Manhattan Associates (MANH) has been back on investors’ radar after management used the 47th Annual Raymond James Institutional Investor Conference to highlight record fourth quarter bookings, strong new customer contributions, and confidence in cloud revenue growth.

See our latest analysis for Manhattan Associates.

At a share price of US$147.00, Manhattan Associates has seen a 5.29% 7 day share price return and an 8.38% 30 day share price return. Its year to date share price return of 12.12% and 1 year total shareholder return of 13.05% suggest that recent momentum is still rebuilding after earlier weakness, with investor attention now centering on record bookings, the enlarged US$500m buyback authorization, and the planned CFO transition to long time finance leader Linda Pinne.

If this focus on supply chain software is on your radar, it could be a good moment to scan beyond Manhattan Associates and check out 35 AI infrastructure stocks as another way to find AI related infrastructure names catching market interest.

With shares still down 12.12% year to date and 13.05% over 1 year, yet trading at a reported 38% discount to an intrinsic estimate, you have to ask yourself: is this a reset buying chance, or is the market already baking in future growth?

Most Popular Narrative: 8.1% Undervalued

With Manhattan Associates last closing at $147 and the most followed narrative pointing to a fair value of $160, the valuation debate turns on a handful of specific growth and margin assumptions rather than sentiment alone.

The broader market’s unpredictable tariff environment may lead to volatility in inventory costs, influencing earnings as companies reconsider their purchasing commitments, potentially impacting Manhattan Associates’ sales pipeline and cloud bookings. The company has cited that some of its customers are electing longer ramp timelines for implementation, which could decelerate revenue recognition from contracted RPO, affecting Manhattan Associates’ overall short term revenue growth trajectory.

Curious how a slower cloud ramp, tempered revenue assumptions and reworked profit margins can still support that higher fair value tag? The narrative leans on specific earnings forecasts, a premium future P/E and a tighter discount rate to bridge today’s price to that $160 figure, but the exact mix of those levers is where the story really gets interesting.

Result: Fair Value of $160 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, if cloud growth or margins fall short of those higher P/E assumptions, or if sector demand for warehouse and industrial tech cools, that $160 fair value argument weakens.

Find out about the key risks to this Manhattan Associates narrative.

Another View: Rich P/E Puts The Spotlight Back On Risk

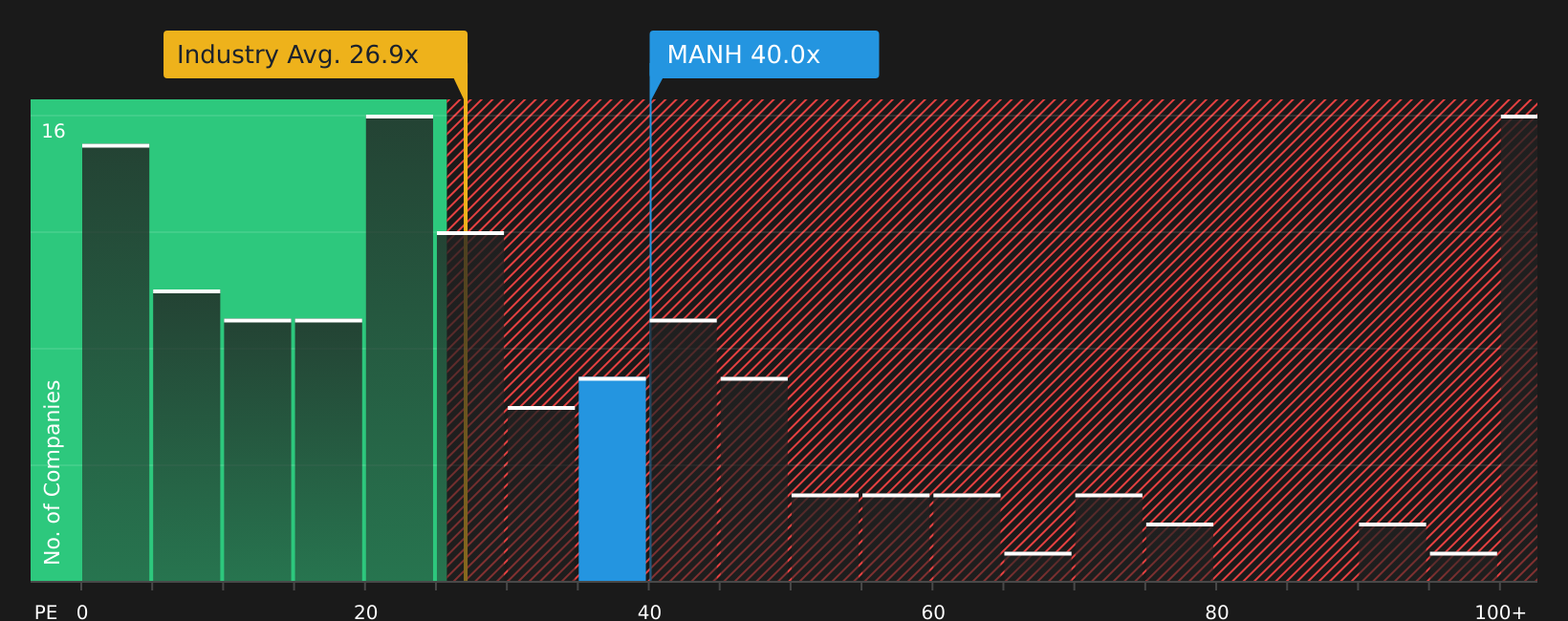

That 8.1% discount to a $160 fair value leans on detailed forecasts, but the current P/E of 40x tells a different story. It sits well above the US Software industry at 26.6x, peers at 34.2x, and an SWS fair ratio of 27.1x, which raises clear valuation risk questions.

See what the numbers say about this price — find out in our valuation breakdown.

NasdaqGS:MANH P/E Ratio as at Mar 2026Next Steps

NasdaqGS:MANH P/E Ratio as at Mar 2026Next Steps

If the mixed signals in this article leave you undecided, act while the data is fresh and form your own view by checking the company’s 4 key rewards.

Looking for more investment ideas?

If this story has sharpened your thinking, do not stop here. Give yourself more options by lining up a few fresh ideas in your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com