Why Moody’s Stock Is Back in Focus

Moody’s (MCO) is under fresh scrutiny after it cut New York City’s credit outlook to negative, and investors reacted to new worries around private credit market stress and broader financial sector stability.

See our latest analysis for Moody’s.

At around US$430.01, Moody’s recent share price return has been mixed, with a 1 day gain of 0.83% but a 7 day share price decline of 8.89% and a year to date share price decline of 13.82%. The 3 year total shareholder return of 49.78% and 5 year total shareholder return of 55.78% point to stronger longer term compounding, suggesting recent credit outlook headlines and private credit worries have cooled momentum rather than erased the longer run story.

If credit market jitters have you looking beyond ratings agencies, this could be a moment to scan 19 top founder-led companies as potential long term compounders outside the usual financial names.

With Moody’s posting annual revenue of US$7.7b and net income of US$2.5b, yet showing a year to date share price decline of 13.82%, you have to ask: is there a mispricing here, or is the market already baking in future growth expectations?

Most Popular Narrative: 22% Undervalued

According to one of the most followed narratives on Moody’s, a fair value of $551.41 sits well above the latest close of $430.01, putting that valuation work firmly back in focus for anyone reassessing the stock after the credit headlines.

📈 Moody’s has established itself as one of the global standards in credit ratings, a status reflected in its wide economic moat and consequently stellar operating margins in the 45 to 50% range. The company consistently generates returns on invested capital roughly 5x its cost of capital, a strong signal of disciplined and effective capital allocation by management.

According to andre_santos, that fair value leans heavily on high margins, robust returns on capital and a cost of capital that stays comfortably below projected profitability. Curious how earnings, revenue and dividends are woven together to support that $551.41 figure without relying on tech style growth assumptions? The full narrative spells out the math, the weight given to each model and how those inputs tie back to Moody’s long run business profile.

Result: Fair Value of $551.41 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, there are still clear pressure points, including questions around AI’s impact on Moody’s Analytics and any long term shift away from US based rating agencies.

Find out about the key risks to this Moody’s narrative.

Another View: Higher Multiple, Higher Expectations

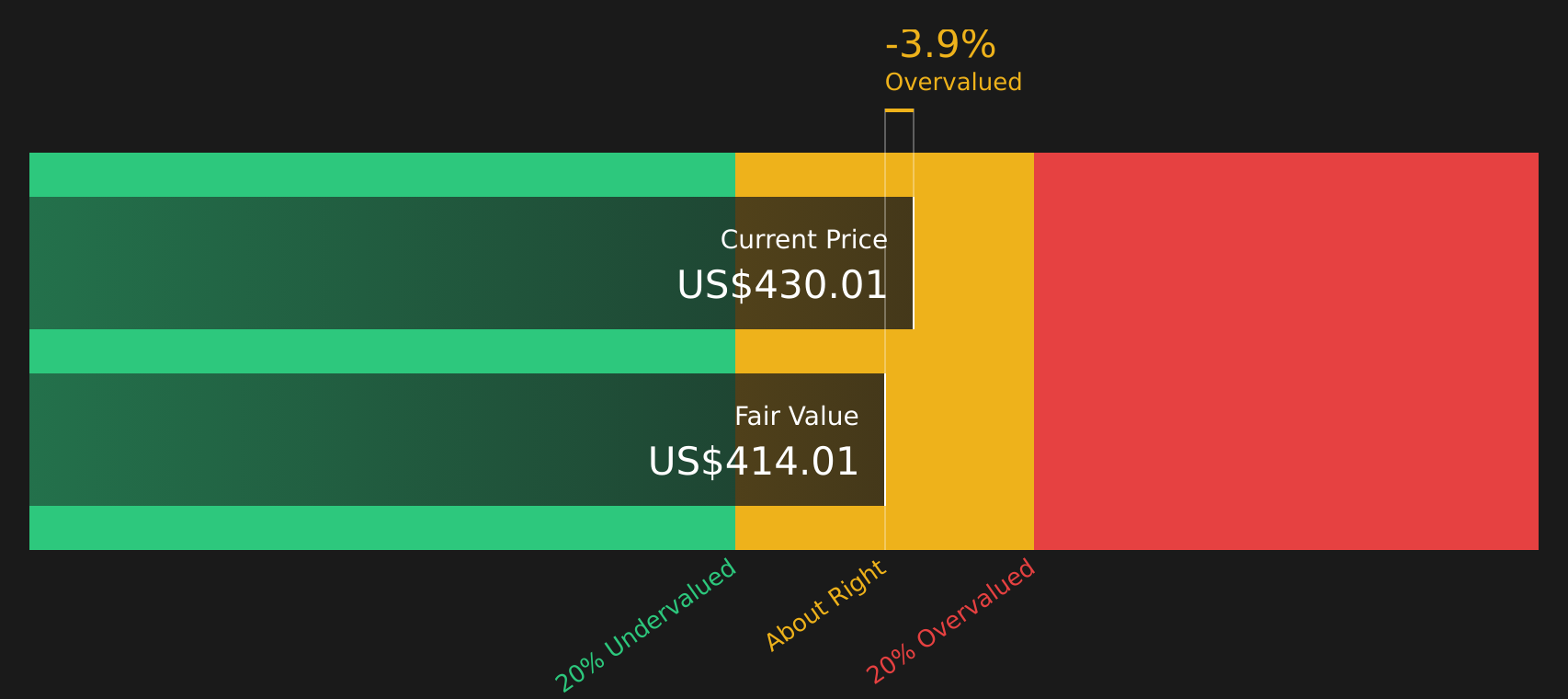

Our DCF model has Moody’s at a fair value of $414.01, slightly below the current $430.01 share price. This points to the stock being overvalued on this measure rather than 22% undervalued. If cash flows do not match the optimism baked into the narrative, where does that leave you?

Look into how the SWS DCF model arrives at its fair value.

MCO Discounted Cash Flow as at Mar 2026Next Steps

MCO Discounted Cash Flow as at Mar 2026Next Steps

With mixed views on value and some clear tension between risks and rewards, now is a good time to look at the numbers yourself and decide where you stand. To weigh both sides in one place, take a close look at the 3 key rewards and 2 important warning signs.

Ready to Hunt for Your Next Idea?

If Moody’s has sharpened your focus, do not stop here. Use this momentum to line up your next moves with a few targeted stock ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com