Since April 2021, the S&P 500 has delivered a total return of 68.6%. But one standout stock has more than doubled the market – over the past five years, Texas Pacific Land has surged 148% to $426.79 per share. Its momentum hasn’t stopped as it’s also gained 36.4% in the last six months, beating the S&P by 31%.

Is now still a good time to buy TPL? Or are investors being too optimistic? Find out in our full research report, it’s free.

One of America’s largest private landowners with roughly 868,000 acres in the Permian Basin, Texas Pacific Land (NYSE:TPL) owns land in West Texas and earns revenue from oil and gas royalties, water services, and land leases.

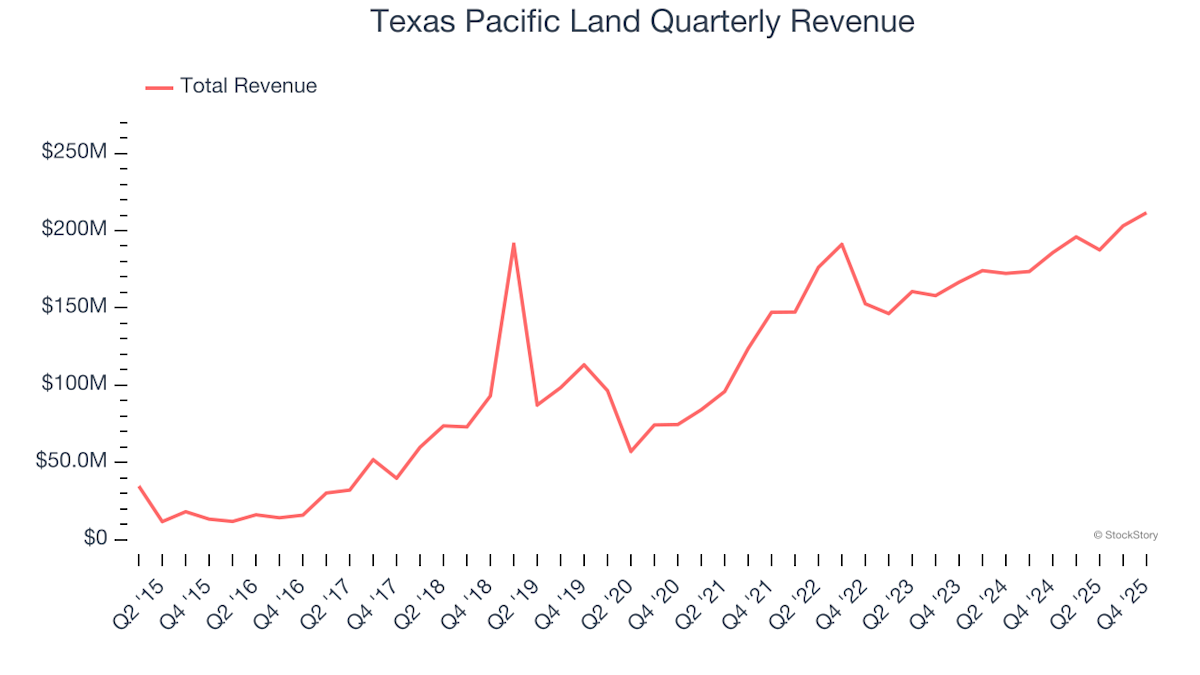

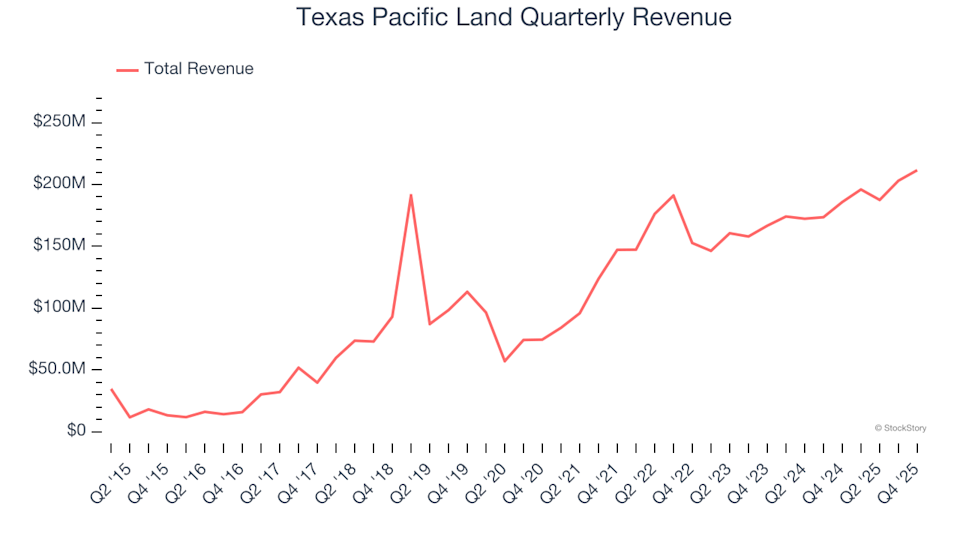

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Thankfully, Texas Pacific Land’s 21.4% annualized revenue growth over the last five years was excellent. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Texas Pacific Land Quarterly Revenue

Texas Pacific Land Quarterly Revenue

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Texas Pacific Land, which averaged 95% gross margin over the last five years, exhibits enviable unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an advantaged starting point for ultimate operating profits and free cash flow generation.

Texas Pacific Land Trailing 12-Month Gross Margin

Texas Pacific Land Trailing 12-Month Gross Margin

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Texas Pacific Land has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging an eye-popping 62.3% over the last five years.

Texas Pacific Land Trailing 12-Month Free Cash Flow Margin

These are just a few reasons why we’re bullish on Texas Pacific Land, and with its shares beating the market recently, the stock trades at 31.2× forward EV-to-EBITDA (or $426.79 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.