Erie Indemnity recently saw its shares come under pressure as investors reacted to weaker sentiment around the company’s latest financial results and the broader market backdrop. The stock’s slide to a new 52-week low, alongside higher-than-usual trading volume, points to heightened anxiety ahead the February earnings update that has now passed. We will now examine how rising investor concern over recent financial results shapes Erie Indemnity’s investment narrative going forward.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best ‘picks and shovels’ of the AI gold rush converting record-breaking demand into massive cash flow.

What Is Erie Indemnity’s Investment Narrative?

To own Erie Indemnity, you need to believe in the resilience of its fee-based insurance model, its high return on equity and its track record of consistent earnings and dividend growth. The recent drop to a new 52-week low, despite solid year-on-year improvements in revenue and earnings through 2025, suggests sentiment is now a bigger swing factor than the latest reported numbers. That shift matters for the short term: the upcoming Q4 2025 release on February 23 has effectively become a credibility check on recent margin trends and the sustainability of Erie’s high-quality earnings profile. At the same time, the core business risks have not changed much, with valuation sensitivity, slower forecast growth than the broader market and industry competition remaining key pressure points.

However, one emerging risk around Erie’s premium valuation and recent share-price weakness is worth watching closely for any further cracks in confidence.

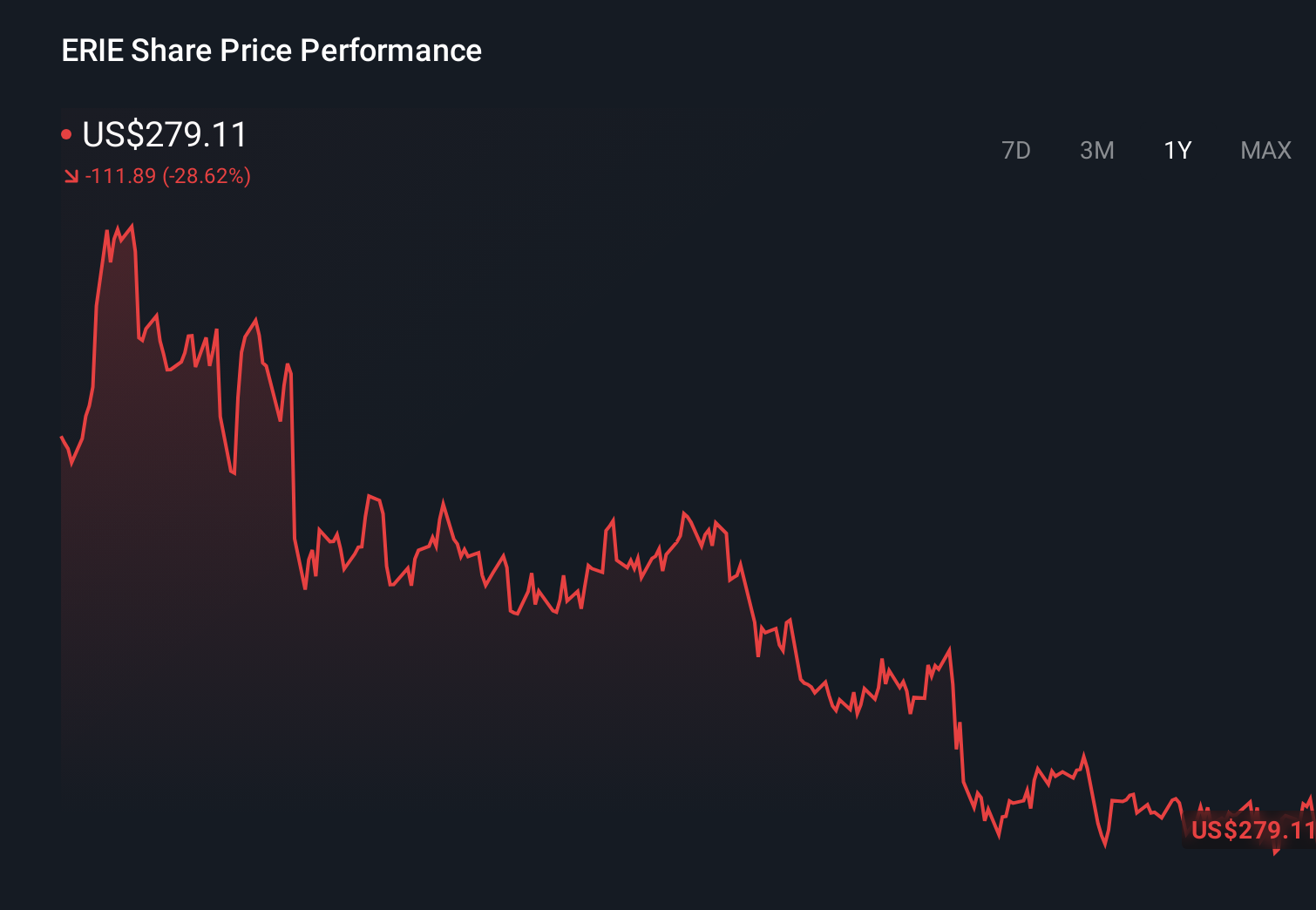

Erie Indemnity’s share price has been on the slide but might be up to 22% below fair value. Find out if it’s a bargain.Exploring Other Perspectives ERIE 1-Year Stock Price Chart With only two Simply Wall St Community fair value views ranging from about US$228 to US$333, you can see how far apart individual expectations sit. Set those against Erie’s recent share-price slide and heightened concern around its upcoming earnings, and it becomes clear why many investors are reassessing what they are willing to pay and what could drive performance from here.

ERIE 1-Year Stock Price Chart With only two Simply Wall St Community fair value views ranging from about US$228 to US$333, you can see how far apart individual expectations sit. Set those against Erie’s recent share-price slide and heightened concern around its upcoming earnings, and it becomes clear why many investors are reassessing what they are willing to pay and what could drive performance from here.

Explore 2 other fair value estimates on Erie Indemnity – why the stock might be worth 18% less than the current price!

Build Your Own Erie Indemnity Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

A great starting point for your Erie Indemnity research is our analysis highlighting 3 key rewards that could impact your investment decision.Our free Erie Indemnity research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Erie Indemnity’s overall financial health at a glance.Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Erie Indemnity might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com