by Mark McDermott

Local Realtors did not enter 2026 with outsized expectations.

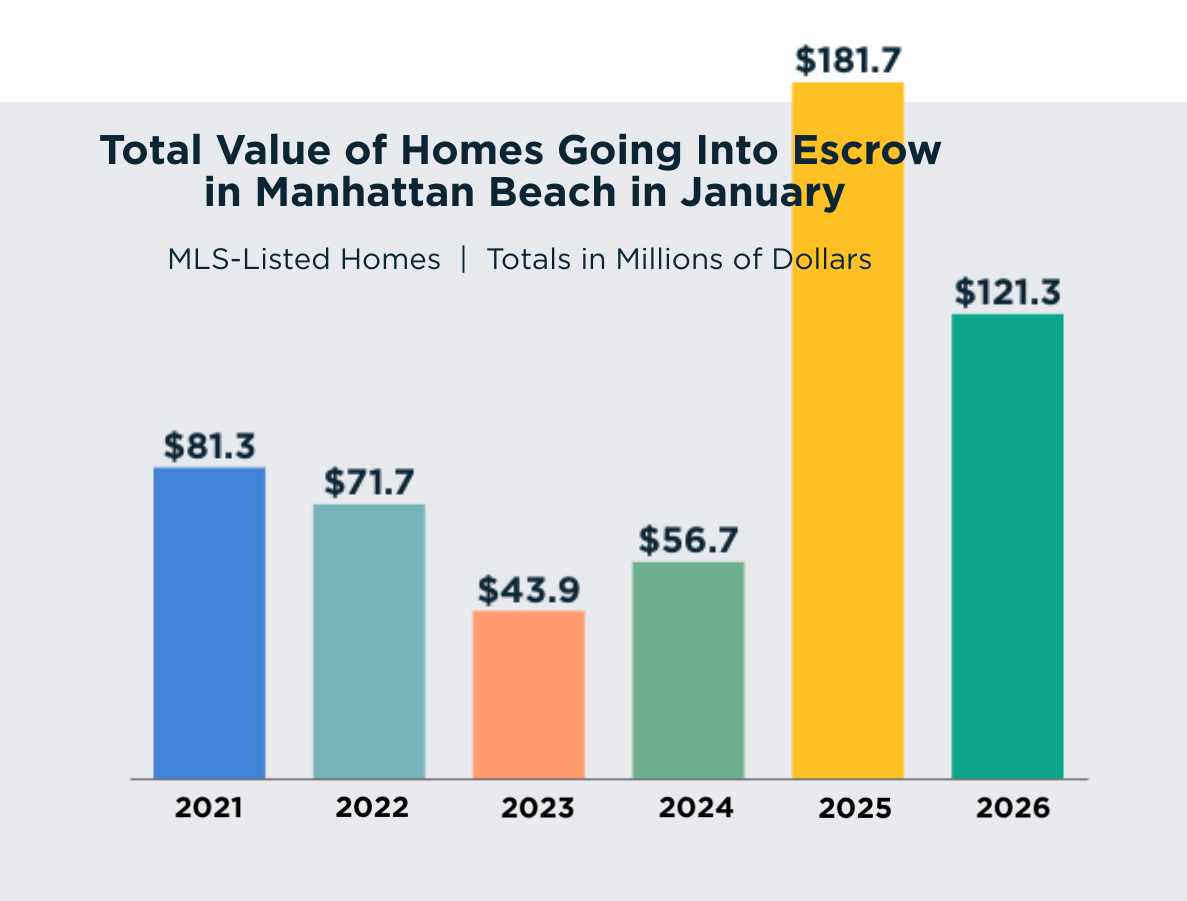

Last January was very different. A stagnant real estate market had been steadily picking up pace over the latter half of 2024, and most local real estate professionals were bullish about 2025. Then the Palisades fires happened, and the Manhattan Beach market caught fire, with a record $181.7 million in homes going into escrow in January alone — beating the old record by a cool $100 million.

Most observers thought the rest of the year would follow the trend, if not reaching quite so spectacular highs, at least achieving a full rebound from the previous sluggishness. And then…a whole lot of nothing happened. By year’s end, Manhattan Beach had logged just 325 sales — barely 21 more than 2024’s depressed total of 304, and not even matching 2009’s “Great Recession” volume. Each quarter after that record Q1 saw fewer sales than the one before it — a pattern that, as broker Dave Fratello of the Edge Real Estate Agency noted, “simply never happens” in real estate.

And so the New Year was not a time of great hope. Then January happened.

It didn’t quite reach the heights of last January, which were driven by emergency buyers, but registered the second biggest total value in sales at $121 million. Nearly everyone’s expectations were boggled.

“At the start of this year, I expected a great Super Bowl and a tepid real estate market,” Fratello said. “I had it backwards.”

The January surge featured multiple properties receiving double-digit offers, with one East Manhattan Beach home drawing 18 competing bids. Properties that real estate professionals carefully priced to attract attention were routinely bid up 10 percent or more above asking, a pattern not seen since the fire-driven frenzy of early 2025.

Fratello said these multiple bid properties were indicative of just how unexpected early 2026 surge has been.

“When you’re over 10 [offers], it’s telling you that your price was probably 10% too low, or more,” he said. “Professional realtors do not intentionally underprice by 10%. Because every house could be an auction, but we don’t do that — so it’s telling you that we as a community just did not anticipate the demand that was right there just below the surface.”

Amy Pearce of Vista Sotheby’s International Realty, who represented the 18-offer property at 1728 Oak Street, couldn’t speak to the final offer because the home is still in escrow. But she said the offers far outstripped the original listing price, a four bedroom, 1,996 sq. ft house, which was $2.199 million.

This home on Oak Street in Manhattan Beach garnered 18 offers in January. Photo courtesy Amy Pearce/Sotheby

This home on Oak Street in Manhattan Beach garnered 18 offers in January. Photo courtesy Amy Pearce/Sotheby

“We sent out 10 seller multiple counter offers, eight responded with a best and final, and we are in escrow well over $2.5 million with a backup offer as well,” Pearce said.

The Oak Street home illustrated both the opportunity and challenge facing Manhattan Beach buyers. Though somewhat dated and in need of updates, prospective buyers told Pearce they were “just fine living in it the way it is, and then giving it the glow up later on.”

“I think people are willing to put the work in to get into the market,” Pearce said. “They’re not afraid of a fixer-upper.”

Topsy turvy

To understand January 2026’s surprise, it helps to revisit the strange trajectory of 2025. It was a year that defied every prediction.

The year began with extraordinary optimism. Market momentum had been building through late 2024, and real estate professionals sensed the long stagnation was finally breaking. Then the January 7 Palisades fires accelerated everything into overdrive.

“This market was already heating up substantially in summer and fall of 2024, particularly at the high end,” Fratello said. “Anything that was happening that was busy, or prices going up in early 2025 was, in many ways, a continuation of trends we already had.”

“To me, the most significant positive change in the market was in the way both buyers and sellers re-entered the market — it felt like a normal year,” he said. “We just really hadn’t really seen sellers by choice for two and a half years. Like 90% of the homes that were on the market for two and a half years, somebody died or got divorced or got a job transfer, and that was the reason behind the sale. And it was like daybreak last year. People were saying, ‘Hey, I’ve waited long enough. I’ve always been wanting to make this move, out of state to be with family, or cash out and move to the desert’ or who knows what — the many different reasons why people might sell their home. They were deciding that it was time to sell and that the market looked fine for them.”

The fire added rocket fuel. That record $181.7 million January was more than double the $81.3 million COVID boom year of 2021 and represented only the first January ever to exceed $100 million in new escrows.

By April, however, something shifted. “By mid-March to mid-April, someone had hit the brakes,” Fratello said. Each subsequent quarter saw fewer sales than the one before, creating that unprecedented upside-down pattern.

The second half of 2025 turned particularly sluggish. Properties that had sold in days during the January frenzy sat for months by fall. The Manhattan Beach rental market — typically predictable at $8,000 to $15,000 per month, with a median rent of $9,500 —”almost collapsed” in terms of demand, according to Fratello, with some homes renting for less than previous tenants had paid.

“There’s something weird going on out there,” Fratello said at the time, speculating about broader economic uncertainty.

Jerry Carew, broker and owner of Three Leaf Realty in Manhattan Beach, attributes the 2025 pattern to basic supply and demand dynamics amplified by the fires.

“You had this big demand that just shot prices way up because of crazy demand, and then there’s the inevitable come down from the high,” Carew said. “A lot of people took advantage of the demand that was created by the Palisades fire. The supply has been low for years, so it’s our new norm. We had an unusual demand, and then the demand went away, so it softened up.”

Despite the year’s ups and downs, Manhattan Beach finished 2025 with a median home price of $3.325 million — up 9.9 percent from 2024 and setting a new record. The previous high of $3.137 million was set in 2022.

This home on Agnes Street, a 3,505-square-foot, six-bedroom, seven-bath home made from salvaged brick walls and reclaimed wood, sold for $6.25 million last year. Photo courtesy the Edge Real Estate Agency

This home on Agnes Street, a 3,505-square-foot, six-bedroom, seven-bath home made from salvaged brick walls and reclaimed wood, sold for $6.25 million last year. Photo courtesy the Edge Real Estate Agency

The Palisades fade

One major question heading into 2026 was whether fire-displaced buyers would continue impacting the market. The answer appears to be no — at least not in the dramatic way seen in early 2025, nor in the expectations that it would permanently change the local market.

School enrollment data tells part of the story. According to Manhattan Beach Unified School District figures, emergency transfers from fire-affected families peaked at 231 students last year. By this school year, according to MBUSD data first reported by the MB News, that number had dropped to 76 — a decline of 67 percent.

Mira Costa High School, which enrolled 120 displaced students in the initial surge, now has 43. Manhattan Beach’s five elementary schools combined host just 28 transfer students, with another 5 at the middle school.

“Each family’s journey after the fires has been deeply personal, and we respect the decisions they made for their children,” Tina Shivpuri, current president of the MBUSD school board, told MB News.

At the real estate level, Palisades buyers appear to have largely moved on from the Manhattan Beach market.

Carew concurred. “It seems like it was about a nine-month run and then it was over,” he said. “There’s probably some, especially in the Sand Section, maybe just the higher end, but the impact was severe and swift and less and less impact. I would say not a whole lot at this point.”

Pearce thinks the impact will be ongoing, if less dramatic than early last year. She believes some families affected not just by the Palisades fire but the other fires from last January are finally able to pull the trigger on purchasing new homes.

“I have a couple of Palisades buyers that are looking, but as I think back to all of these offers, they weren’t [Palisades buyers],” Pearce said of her 18-offer property. “There were like three people from Culver City who were looking, maybe one from Santa Monica, someone from the valley, which was random. But there weren’t any Palisades buyers, actually.”

The initial wave, last January, tended to be what one realtor at the time called “the big whales,” those with the resources to pay cash. But for most other potential buyers, it took time for insurance to cover their losses before entering the market, and for the possibility of rebuilding to perhaps fade. Some families who lost their homes to the fires and initially leased locally are now making permanent moves.

“One client made a comment to me that they’re the first of their friend group that lost their homes that have actually bought something,” Pearce said of a recent Malibu fire victim who purchased in Hermosa Beach. “So I think we have yet to see the impact of those people starting to make decisions. They’ve had the time to look around and figure out where they want to be.”

“If they’re not heading back up towards the Palisades or not rebuilding, then they’ve figured out where they want to be,” she said. “They’ve had the time, and now, it’s go time.”

After the surge

It’s fairly clear, at any rate, that Palisades families didn’t fundamentally drive the January surge. Who or what did? The answer remains somewhat mysterious, even to veteran professionals. Several factors may have converged. One is simple pent-up demand.

“Buyers did seem to retreat a bit in the later part of 2025, and those with needs and plans may now just be deciding it’s time to come back,” Fratello said.

Mortgage rates dropped in late September and early October to around 6.3 percent, but more importantly, buyers seem to have accepted that rates in the sixes are “the new normal.”

“I think it’s between just low inventory, rates getting better, and people just getting used to the rates,” Pearce said. “This is where we are. It’s not going to get any better, so if we want to get in, we need to get in. People are just ready.”

Or maybe, Fratello said, only half-joking, it was just a matter of what a little bit of sunshine could do.

“Don’t rule out good weather,” he said. “We had plenty of rain leading into the New Year and in the first couple days of January, but the clear, warm and beautiful days ever since have paired nicely with visiting open houses. Perhaps it’s that kind of elevated mood one might need to jump into multiple offers. You need a big down payment and a bunch of Vitamin D to compete.”

Unlike many off-season listings that hit the market due to distress sales, January 2026 featured “some really, really nice places,” according to Fratello. “That’s why they’re all getting bid up and absorbed so quickly.”

Inventory increased slightly to 42 active listings from December’s 33, providing “just enough” new listings to hold buyers’ interest without flooding the market and creating what Fratello calls “mass waiting” — where buyers sense an advantage developing as more and more sellers bring out homes at the same time.

Carew noted that Manhattan Beach buyers typically come from north of the South Bay. “When you say, where are most of the buyers coming from? They’re coming from the Culver City, Palms area…They’re just coming from north of here, they’re moving south,” he said.

The fundamental constraint on Manhattan Beach’s market remains inventory — or rather, the lack of it.

Sales as measured by number of homes sold have remained well below normal levels for several years, a phenomenon Fratello attributes to “golden handcuffs” — homeowners with 2 to 3 percent mortgage rates who are reluctant to sell and take on today’s 6 percent rates.

“We still have a shortage of willing sellers,” Fratello said.

Inventory numbers support this theory. By way of example, 2024, with 304 sales, was the lowest sales volume since 1995, according to Fratello’s MB Confidential website’s data. Despite its fast start, 2025 saw only 325 sales. Typically, about 400 homes sell each year. The highest year on record was the 518 homes sold in 2021.

Carew said that those golden handcuffs won’t last forever.

“The further we get away from the 2 percent rates, the less people will have them, and the more people will want to move,” Carew said. “But for a couple of years, people had just refinanced for 2 or 3 percent, so there’s no way they’re going anywhere. As time goes on, it’ll have less of an impact, so it’s a slow increase back to what we would call normal inventory.”

This is not specific to Manhattan Beach. Carew’s data shows the Beach Cities are still off approximately 35 percent in transactions compared to 2018-2019 levels.

“We’re still off quite a bit,” he said.

The combination of limited inventory and strong demand continues pushing prices higher, creating an affordability crisis even by Manhattan Beach standards.

“Everything under $4 million has been bid up,” Fratello said. “It’s scary in many ways. This is obviously a luxury market anyway, so affordability — traditional calculations of affordability — don’t really apply here. But still, you’d like to think that somebody could get into a nice house for under $3 million, and it’s just getting really hard.”

According to data from Haynes, Manhattan Beach’s median home price of $3.325 million requires a minimum annual household income of approximately $802,350 to qualify for a mortgage with 20 percent down, assuming a 6.9 percent interest rate.

By comparison, the California median home price of $905,680 requires an annual income of at least $232,400.

Manhattan Beach is increasingly becoming a market dominated by cash buyers and the ultra-wealthy. In the second quarter of 2025, 44.6 percent of Manhattan Beach transactions were all-cash purchases, according to Haynes’ analysis — far above regional norms.

Real estate professionals have varying outlooks for 2026, shaped by last year’s unpredictability.

Pearce is bullish. “I think it’s going to be a really good year,” she said. “There’s a lot of momentum and a lot of people watching. Hopefully, if people are thinking about selling, they’ll want to get on the bandwagon and list their house if they have an alternative, because we need to shake loose some inventory.”

Carew is more cautious, hoping for what he calls “a vanilla year.”

“Some ways I’m hoping for a vanilla year so that we can predict it,” Carew said. “When you can predict the market, it’s kind of nice. You know what’s coming. Everything seems to be very unpredictable around the globe at the moment, so it’d be nice if at least real estate was predictable.”

He projects an average year at best unless something dramatic changes, such as interest rates dropping to 4.5 percent.

“If it stays around six, give or take, I think we’ll just have an average year, nothing special,” Carew said.

Fratello, chastened by the unruliness of 2025 and early 2026, is reluctant to make forecasts.

“If I couldn’t predict what was going to happen in January, how can I predict what’s going to happen the rest of the year?” he said.

What he and everyone else in the local real estate industry can measure is momentum. Carew tracks weekly escrow data across the Beach Cities for his office meetings and has seen consistent improvement since January began.

“It’s gone up every week since January, and we’re in week five or six, and it’s gone up nice and steady,” he said. “The market’s improving. That’s what you would expect, and it’ll peak in May, June.”

Whether that pattern holds — or whether 2026 delivers another surprise — remains to be seen.

“There’s no one thing that broke,” Fratello said, reflecting on January’s unexpected surge. “You could try and say, now that it’s happening, I can taste what’s in the soup. But the truth is, nobody could have foreseen it. There isn’t any one factor.”

Manhattan Beach’s strong performance is leading a broader South Bay recovery, according to Haynes’ year-end analysis.

Redondo Beach saw an 11.7 percent jump in sales volume in 2025, the highest increase in the region, paired with 4.8 percent price growth to a median of $1.59 million. Hermosa Beach’s median rose 6.8 percent to $2.4025 million, though sales dipped 8.3 percent — likely due to tight inventory.

On the Palos Verdes Peninsula, the picture was mixed. Rolling Hills Estates posted 7.9 percent price growth despite an 11.4 percent drop in sales. Rancho Palos Verdes saw modest 0.8 percent appreciation with a 5.6 percent sales increase. Palos Verdes Estates experienced a 7 percent price decline to a $2.5665 million median, though sales rose 6.9 percent.

Rolling Hills, with its extremely low transaction volume, saw the largest price swing — down 28 percent — though sales increased 23.5 percent.

“Despite high mortgage rates and affordability concerns, the market proved resilient,” Haynes wrote. “Buyers were still making moves, and well-located homes continued to command strong prices.”

Carew emphasized Manhattan Beach’s continued dominance in the region.

“Manhattan Beach leads everything. There’s no doubt about it,” he said. “Even when the market crashed back in ’07-’08, it was the last to crash and the first to come back. It will always be the leader of the Beach Cities. It’s a destination. I don’t see that changing anytime soon. I am just happy to be living here, and to have a business here.”

It’s also continuing to be a destination for high profile buyers. Last year, Laker Luka Donicic bought a $25 million Sand Section home (one formerly owned by tennis star Maria Sharapova), while actor Vince Vaughn, a longtime East Manhattan Beach resident, bought a Strand home for $16.75 million (which, curiously, was originally listed at $27 million).

As the spring selling season approaches, one thing seems certain: in Manhattan Beach real estate, the only constant is unpredictability, albeit of an ever-upward sort. ER