Time to read [6 minutes]

Despite fears that higher taxes under NYC’s new mayor would drive out Wall Street tenants, data show no mass relocation, and office demand remains strong, particularly for Class A space, which now dominates leasing activity.

Manhattan’s office market rebounded sharply in 2025, hitting its strongest leasing levels since 2019 and its biggest year‑to‑date demand since 2000, yet the recovery is highly polarized, with newer Class A buildings thriving while older Class B/C office stock struggles.

Major firms like JPMorgan, Apollo, and Elliott Management continue to expand in Manhattan, underscoring that New York remains the financial and cultural hub despite talk of an exodus; the city’s “tax‑the‑rich” push hasn’t meaningfully altered location or migration trends.

As my CT-based grandfather always told me as a teenager growing up in The DMV, “Jonathan, if you’re not in New York, then you’re just camping out.” He may have borrowed that line from former New York governor Thomas E. Dewey, who once said that. But who cares? It was a great quote and stuck with me.

There was a terrific Financial Times piece that came out last Friday: The great Wall Street relocation that never quite happens. The piece talked about how the new NYC Mayor, with his push for higher taxes on the wealthy, was expected to drive out office tenants (especially on Wall Street). And remember, there has been record compensation on Wall Street over the past two years.

Placing the compensation issue aside, a relocation pattern out of New York isn’t showing up in the commercial data, and demand remains strong (perhaps because of the line my grandfather shared with me). I described the exact same phenomenon that drove me crazy with the lead-up to the election and the supposed exodus that never happened last fall: NYC Housing Wealth Exodus Only In Headlines and Hearsay.

From The FT:

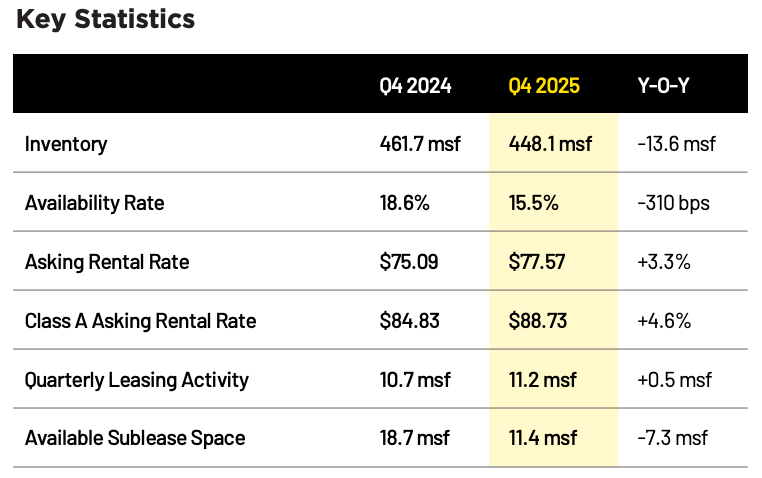

The article referenced a Savills office research piece for 4Q25 with the headline: Manhattan ends strongest leasing year in a decade with a high-performing fourth quarter. Inventory is down, and prices are rising.

Source: Savills

Source: Savills

The top-tier and overall leasing side of the NYC office market has strengthened sharply since 2024 (Class A), but the recovery is highly polarized and still leaves a big overhang of older, Class B & C stock. This is a highly polarized commercial office market with a boom at the top and a long, grinding workout for obsolete assets in the remainder. Media coverage tends to focus on Class A and little else. We see the same parallel in the residential luxury market.

Manhattan office leasing volumes in 2025 hit their highest levels since 2019. By the first three quarters of 2025, roughly 30M sf had been leased in Manhattan, the strongest year‑to‑date demand since 2000. Class A is capturing the bulk of this: about 70% of Q3 2025 volume was Class A, and occupancy in top‑tier buildings has risen for four consecutive fiscal years.

Manhattan Central Business District (CBD) availability is still well above pre‑COVID levels: roughly 18% in mid‑2024, versus 12% pre‑pandemic, despite recent improvement. The comptroller characterizes the picture as a mix of “boom loop” at the high end and structural stress for older assets that will need renovation or conversion.

Many of the firms that have threatened relocation to cheaper office hubs in the south are still growing their NYC presence despite a new headquarters location. Again, per that FT piece:

That may explain why some firms that officially “moved” are still expanding in Manhattan. Elliott Management may be headquartered in Florida, but it continues to grow its New York presence. Apollo may well build a major office in the south. But the centre of gravity of Wall Street remains, stubbornly, where it has been for more than a century.

Source: JPMorganChase

Source: JPMorganChase

JPMorgan has just opened a monster $3 billion, 60‑story global headquarters at 270 Park Avenue, seemingly on stilts, designed for about 10,000 employees. It is impressive – just walking around gives one a clear scale of its immensity. I’ve never experienced that walking around any other office building. I honestly marvel how it won’t tip over. The bank has acquired adjacent properties and built a multi‑block Midtown “JPMorgan neighborhood.” This pattern indicates they have a long-term commitment to remain in Manhattan rather than an exit.

Their CEO has repeatedly said he “wants everyone in the office,” using the new HQ as a recruitment and cultural tool, and has criticized extensive remote work as undermining apprenticeship, culture, and productivity. He describes the building as “commute‑worthy” and future‑proofed, with heavy investment in hospitality, wellness, and technology, which implicitly argues that a high‑end urban office is essential to a leading global bank.

Does it have a rock-climbing wall? Asking for a friend.

Mamdani’s millionaire‑and‑billionaire tax agenda is framed as clawing back a portion of federal giveaways to the top 1% and reversing the narrative that rich donors set the standard for what is “responsible” tax policy. Research cited in the context of Mamdani’s election indicates that when New York previously raised top‑bracket taxes, millionaire migration barely moved, suggesting that social and professional ties may matter more than marginal tax changes. The idea of tech bros leaving California for Florida to avoid taxes is NOT the same concept.

Mamdani’s NYC idea is an annual income/estate‑based “tax the rich” push, while California’s proposal is a one‑time 5% wealth tax on billionaires’ net worth.

My “camping out” quip seems to be the actual driver of Wall Street’s unwavering focus on Manhattan. That’s great news for the housing market in the NYC metro area. JPMorgan’s $3 billion HQ signals that major players still see Manhattan as an important global location, as reflected in the strength of office leasing data. Yet certain media coverage keeps predicting an exodus that never quite shows up in the data, and it’s tiring, no?

The Actual Final Thought – “And you just don’t get it, you keep it copacetic. And you learn to accept it, you know you’re so pathetic.” While this is how I learned what “copacetic” meant (translated: hunky-dory), it is clear that either word can apply to Class A office space despite the negative drumbeat of office market predictions. Admittedly, I still prefer to use “hunky-dory.”