Erie Indemnity (NasdaqGS:ERIE) raised its dividend for the 36th consecutive year, extending its long record of annual increases. This latest dividend hike qualifies the insurer for Dividend Aristocrat status, a label often associated with consistent dividend growth over multiple decades. The announcement reinforces the company’s long running focus on regular cash returns to shareholders.

For you as an investor, a 36 year streak of dividend increases at Erie Indemnity, which operates in the insurance sector, points to a long history of maintaining distributions through different business conditions. Insurance is often viewed as a steadier corner of financial services, where underwriting, claims trends and investment income all feed into the ability to keep paying shareholders.

Dividend Aristocrat status does not guarantee future income, but it does highlight a policy of regularly returning cash to investors. If you are evaluating NasdaqGS:ERIE, this track record may be one factor to weigh alongside balance sheet strength, underwriting quality and your own income targets.

Stay updated on the most important news stories for Erie Indemnity by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Erie Indemnity.

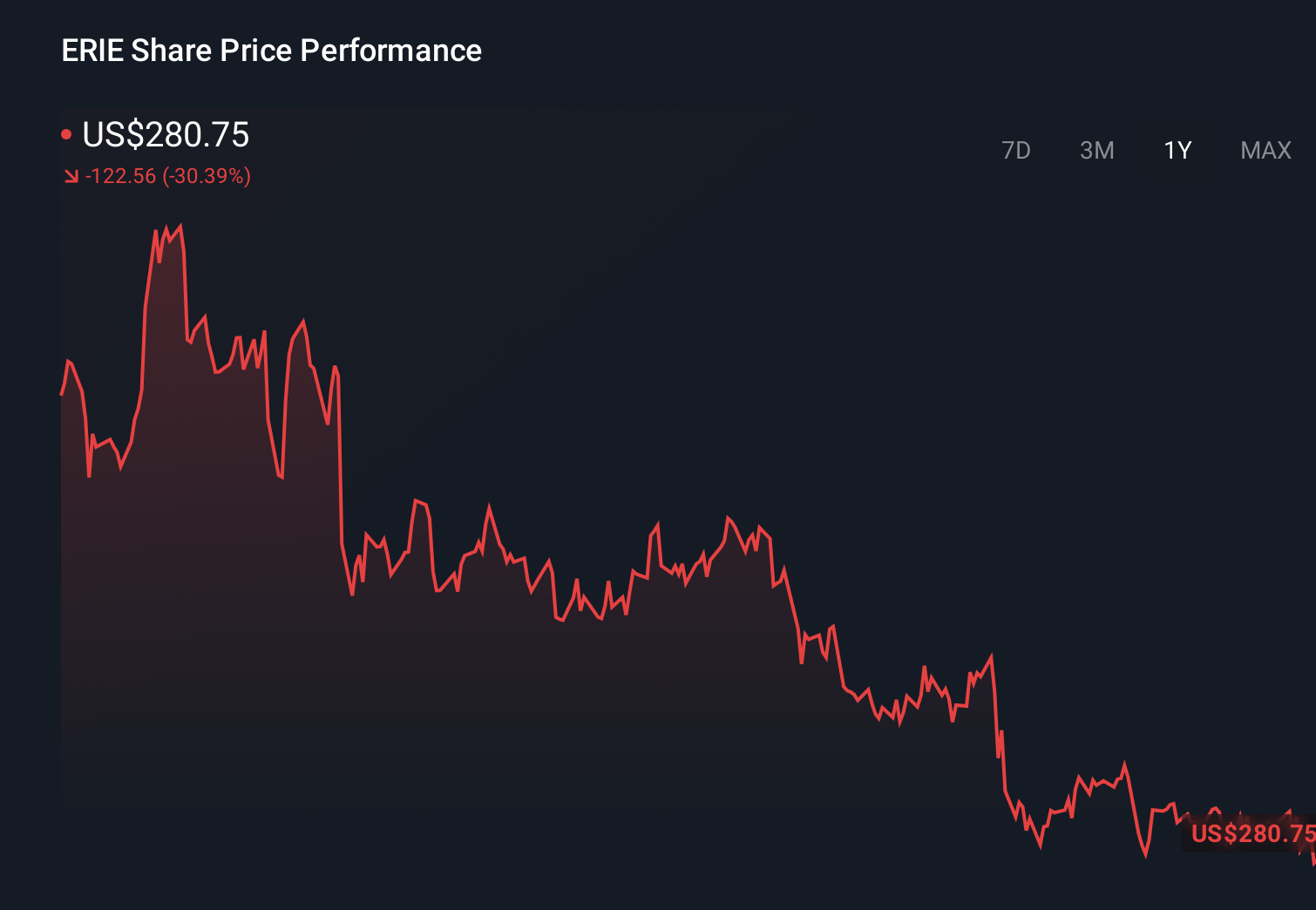

NasdaqGS:ERIE 1-Year Stock Price Chart

NasdaqGS:ERIE 1-Year Stock Price Chart

Why Erie Indemnity could be great value

Quick Assessment ⚖️ Price vs Analyst Target: There is no current analyst price target, so you are relying more on your own assessment than on broker consensus at $280.75. ❌ Simply Wall St Valuation: Shares are flagged as trading about 26.7% above estimated fair value, which points to an overvalued status. ✅ Recent Momentum: The 30 day return of roughly 1.1% suggests the share price has been edging higher recently.

Check out Simply Wall St’s

in depth valuation analysis for Erie Indemnity.

Key Considerations 📊 The new dividend increase and Dividend Aristocrat label reinforce Erie Indemnity’s income track record, which may matter if you are focused on reliability. 📊 Keep an eye on the 2.08% dividend yield, the current P/E of 22.7 versus the insurance industry average of about 13.3, and future earnings delivery against expectations. ⚠️ With shares assessed as 26.7% above estimated fair value, the key risk is paying too much for a high quality dividend story. Dig Deeper

For the full picture including more risks and rewards, check out the

complete Erie Indemnity analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Erie Indemnity might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com