The big four rating agencies aren’t happy with Mayor Zohran Mamdani.

Moody’s, Standard & Poor’s, Fitch and Kroll, which each assign a letter grade to the bonds New York City sells to finance its debt, have warned they may reduce their rating because Mamdani intends to dip into the city’s reserves at a time when revenue is growing.

The rating agencies are not outliers. The mayor’s plan has been panned by both the state and city comptrollers, fiscal watchdogs and even the City Council.

But that doesn’t mean a downgrading will have serious consequences. If bonds are downgraded, the move will not lead to a jump in the interest rates the city pays on its bonds — because the city is such a crucial source of bonds for buyers of state and local debt. And, more importantly, a bond rating is not a measure of whether a state or city is acting in the best interests of its constituents.

“A bond rating is no more a measure of a mayor or governor than a credit score is a grade on whether you are a good parent,” said Matt Fabian, the president of Municipal Market Analytics, an independent bond analysis firm.

“Would you be a good parent if you didn’t help your children financially to go to college to keep your credit score high?”

While the mayor seems to have proposed using reserves, as well as a property tax increase, to pressure Albany to raise taxes on the wealthy and corporations, the plan to dip into the rainy-day fund has touched a nerve with budget experts especially.

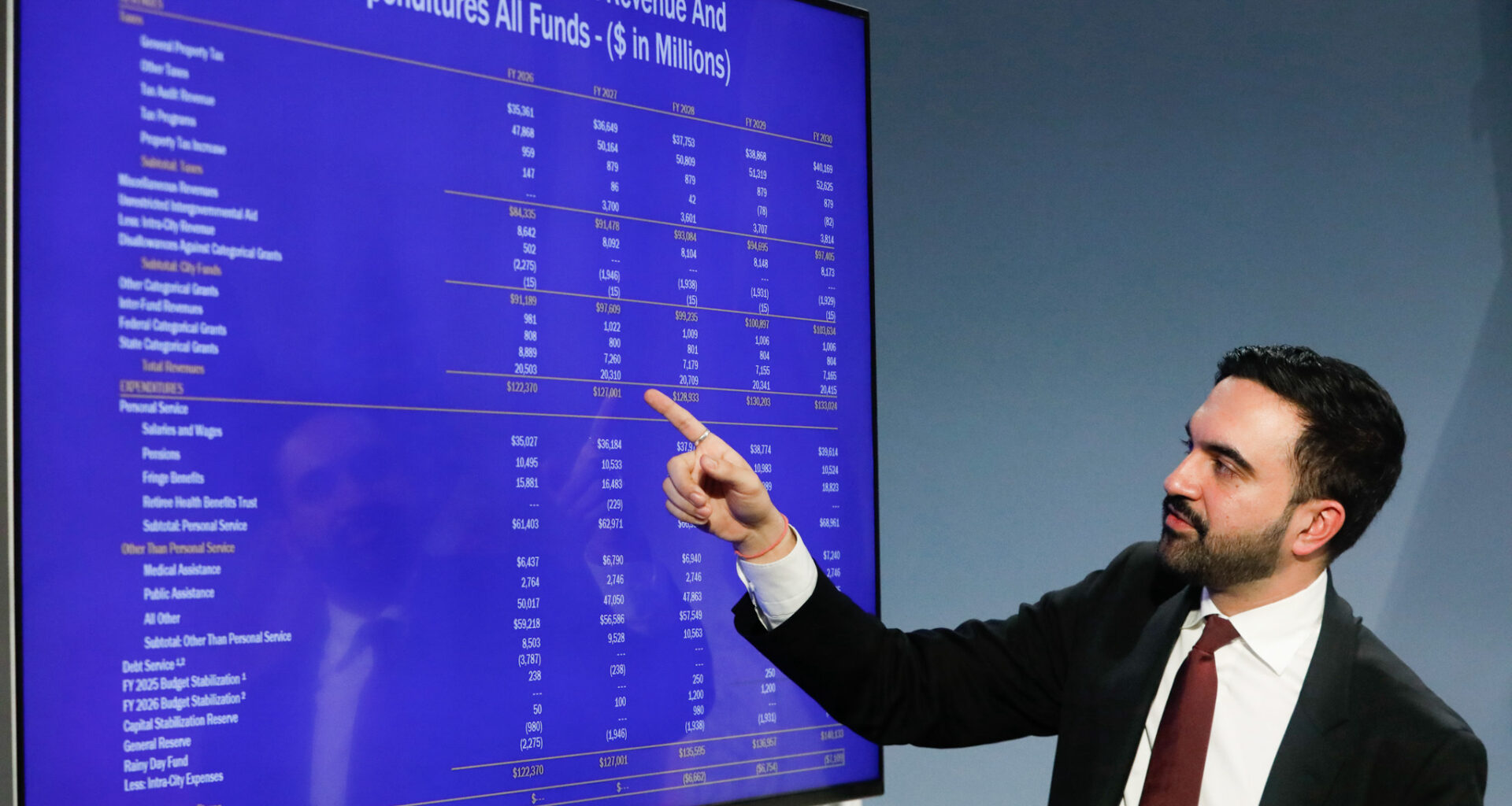

The city has built up a cushion of $8 billion, which is designed to be used to avoid steep budget cuts when the economy heads into a recession and tax revenues plummet.

“Rainy day reserves should be saved for a recession or severe emergency,” said Ana Champeny, research director of the Citizens Budget Commission, which has been among those opposing the Mamdani plan.

“Look no further than global instability, weak job creation and a possible AI bubble to remember that the economy can swing down as well as up. Using reserves as a one-shot budget hole patch is misguided. It both leaves NYC to face the same hole next year and leaves it less prepared to protect New Yorkers from the next recession,” said Champeny.

The $8 billion figure is the highest in the city’s history, but former Mayor Eric Adams and the City Council didn’t increase it in recent years, meaning that it has declined as a percentage of the budget.

State comptroller Tom DiNapoli and former city Comptroller Brad Lander have repeatedly called for the city to increase reserves in recent years.

The four rating agencies all put the city on what is known as a watch list because of the budget proposal.

“The downside risk to our rating on New York City could materialize if we believe two conditions persist: the city relies on nonrecurring budget solutions that fail to reduce the structural mismatch between recurring revenue and expenditures; and the city’s reserves erode to a point where its capacity to absorb an economic downturn or a federal funding shock is materially diminished,” Moody’s said.

Moody’s rates New York bonds at Aa2, which is only slightly below the highest possible rating of AAA.

But even if the rating is lowered, estimates of its impact have been greatly exaggerated.

A City Council study leaked to the New York Post this week assumed that the rate on the city’s bonds would increase from 6% to 6.25% and claimed that would cost the city $400 million a year and increase interest fees by $3.6 billion over the lifespan of the city’s various bonds.

However, a rating downgrade does not affect the interest rate on bonds already issued by the city, only new bonds the city sells. So, if the city sold $5 billion in bonds in the next year, the added cost would be about $12 million a year or $360 million over the life of $5 billion in 30-year bonds.

In fact, the interest rate on the city’s last sale of 30-year bonds, which carry the highest rate, was less than 5%.

Fabian, who has spent decades studying the bond market, says the cost is unlikely to be anywhere near what the Council claims.

State and local bonds are often bought by wealthy taxpayers because the interest is exempt from federal income taxes. New Yorkers who buy New York bonds also receive an exemption from state and local income taxes, making it an extremely attractive investment, keeping demand high and interest rates relatively low.

Since New York is also such a big force in the market, with $65 billion in bonds outstanding, and its economy is the biggest in the country, demand will continue to be strong, he says.

“At most I would expect a downgrade to cost the city a couple of basis points,” he said.

A basis point is one hundredth of one percent.

Related