Time to read [6 minutes]

Manhattan townhouses are a tiny slice of the sales market (about 2% of 4Q25 residential closings) and behave as a niche segment rather than a market driver.

In contrast to apartment combinations where larger, contiguous space, up to roughly 6,000–7,000 square feet, can achieve a price-per-foot premium. Side‑by‑side townhouse combinations generally fail to generate that same premium and mainly just satisfy demand for more space.

“Double‑wide” mansionization, concentrated in affluent Manhattan neighborhoods, is shrinking the city’s housing unit count and reflects a widening wealth gap without meaningfully boosting price per square foot beyond condition-driven gains.

I’ll get to the townhouse thing in a sec, but first, take this as a lead-in. To my grad students and regular podcast listeners, you already know I think pie is better than cake and convey this opinion whenever I can. Here is a PowerPoint slide I use every year which likely makes my students wonder about my sanity.

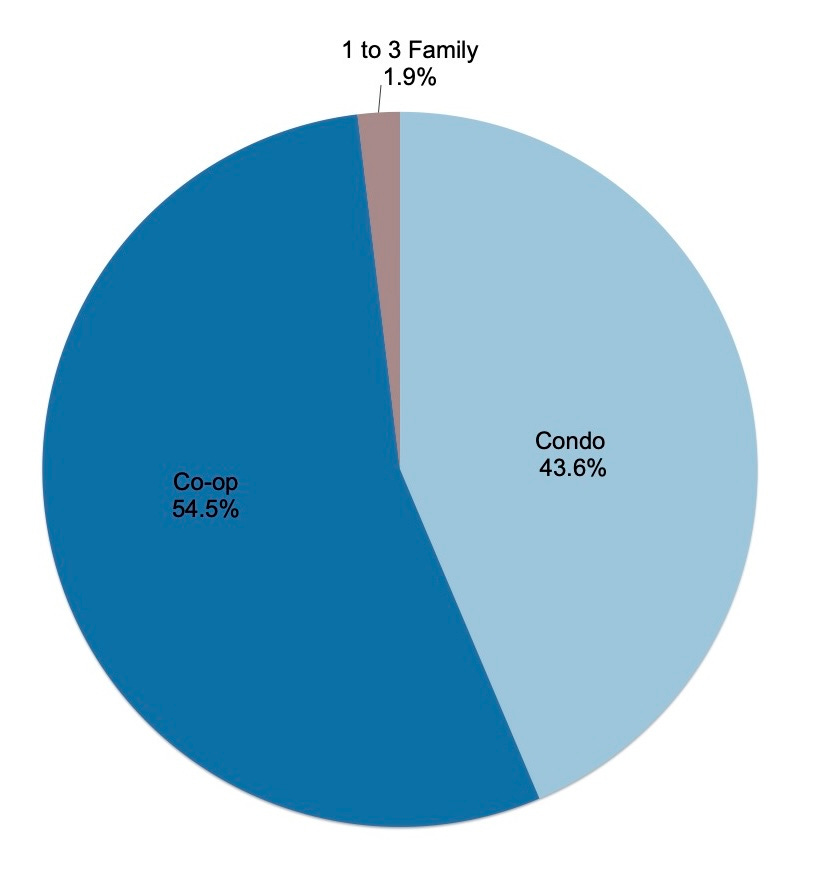

The juxtaposition of pie as both food and chart is a bit ironic, since pie charts are generally bad for data visualization but excellent as food. However, there are sometimes exceptions, especially in the case of the following chart. It is based on the number of residential sales in Manhattan by property type in 4Q25 and is obnoxiously large. You can see how Manhattan townhouses (1-3 families) are essentially a rounding error in the residential housing ecosystem of sales, accounting for ±2% of the sales market, a consistent market share for much of my 40-year Manhattan career.

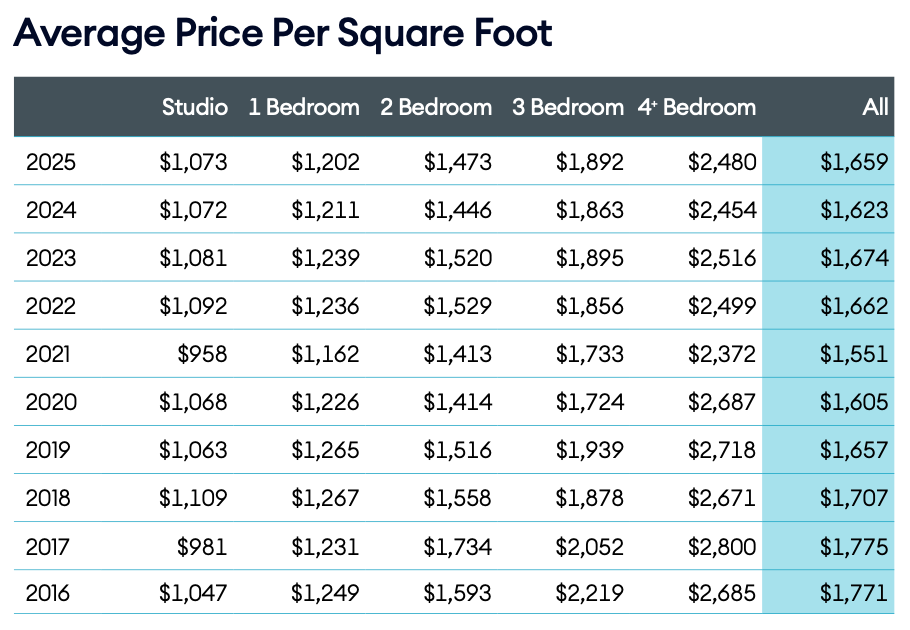

Manhattan has a size formula that has been a housing-market fact during my four decades of valuation experience. In the table below, the premium price per square foot increases with apartment size. The same thing happens when combining two apartments like a studio being purchased by the adjacent owner of a 3-bedroom. In fact, when the studio is purchased, the buyer usually pays much more than the studio is worth because it instantly jumps to the price per square foot of the 3-bedroom before any connection is made or any renovations are performed.

Source: Elliman Report: 2016-2025 Manhattan Decade

Source: Elliman Report: 2016-2025 Manhattan Decade

There is a clear premium for larger, contiguous space, as noted in this 2011 New York Times piece that I was sourced: Combine and Conquer: Your Place and Mine (gift link), so combining apartments seems to yield a higher price per square foot before renovations even begin. But that premium seems to max out at 6,000 to 7,000 square feet (another 6-7 reference).

Source: New York Times

Source: New York Times

These apartment combinations often result in a higher price per square foot.

Source: New York Times

Source: New York Times

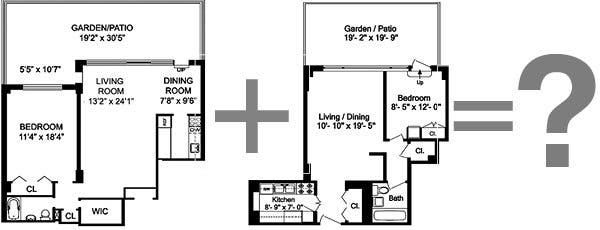

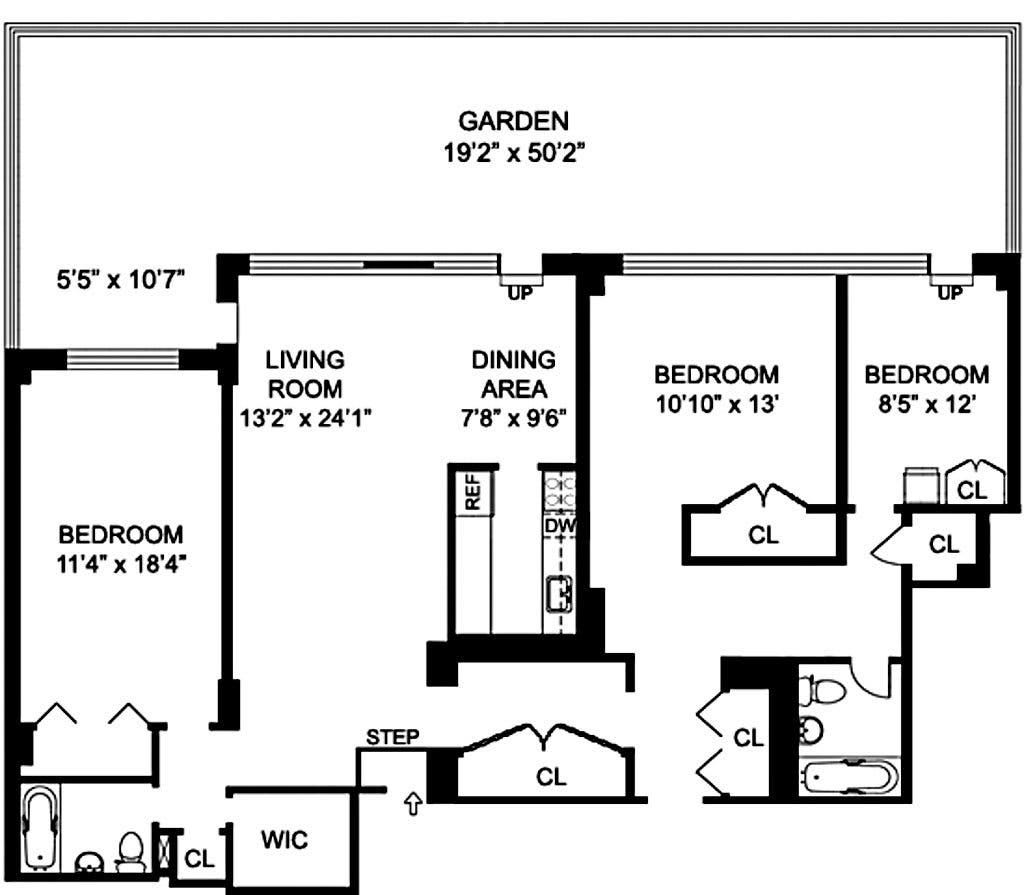

But because the average size of a Manhattan townhouse typically ranges from 4,000 to 5,500 square feet, combining two of them side by side rarely creates a premium contribution like apartments do, because a combination of two properties nearly always bumps up against that size 6,000-7,000 square foot threshold. We see this phenomenon in the very large Soho loft market as well. If the final layout is awkward or the construction quality is low, the value premium of 1+1 may be much closer to 2.0, or even less, after netting out hard and soft costs.

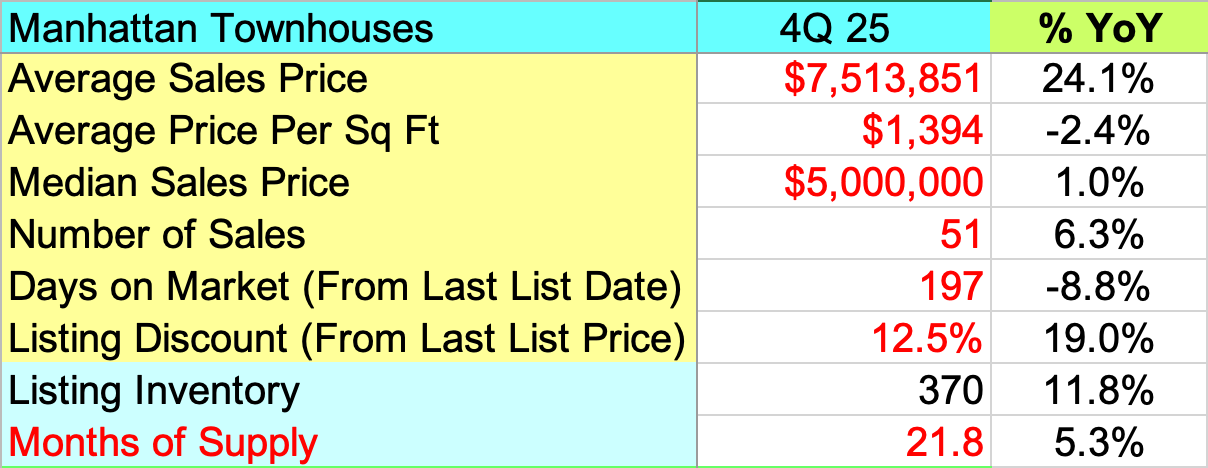

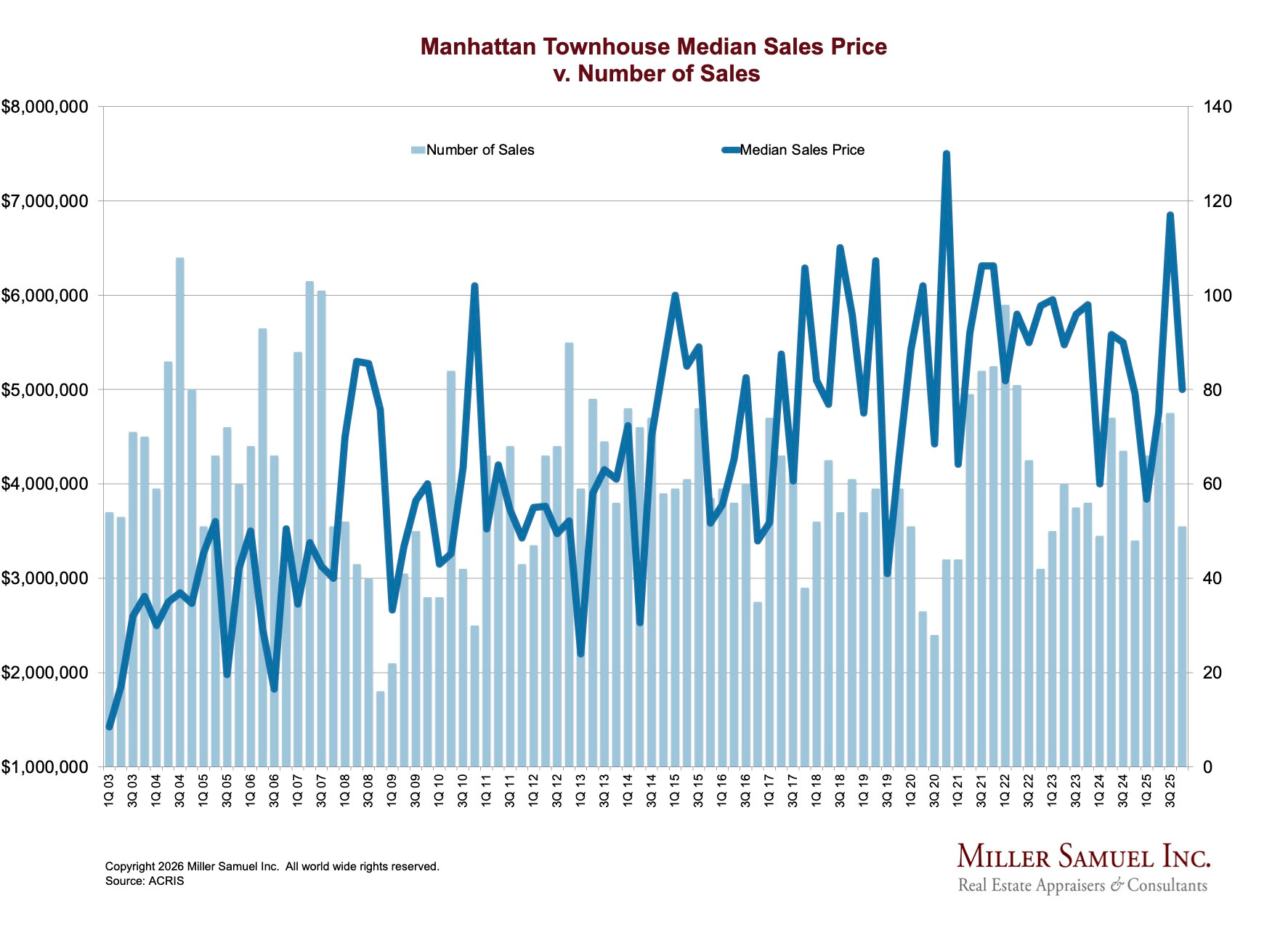

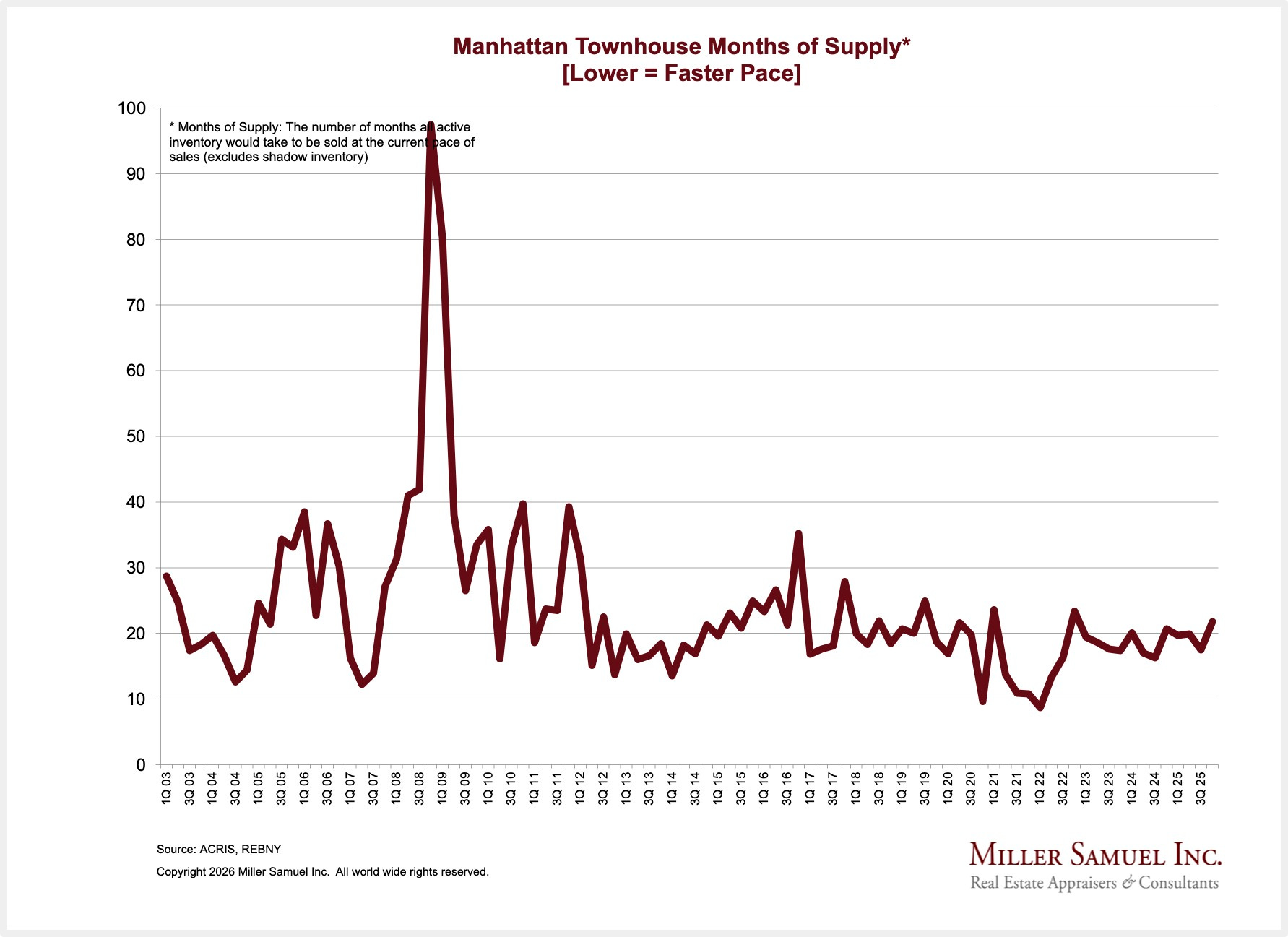

The following is a screenshot of our internal 4th quarter Manhattan townhouse metrics and their annual performance, since I don’t have a formal report to share.

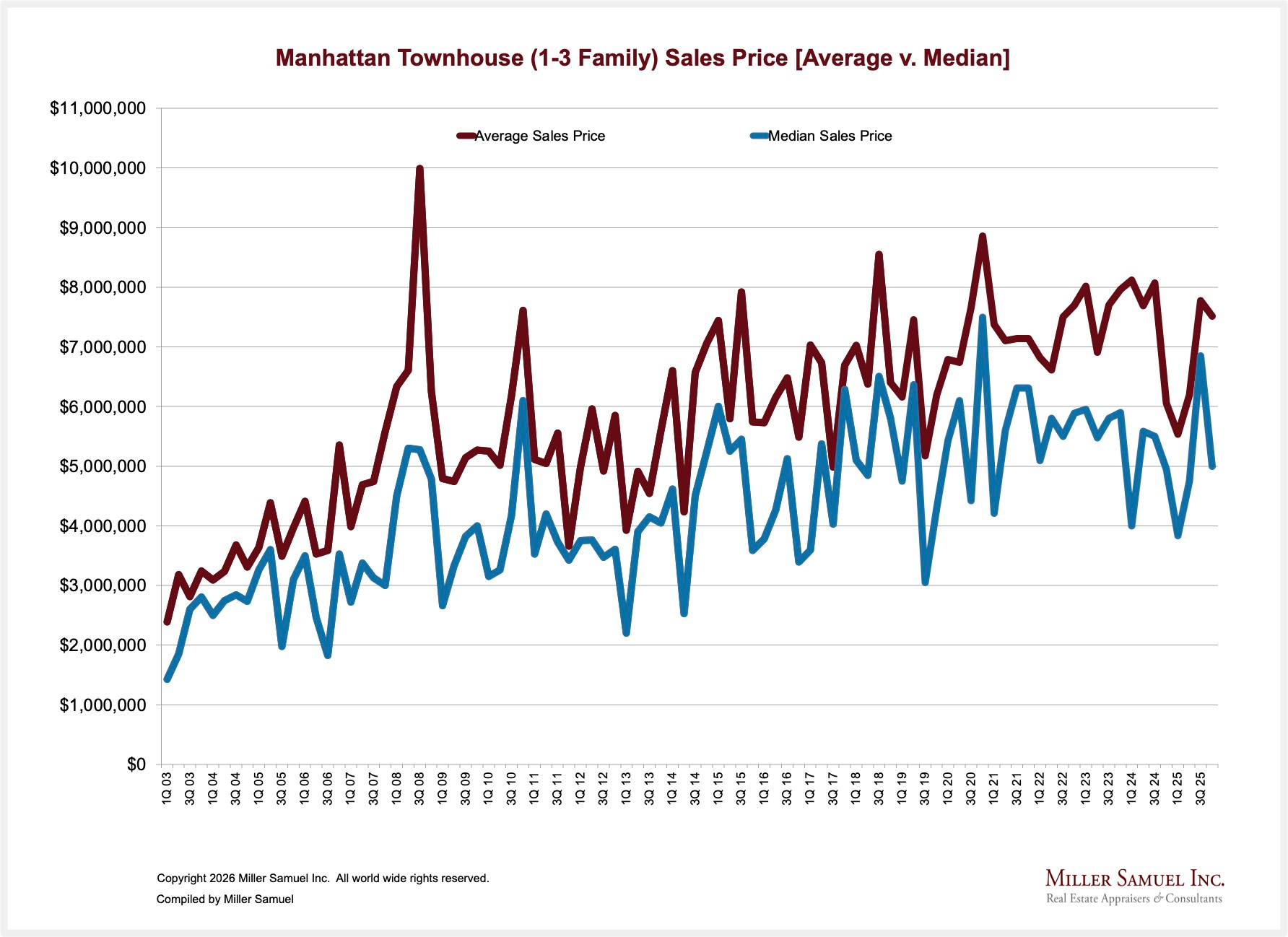

Over the last few years, price trends seem to be leveling off, but the long-term trend shows rising prices.

Coming out of the pandemic era, Manhattan townhouse sales, like apartment sales, have returned to more normalized levels over the past several years.

The months of supply, the number of months it would take to sell all listings at the current sales rate, has been remarkably steady at around 20 months for the past dozen years.

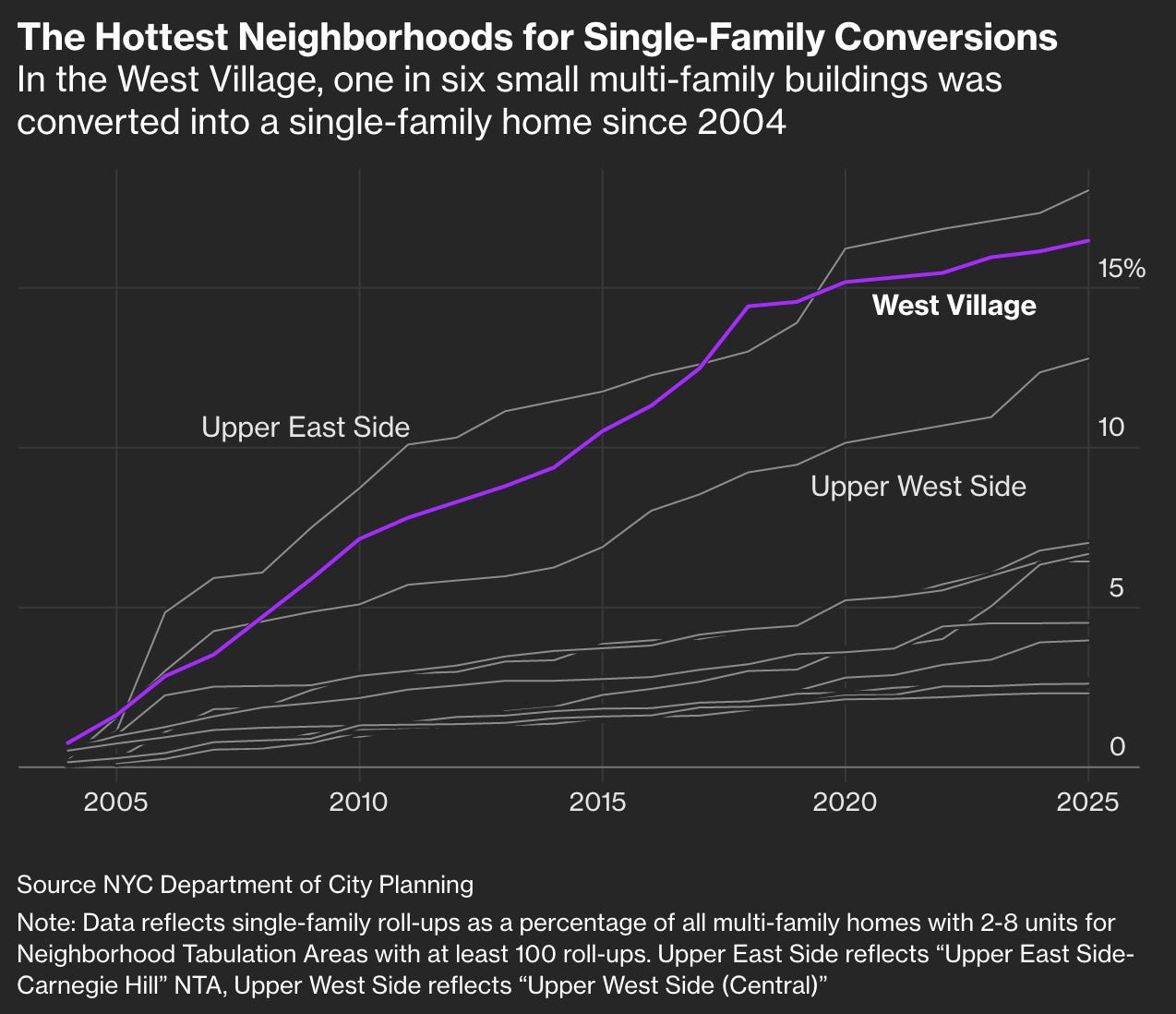

Bloomberg’s CityLab unleashes a spectacular visualization in “The Rise of the Manhattan Mega-Mansion” (gift link). It’s an amazing presentation.

Source: Bloomberg CityLab

Source: Bloomberg CityLab

The visualization follows the typical path of these historic townhouses. They tend to be built as single family properties and, over time, especially after World War II, are converted to multi-family. Eventually, someone buys them and converts them back to a single family configuration because that’s their highest and best use in the market. In other words, there is a growing demand for larger townhouses. In NYC, Bloomberg found that two or more townhouse combinations have resulted in 169 fewer housing units. The largest concentrations of these combinations tend to be in the West Village, the Upper East Side, and the Upper West Side, all in Manhattan.

These combined houses are reducing the number of housing units available in the market, and the widening wealth gap is making this phenomenon more common. While I’ve been in several combined townhouses over the years, the layouts often don’t work. Two adjacent townhouses might not have the same floor heights, so crossing from one property to another requires a step, and the floors can be further apart on higher floors. The key is to combine two adjacent historic rowhouses that were built at the same time by the same architect.

However, even when these combinations are done, their excessive size does not provide a bump in price per square foot after accounting for the improvement in condition. The new type of buyers seeking these out want more contiguous space, which they clearly pay for, but it doesn’t add a premium to the resulting project’s value before renovations. Perhaps down the road, after considering how difficult it is to create these townhouse combinations, the market will recognize a premium for them on a per-square-foot basis. At this point, who knows? And the search for premium is not the economic driver of this market phenomenon.

Manhattan townhouses account for only about 2% of residential sales and constitute a niche within the broader housing market, even as long-term prices have trended higher. Larger, contiguous space commands a clear price-per-square-foot premium in Manhattan apartments, especially when units are combined, up to roughly 6,000–7,000 square feet. Combining two townhouses usually overshoots that size threshold and rarely produces a similar premium, particularly if layouts are awkward or construction quality is poor. Recent analysis shows townhouse sales and months of supply have normalized and remained steady post-pandemic, while Bloomberg’s visualization of “mega-mansion” conversions highlights how double-wide and larger townhouse combinations in affluent neighborhoods have actually reduced the city’s housing-unit count, catering to wealthier buyers’ appetite for more space without meaningfully lifting value per square foot beyond what improved condition alone would justify.

In other words, the creators of these Manhattan mega-mansions are not being incentivized by a price premium, but rather by the desire for larger, contiguous space.

The Actual Final Thought – I need ANSWERS again! Oh my goodness.