Time to read [6 minutes]

After 32 years of Manhattan housing market coverage, a new independent quarterly report series launches at HousingNotes.com, adding a dedicated Manhattan townhouse (1–3 family) market analysis alongside long-standing co-op and condo coverage.

Co-ops & condos saw continued momentum in 2025, with the median price up 5.2% to $1.225M, sales up 2.9%, and listing inventory down 16.7%—tightening supply amid the early effects of the Iran War shock in March, which deterred new listings. The luxury segment cooled slightly overall, except for a surge in the $3–$5M range (+76.7% year over year).

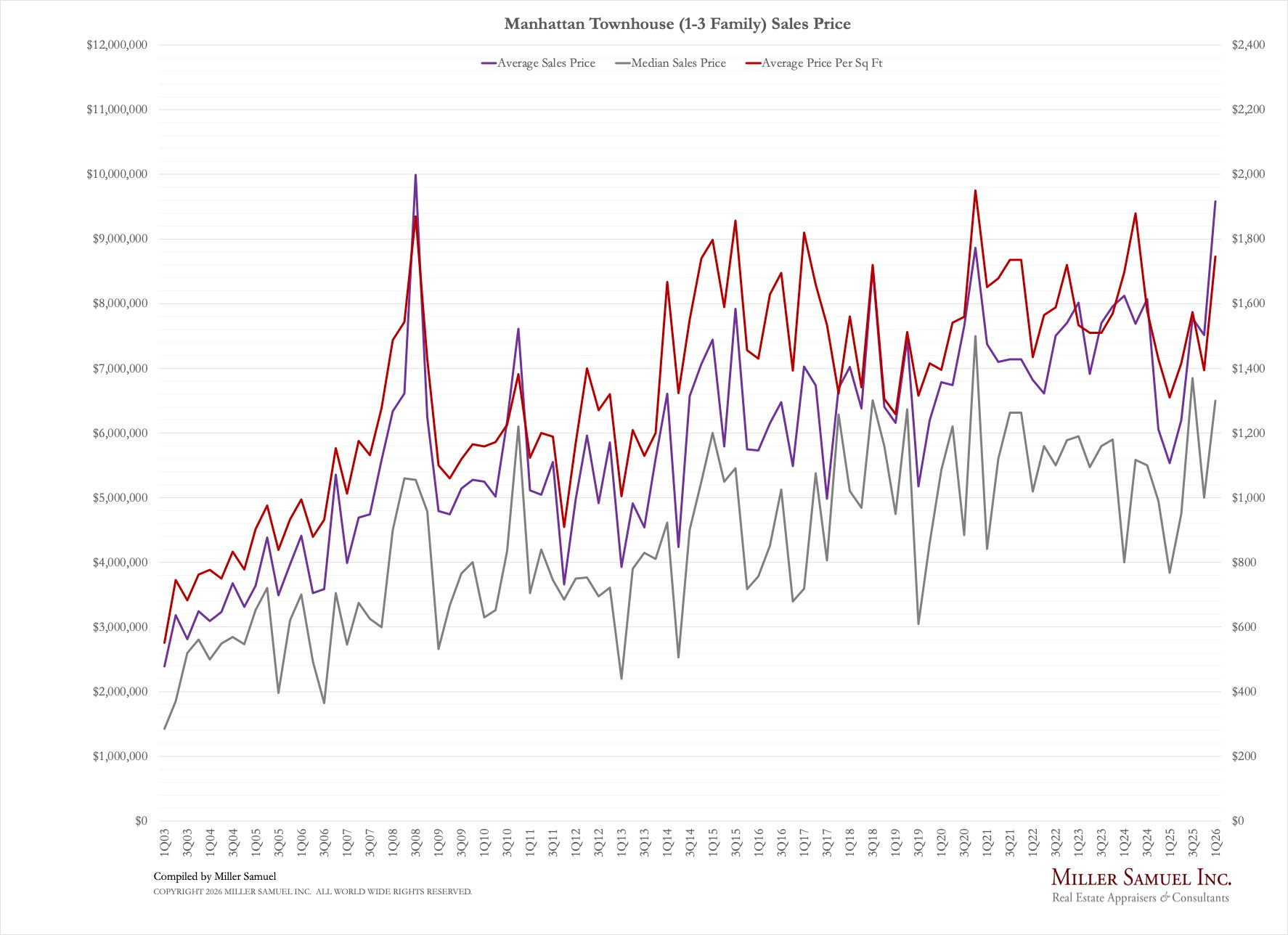

Townhouses rebounded sharply: the median price jumped 69.4% to $6.5M, and the average price rose 73.1% to $9.58M, driven by larger sales and shrinking inventory, with market pace improving to 14.5 months of supply, well above long-term norms.

April 1, 2026: After 32 years of Manhattan housing market coverage, I have struck out with my own report effort and plan to continue the series, with quarterly releases. Initially, the report write-ups with charts will appear at HousingNotes.com. I plan to keep the co-op and condo analysis methodologies consistent, but I am adding the Manhattan townhouse market (1-3 families) as a new, separate addition to this quarterly effort.

It should be noted that this quarter’s sales and price results do not reflect the impact of the Iran War, which began on February 28th, resulting in a spike in mortgage rates and heightened economic uncertainty, due to delays in closed sales. An exception to this impact is listing inventory, which responded quickly as consumers pulled inventory off the market or delayed placing inventory on the market during the month of March.

Here are the hard numbers for the 1Q26 report, followed by the analysis:

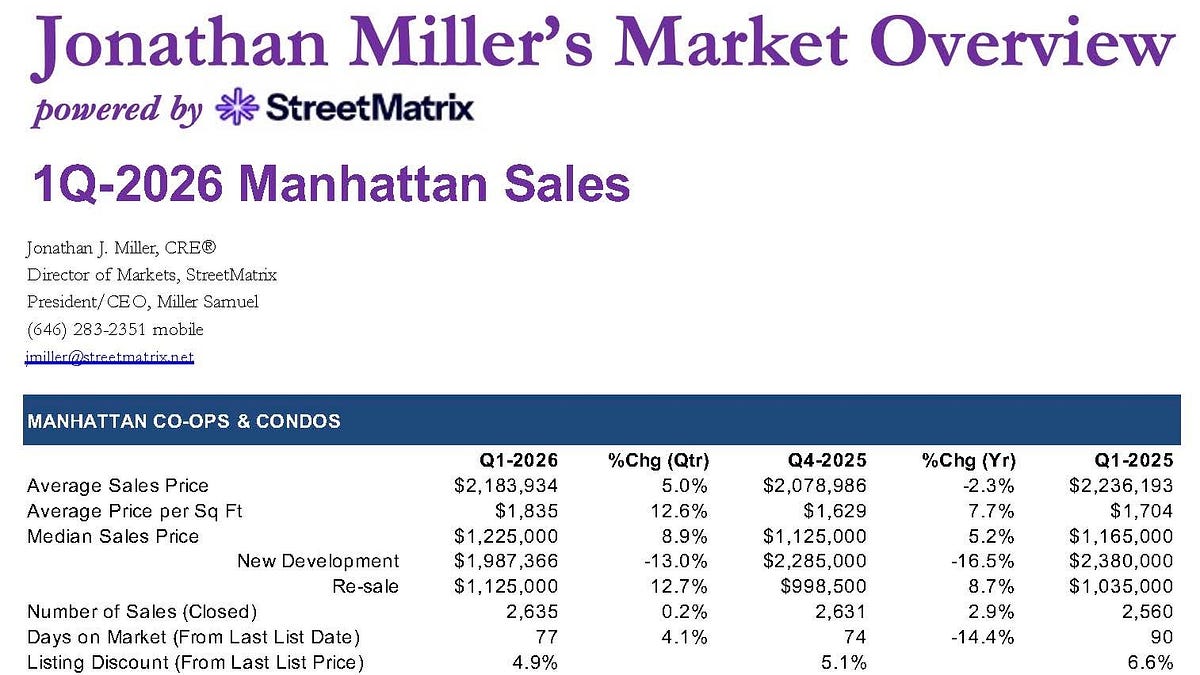

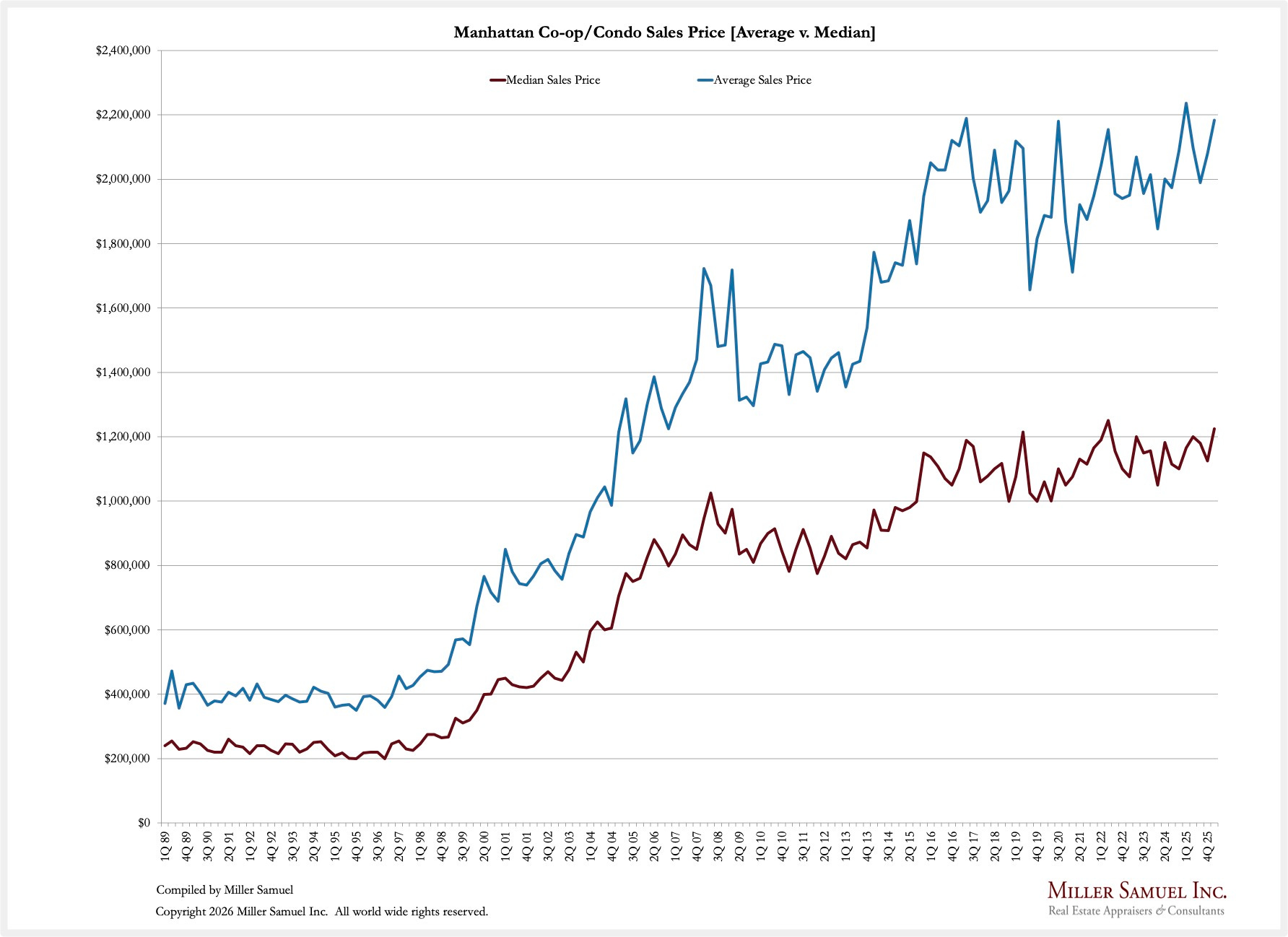

The first-quarter Manhattan market continued its 2025 performance, with rising prices and sales, along with falling listing inventory. The median sales price rose year over year to $1,225,000, up by 5.2% to the second-highest level on record. The average sales price slipped by 2.3% annually to $2,183,934, the third-highest on record. The metric fell from the year-ago quarter record, largely due to a decline in average sales size and a smaller market share for the new development subset.

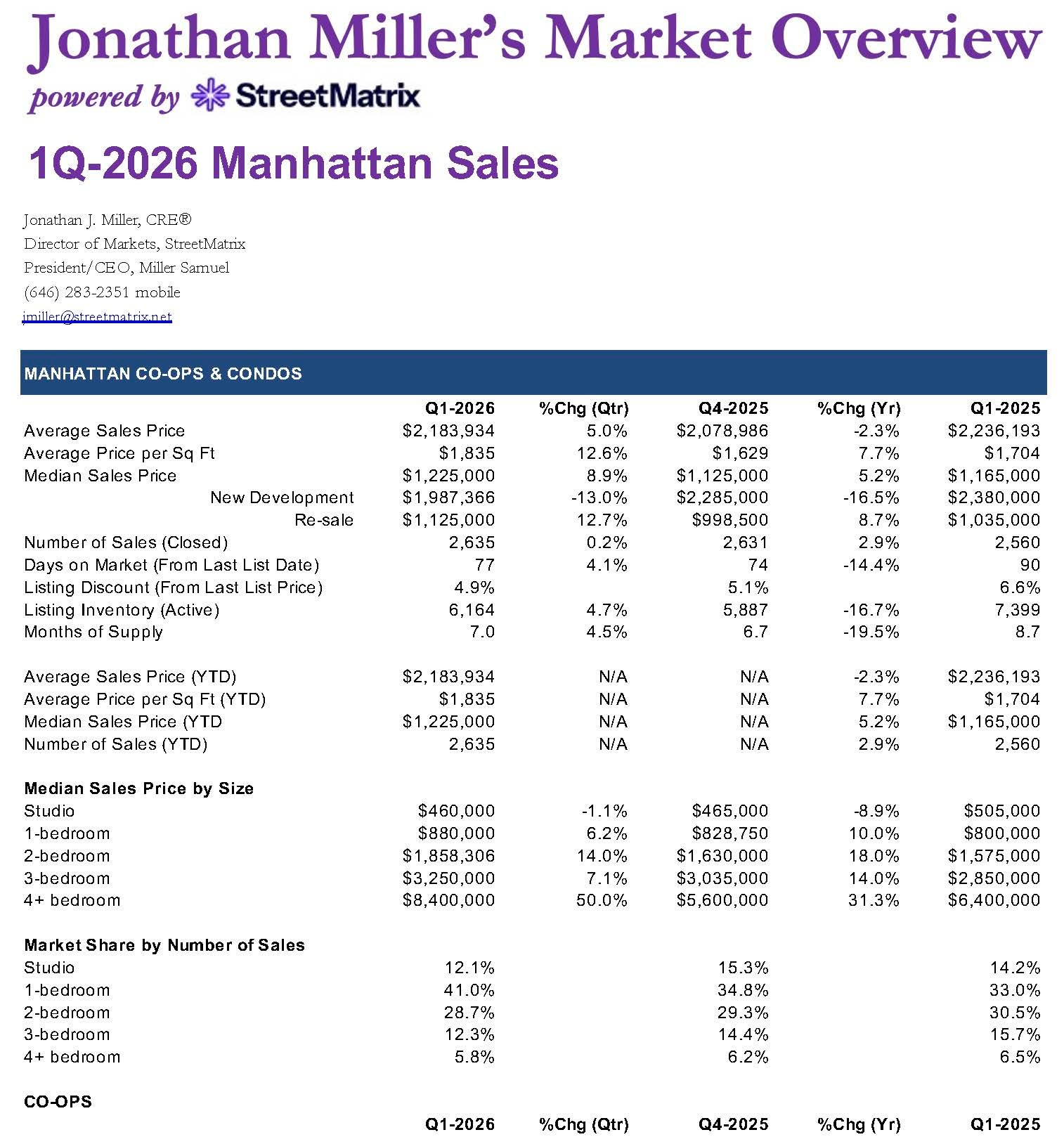

New development accounted for 8.9% of sales, well below the first-quarter market-share average for the decade of 11.7%, while the average sales size was only 1,275 square feet, also down from the first-quarter decade average of 1,526 square feet.

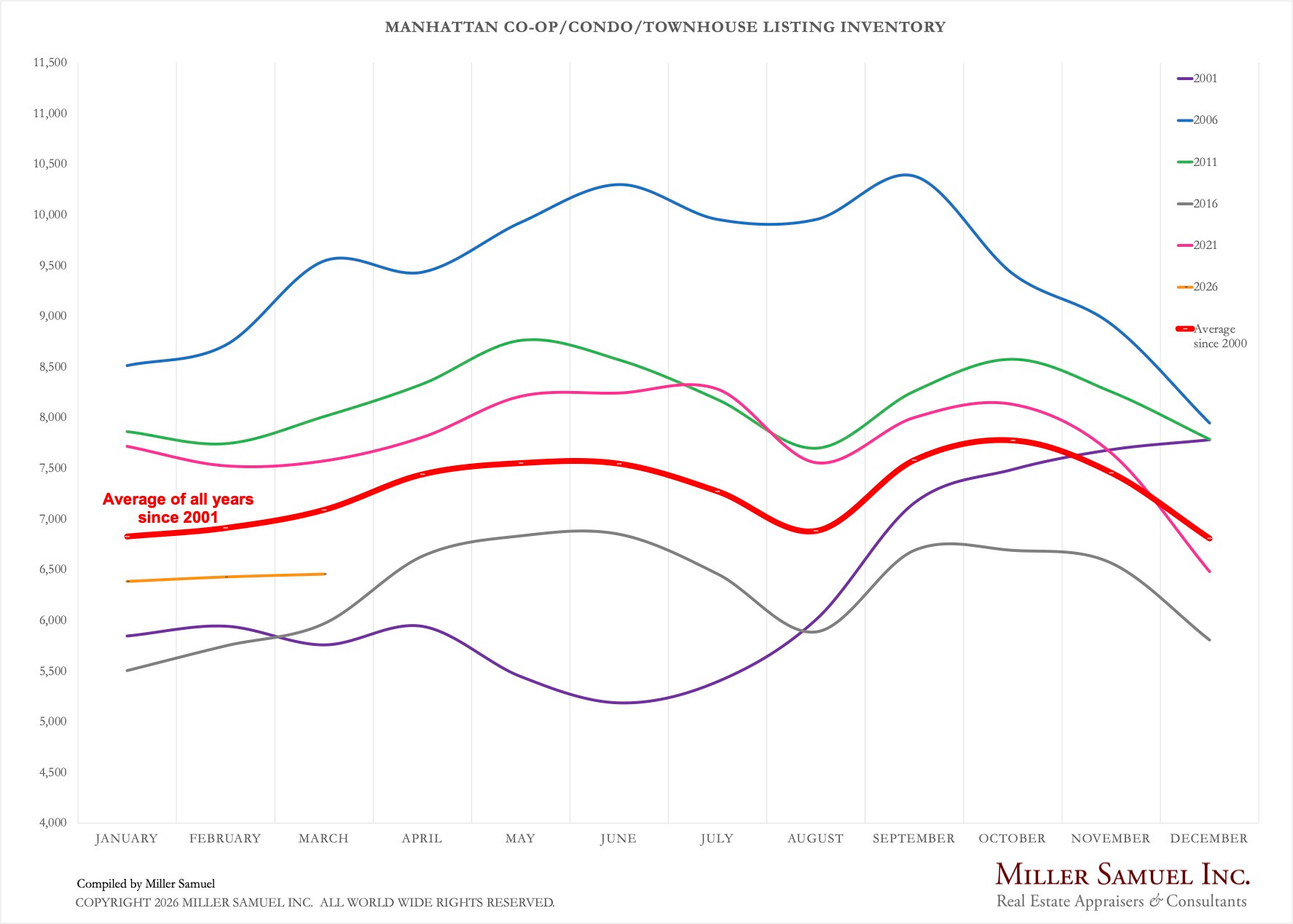

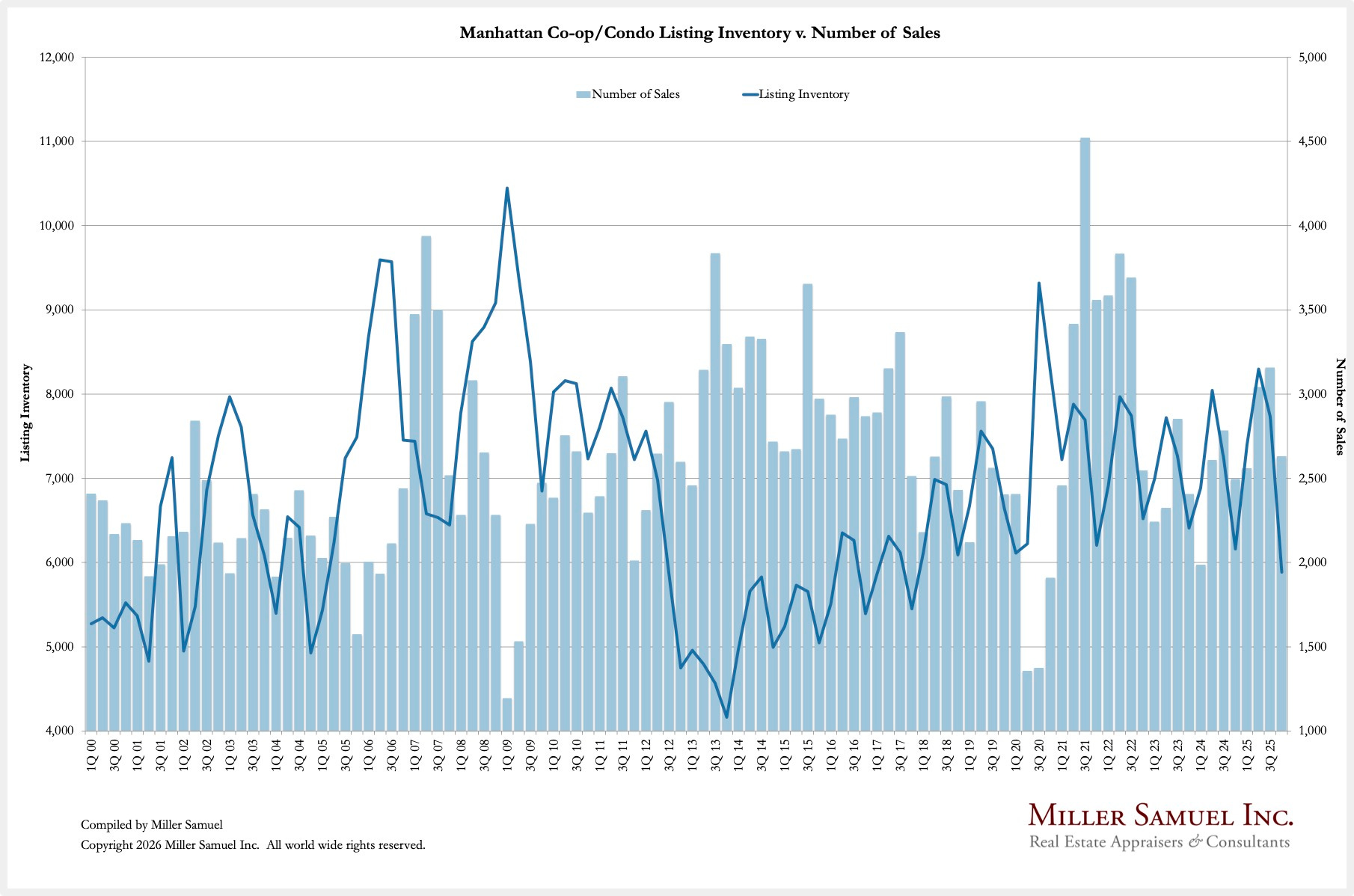

Listing inventory for Manhattan co-ops and condos was 6,164, down 16.7% annually, for the second decline. The drop in supply was consistent among co-ops and condos, with co-ops falling 17.1% annually and condos falling 16.4% year over year. The similar drop was due to the war’s impact, and those declines largely reflected the uncertainty overlay caused by the Iran War in March. There were 2,635 sales during the quarter, 2.9% more than the same period last year, for the fifth consecutive quarter of rising sales. With rising sales and falling listing inventory, the market felt faster on the ground. The months of supply, which illustrates how long it takes to sell all listings at the current sales rate, was 7 months, or 19.5% faster than the same quarter last year and 14.6% quicker than the decade average of 8.2 months. The average months of supply was also 8.2 months, indicating that the current market is running much faster than long-term norms.

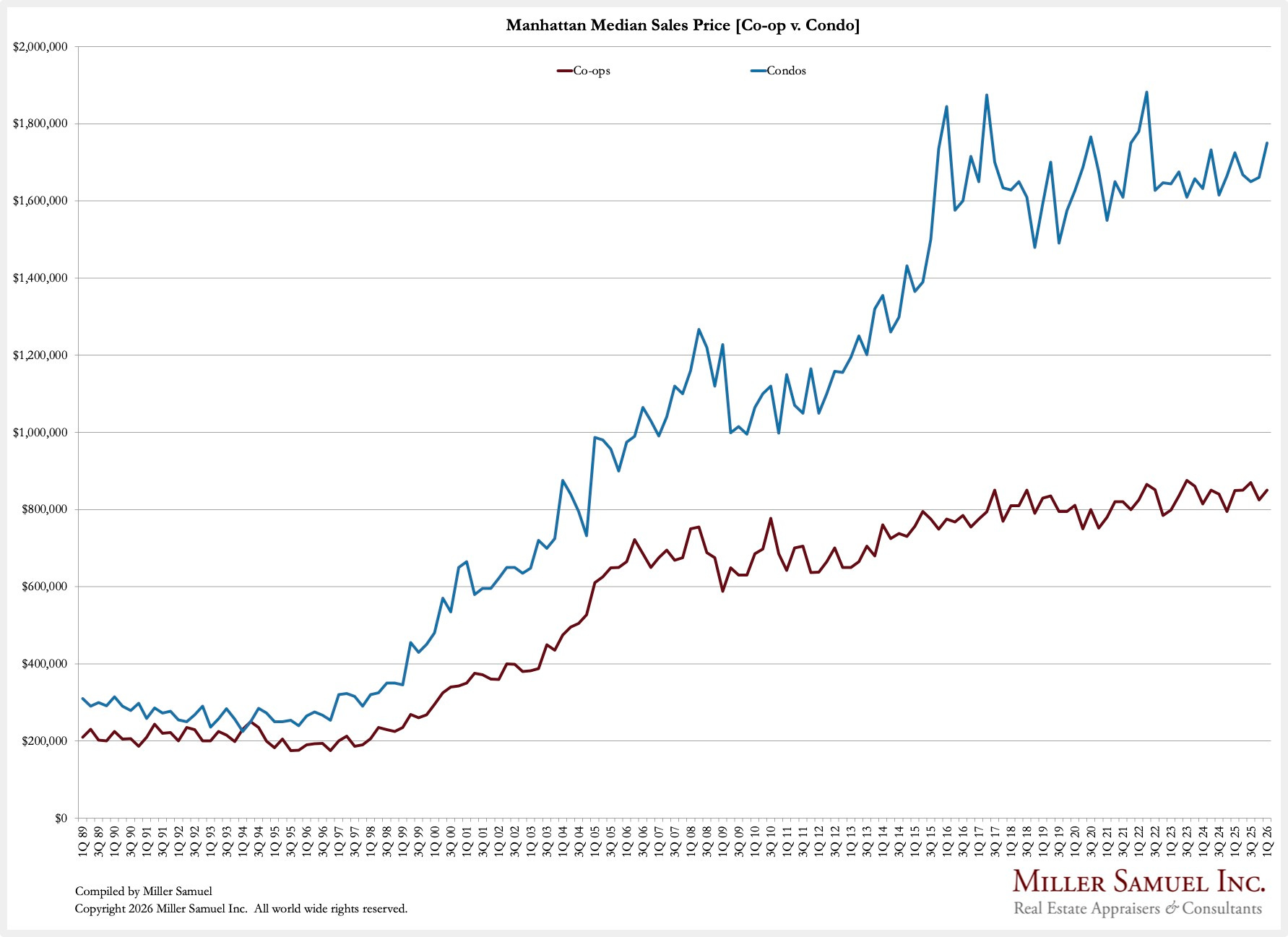

Co-op monthly maintenance averaged $3,007, up 3.5% or $2.76 per square foot per month, while condo common charges plus real estate taxes averaged $4,559, down 5.1% or $3.44 per square foot per month, consistent with their respective differences in median sales prices.

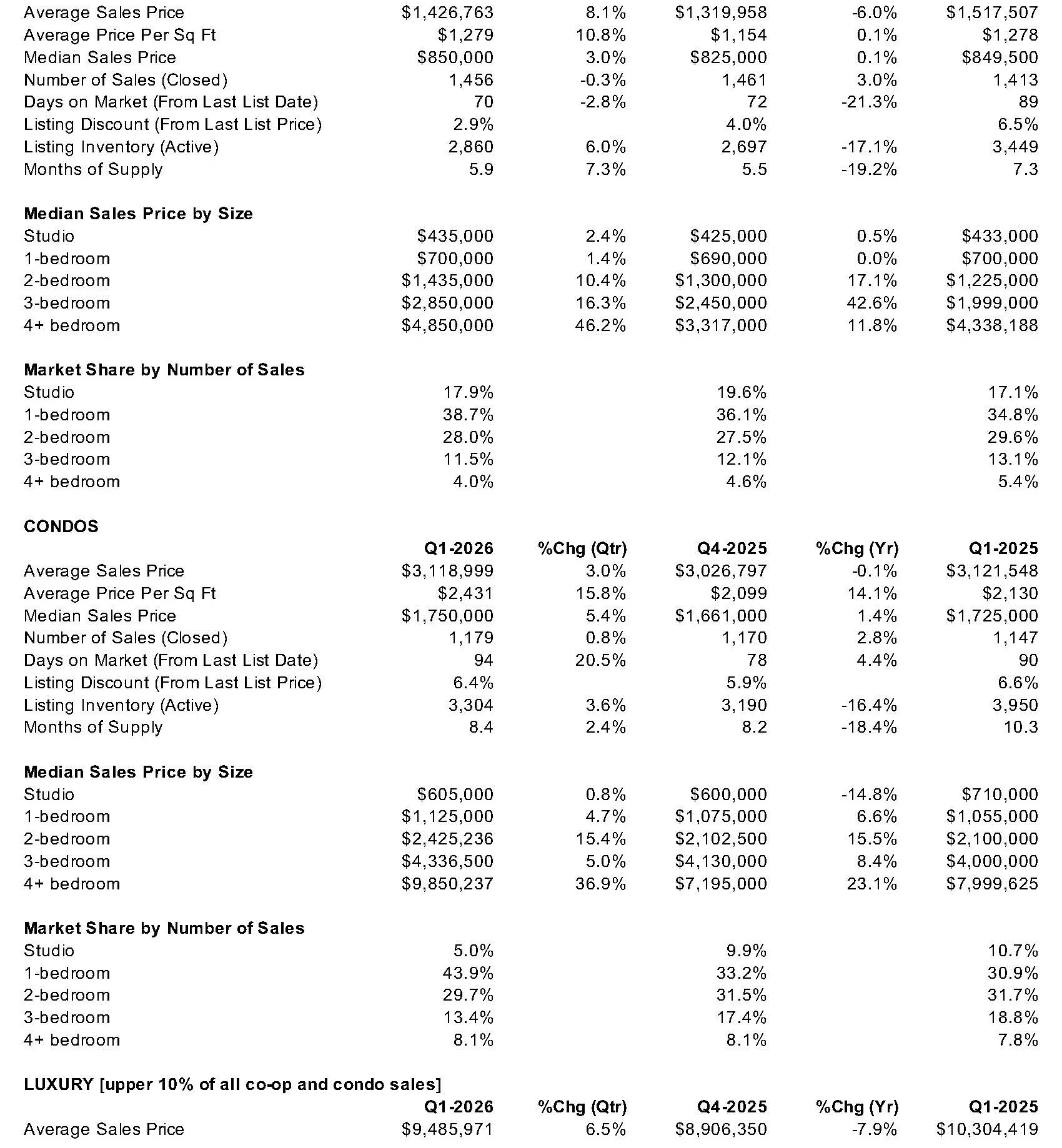

The entry level for the luxury market, based on the top ten percent of all sales, was $4,430,000. The market shift to smaller sales: a 9.2% drop in average sales size to 2,948; the median luxury sales price was $6,850,000, down 0.3% year over year. The hot spot in the luxury market was clearly in the $3 million to $5 million price tranche, with 456 sales, surging by 76.7% year over year, the highest total in a dozen years. Even though a portion of these sales fall outside the luxury minimum threshold, it demonstrates that certain higher-end segments are seeing significant sales activity. Luxury listing inventory dropped by 26.9% to 903, the lowest level since the second quarter of 2008.

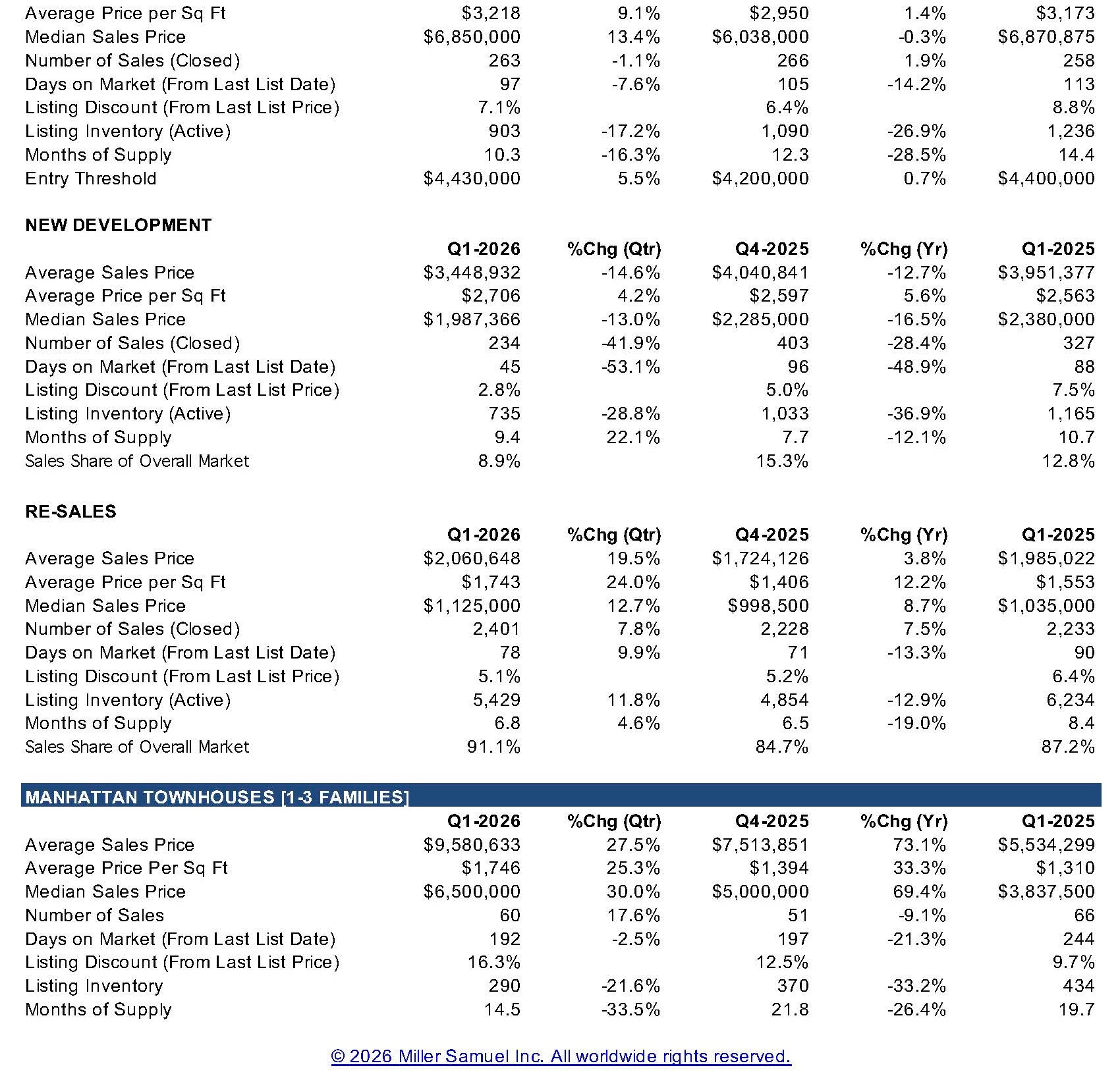

After a year of weak price direction, the last two quarters of Manhattan townhouse sales have seen a year-over-year surge in all price trend indicators. The median sales price surged 69.4% annually to $6,500,000, largely due to a shift toward larger sales. The average sales size of Manhattan townhouses was 5,487 square feet, the second-highest on record and 29.9% larger than the prior-year quarter. As a result of the shift in sales size, the average sales price also surged by 73.1% to $9,580,000, the second-highest on record.

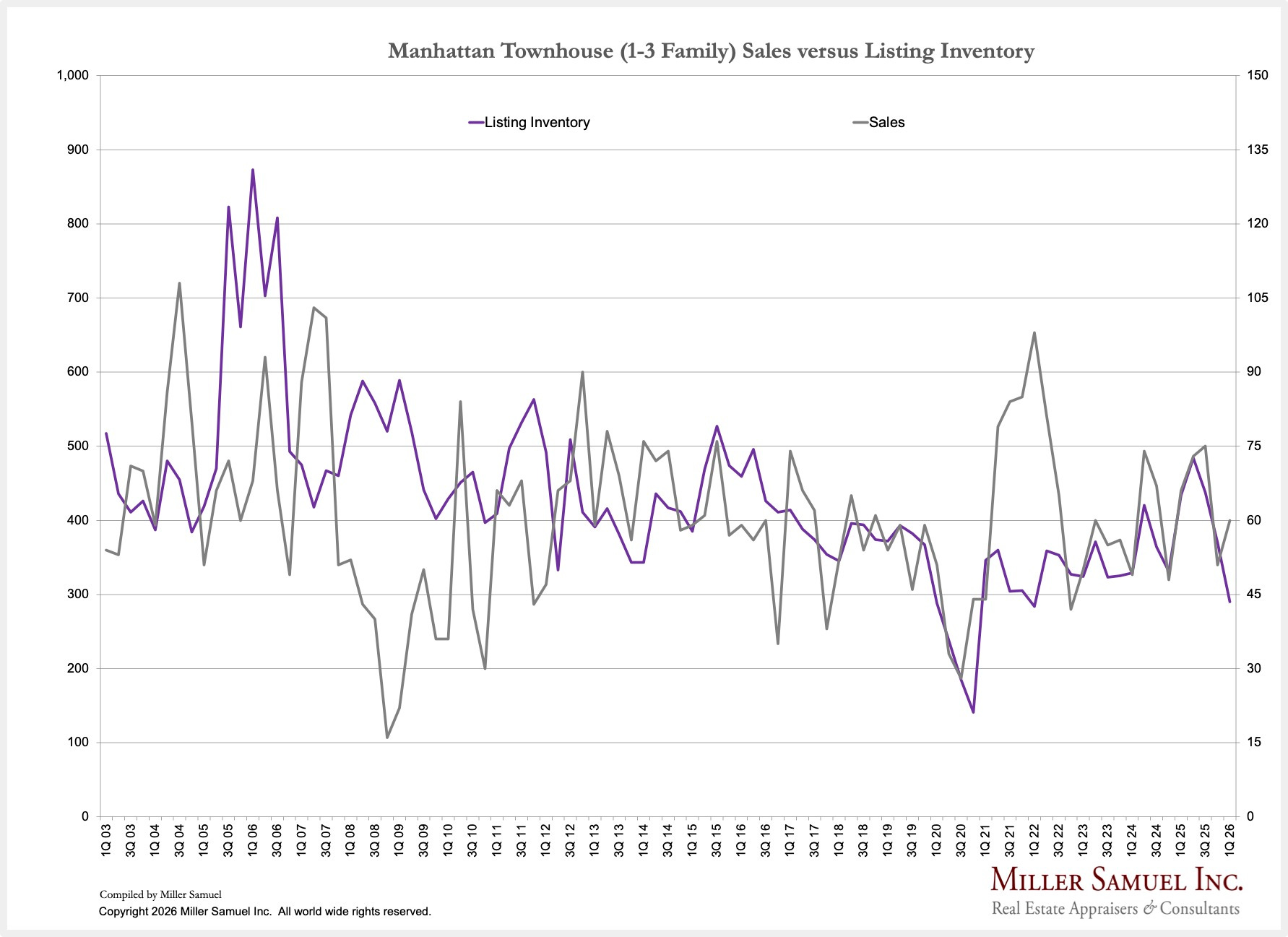

With listing inventory falling faster than sales, the market quickened. The months of supply were 14.5 months, or 26.4% faster than the same quarter last year and 19.6% quicker than the first quarter decade average of 18 months.

The average co-op/condo sale is skewing smaller and less new-development heavy: the average price slipped 2.3% even as the median hit the second-highest on record, because average size fell and new development’s share (8.9%) sat well below its 10-year first-quarter norm (11.7%).

Market velocity meaningfully outperformed history: 7 months of supply is not just 19.5% faster than a year ago, it is also well below the 10-year first-quarter average of 8.2 months, implying a structurally tighter resale environment heading into the Iran War shock.

Cost-of-carry dynamics are diverging: co-op monthly maintenance rose 3.5% to $3,007 (or $2.76 per square foot), while condo common charges plus taxes fell 5.1% to $4,559 (or $3.44 per square foot), subtly narrowing the operating-cost gap between co-ops and condos even as their sale-price hierarchy remains intact.

The Actual Final Thought – Manhattan is showing its groove.

I joined my friends Noah Rosenblatt and John Walkup from Urban Digs to talk about national issues and specifically the Manhattan housing market. It is always fun to talk with them – they care about what happens in the weeds while smartly avoiding my dad jokes.

Urban Digs is an important market intelligence tool for real estate professionals.