Airlines has resumed flights to Venezuela and committed around $1b to expand its facilities at Miami International Airport.

Shares of American Airlines Group trade at $11.79, with the stock showing a 15.4% decline over the past week and a 23.8% decline year to date. Over longer periods the stock has also recorded declines, including 11.0% over 1 year, 25.8% over 3 years, and 46.8% over 5 years. Given this backdrop, the new fuel cost pressure and capital spending decisions are likely to be closely watched by investors in NasdaqGS:AAL.

For investors, the mix of higher fuel exposure, resumed Venezuela service, and a $1b Miami expansion raises questions about future cash flows and financial resilience. Upcoming quarters may show how management balances cost pressure with growth projects, and whether the current share price adequately reflects those risks and opportunities.

Stay updated on the most important news stories for American Airlines Group by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on American Airlines Group.

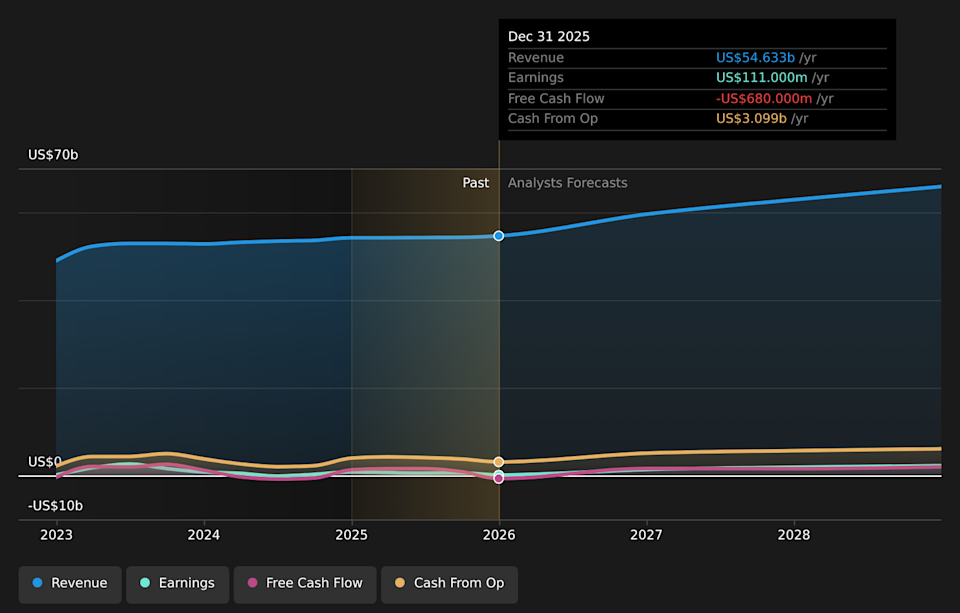

NasdaqGS:AAL Earnings & Revenue Growth as at Mar 2026

NasdaqGS:AAL Earnings & Revenue Growth as at Mar 2026

The latest fuel shock puts American Airlines’ business model under pressure at a sensitive time. Unlike some peers such as Delta Air Lines and United Airlines, American does not hedge jet fuel, so sharp moves in oil prices tend to flow more directly into operating costs. With already tight margins, rising fuel and disruption from Middle East airspace closures can squeeze cash generation just as the company commits to capital-intensive projects like the US$1b Miami International Airport expansion and new routes into Venezuela.

The Miami expansion and resumption of Venezuela flights align with the narrative’s focus on strengthening US Latin America connectivity and premium route networks, which could support revenue growth over time.

Higher fuel costs, a large debt load and interest coverage concerns directly challenge the earlier narrative that highlighted improving margins and better financial flexibility as key supports for long-term earnings.

The recent shelf registration for common shares and debt securities adds a funding angle that is not fully reflected in the narrative, raising questions about how future capital raising could interact with leverage and shareholder dilution.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for American Airlines Group to help decide what it’s worth to you.

⚠️ Interest payments are not well covered by earnings, which can make higher fuel costs and any demand softness more difficult to absorb.

⚠️ Negative shareholders’ equity and a history of thin margins mean balance sheet risk is elevated if conditions stay challenging or if additional capital is raised on less favorable terms.

🎁 Earnings are forecast to grow 32.7% per year, which, if achieved, could give the company more room to handle shocks such as fuel spikes and operational disruptions.

🎁 The shares are trading at 70.9% below one estimate of fair value, which some investors may see as compensation for taking on the higher risk profile highlighted by recent analyst commentary.

From here, keep an eye on how American updates its fuel cost assumptions, capacity plans and cash flow outlook at upcoming events such as the J.P. Morgan Industrials Conference. Any detail on timing and funding for the Miami project, plus initial performance of restored Venezuela routes, will help you judge whether growth projects are strengthening or stretching the business. It is also worth tracking sector-wide moves from carriers such as Delta and United, since changes in domestic capacity or pricing could influence how effectively American can pass through higher costs. Finally, monitor any use of the new shelf registration, as decisions around new equity or debt issuance will feed directly into the risk and reward trade off for shareholders.

To ensure you’re always in the loop on how the latest news impacts the investment narrative for American Airlines Group, head to the community page for American Airlines Group to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AAL.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com