Track your investments for FREE with Simply Wall St, the portfolio command center trusted by over 7 million individual investors worldwide.

Cheniere Energy (NYSE:LNG) secured approval from the U.S. Department of Energy to expand LNG exports from its Corpus Christi terminal.

The authorization increases Corpus Christi’s role in U.S. LNG trade, making it the second-largest LNG export project in the country.

The decision affects future U.S. LNG supply capacity and global buyers that source cargoes from Gulf Coast terminals.

Cheniere Energy, a major U.S. exporter of liquefied natural gas, now has the green light to ship more LNG from its Corpus Christi facility. For investors tracking NYSE:LNG, this decision sits at the intersection of U.S. energy policy, infrastructure build out, and the global search for reliable gas supply. It also adds another large scale project to the Gulf Coast export network, which already plays a key role in seaborne LNG trade.

Looking ahead, the expanded authorization at Corpus Christi gives Cheniere additional flexibility to contract volumes with overseas buyers and refine its long term commercial plans. For investors, the focus now shifts to how the company manages construction, contracting, and operations under this larger export footprint.

Stay updated on the most important news stories for Cheniere Energy by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Cheniere Energy.

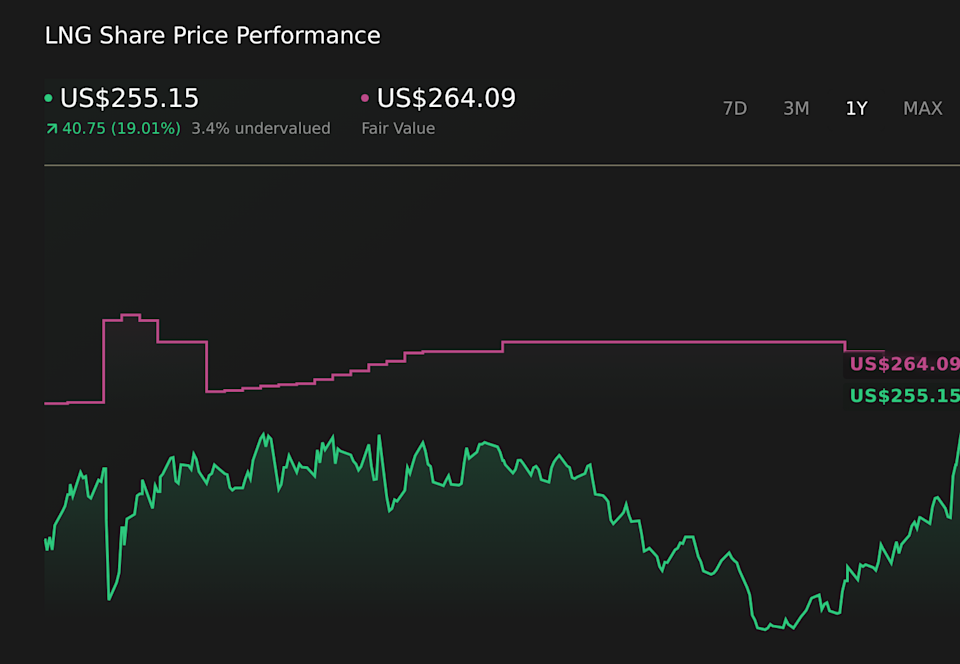

NYSE:LNG 1-Year Stock Price Chart

NYSE:LNG 1-Year Stock Price Chart

The Department of Energy approval comes alongside Cheniere’s decision to issue US$1.75b of new senior notes, which is important context for anyone looking at the company’s balance sheet. The 2036 notes carry a 5.200% coupon and the 2056 notes 6.000%, both issued just below par, so Cheniere locks in fixed long dated funding while accepting a modest interest cost. Because the notes rank equally with existing senior debt and proceeds are earmarked for refinancing, capital expenditure on projects like Corpus Christi, working capital and other uses, the headline increase in gross debt may not translate into the same increase in net leverage if older, potentially higher cost facilities such as the Corpus Christi term loan are repaid.

The new notes provide long term capital that can support ongoing LNG capacity expansion and debottlenecking. This is a key theme in the existing narrative around growth in export volumes and contracted cash flows.

At the same time, relying on sizeable debt to fund projects adds sensitivity to LNG market cycles and demand uncertainty. The narrative already flags this as a risk around potential oversupply and returns on future capacity.

The specific choice to issue long dated fixed rate debt and potentially retire term loans is not fully covered in the narrative. However, it directly affects how resilient future free cash flow might be if market conditions soften.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for Cheniere Energy to help decide what it is worth to you.

⚠️ The company already has a high level of debt, and adding US$1.75b of senior notes increases interest obligations that need to be covered through future LNG exports and existing contracts.

⚠️ Analysts expect earnings to decline by an average of 15.5% per year over the next 3 years, so higher fixed interest costs could tighten coverage if that outlook materialises.

🎁 Earnings grew by 63.4% over the past year, which can give Cheniere more room to manage its capital structure and absorb the cost of new long term funding.

🎁 Shares are trading at what is described as good value compared to peers and industry and around 26.8% below one estimate of fair value, which some investors may see as a cushion while the company invests in growth projects.

From here, you may want to watch how much of the US$1.75b is used to retire existing borrowings versus funding new Corpus Christi related capex, and how that filters through to net debt and interest expense. Progress on Trains 8 and 9, contract signings with buyers and any updates to earnings guidance will help you judge whether the larger export footprint and higher fixed financing costs are tracking in line with expectations. It can also be useful to keep an eye on how competitors such as Freeport LNG, Sempra and other Gulf Coast exporters finance their projects, as that gives context on industry wide leverage and pricing power.

To ensure you are always in the loop on how the latest news impacts the investment narrative for Cheniere Energy, head to the community page for Cheniere Energy to stay up to date on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include LNG.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com