Big raises don’t tell the full story of a region’s startup scene.

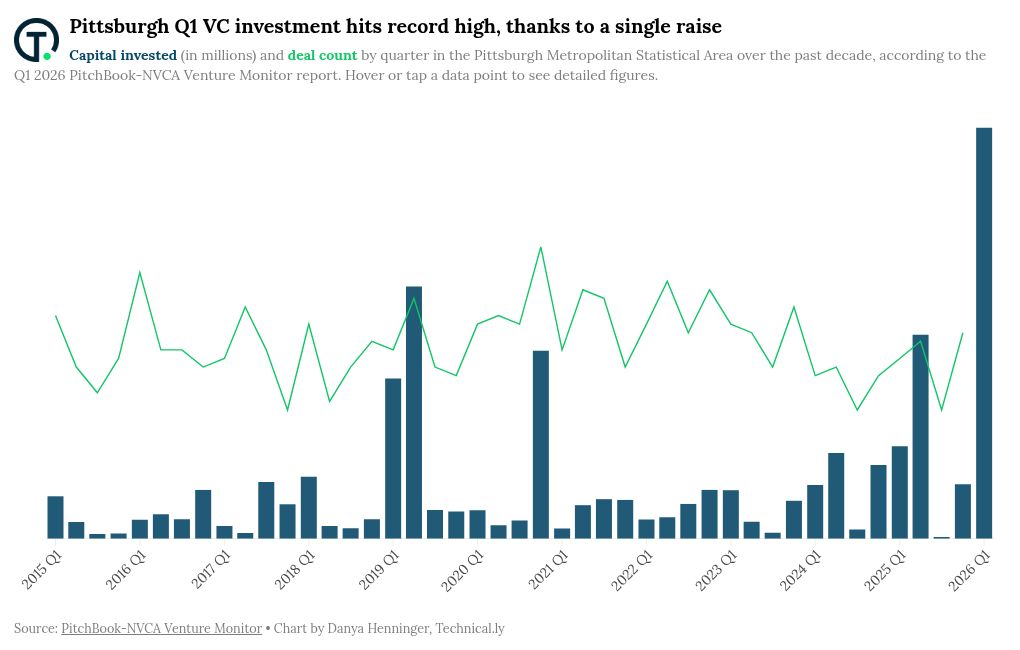

In Q1, companies in the Pittsburgh metro area raised a combined $1.7 billion across 26 deals, according to the latest Venture Monitor report from PitchBook and the National Venture Capital Association. The total raised is above average for the region, and so is the deal count, but more than 80% of the capital was concentrated in just one deal — Skild AI’s $1.4 billion raise from January.

This is part of a larger trend that’s being seen across the US, according to PitchBook experts: More than ever before, capital is being consolidated around a narrower set of perceived winners.

“We didn’t necessarily turn to the coasts, but we definitely had to work with investors outside of Pittsburgh to raise the money we needed.”

Alison Alvarez, BlastPoint

The concentration of capital signals a distinct split in the ecosystem’s needs, according to Lindsay Fairman, managing partner at Pittsburgh-based venture firm BlueTree VC.

“Most of the companies in this quarter’s cohort were at the Series A stage, with very few reaching the B-through-D rounds,” Fairman told Technical.ly. “At BlueTree VC, we’ve observed that our lower capital expenditure companies are becoming capital-efficient and reaching profitability without needing massive growth rounds.”

“For high-capital expenditure companies that do require late-stage scaling, the challenge remains clear,” she added, “we must continue to elevate the Pittsburgh story to attract more national growth-stage allocators to the region.”

If you remove Skild AI’s deal from the region’s total Q1 VC activity, Pittsburgh startup funding still remains steady — even better than usual this quarter. The new total is approximately $300 million, a solid showing for an ecosystem that has a median total raise of roughly $124 million per quarter.

Half of the region’s top 10 deals were Series A. Plus, leading raises show robotics and AI companies are raking in the most funds — a persistent trend in Pittsburgh:

Skild AI — $1.4 billion, Series C

Gecko Robotics — $123.4 million, Series D

Efficient Computer — $60 million, Series A

Gather AI — $40 million, Series B

BERO — $26.9 million, Series A

Wholesome International — $20 million, later-stage VC

BlastPoint — $14.2 million, Series A

Voomi Supply — $10 million, Series A

Profitmind — $9 million, Series A

Freespace Robotics — $6.6 million, early-stage VC

The national picture: concentration escalates

Founders and fund managers outside of the top tier are navigating a market that looks very different from what the numbers suggest, according to Nizar Tarhuni, PitchBook executive vice president of research and market intelligence.

“Concentration has increasingly defined VC over the past couple of years, but Q1 marked a new extreme,” Tarhuni said in the report.

On the national level, if you strip out the five largest transactions in the quarter, both deal and exit figures fall by more than 70%, according to Tarhuni, which doesn’t signal that the market is having a broad recovery, but rather that a shrinking group of players are setting the terms and “record-breaking headlines are obscuring how little has changed for the rest of venture.”

Plus, liquidity is still tight nationally and the IPO window remains mostly closed, he added.

Pittsburgh, however, is uniquely positioned to weather this cycle because it has never thrived on fundraising hype, instead prioritizing capital efficiency, according to Fairman.

“There are numerous paths to a successful exit,” she added, “especially in mergers and acquisitions, that don’t require the massive capital infusions an IPO demands.”

Come prepared, ask big

Founders looking to raise capital in this environment need to lead with numbers, according to Alison Alvarez, cofounder and CEO of BlastPoint, one of the top Q1 dealmakers.

“Develop a pitch that frames your value proposition and ensure you can express the value in numbers wherever necessary,” Alvarez told Technical.ly.

Alvarez recommends having a data room, a shared folder of important business info, ready before your second meeting. Her company had TAM calculations, sales growth numbers, customer testimonials, case studies and competitor analysis available, making it as easy as possible for investors to say yes internally.

And when investors say no, treat it as a data point.

“The most important thing we did was to track why we were turned down and adjust our pitch to anticipate and rebut that refusal before the next investor had a chance to doubt us,” she said.

Serial entrepreneur Skip Smith, who has raised in recent years for his security startup CurvePoint, previously told Technical.ly that since VCs are more inclined to make fewer, bigger bets, founders can benefit from being bold and “ask[ing] for more” money at higher valuations.

Before founders even get to the table, though, investors are prioritizing capital efficiency and tangible traction over hype, according to Fairman.

“My advice would be to prioritize a roadmap that clearly articulates and demonstrates every dollar is invested toward reaching the milestones required for your next inflection point — often the next fundraise — ensuring at least 24 months of runway,” she said.

For startups touting AI to fill in these gaps, be wary of overpromising.

Fairman and Alvarez agreed that AI can be a benefit in the market, but founders must be able to defend its use.

“The emphasis on investing in AI definitely helped us,” Alvarez said. “However, simply being an AI startup wasn’t enough. Our unique approach to AI is what helped us even more. Defensibility is really important and we were able to make a great case for ourselves.”

Who will see the returns?

Of the top 10 deals made last quarter, only 4.5% of the disclosed investors were Pittsburgh-based, according to PitchBook data.

Stakeholders in Pittsburgh’s startup scene have long sounded the alarm that not enough local investors are getting in on the region’s best deals, raising concerns that the value created in this region ultimately leaves it.

“A critical challenge we face is that indigenous capital reserves remain lower than they should be for a region of our caliber,” Fairman said. “To keep this success ‘flywheel’ spinning, we must prioritize increasing our local capital base.”

In the absence of that, top-raising local companies have to predominantly strike deals with coastal and foreign investors to fuel their growth. But with outside capital can come expanded networks or expertise.

“We didn’t necessarily turn to the coasts, but we definitely had to work with investors outside of Pittsburgh to raise the money we needed,” Alvarez from BlastPoint said. “I’m really grateful that we were able to work with a lead not only on the East Coast but also here in Pennsylvania. It’s silly, but being able to travel and be in the same room as our board members fairly easily is a huge asset.”