Advanced Micro Devices (AMD) and Palantir Technologies (PLTR) are both prominent artificial intelligence (AI) players, but operate in different parts of the AI ecosystem. AMD designs cutting-edge AI hardware, while Palantir develops AI-powered data analytics software. AMD serves a wide range of enterprise clients, such as data centers and cloud providers, giving it a strong position in the growing AI hardware market. In contrast, Palantir relies heavily on government and defense contracts, which makes it vulnerable to political and budget-related risks.

Meet Your ETF AI Analyst

Amid growing concerns of an “AI bubble” and a slowing global economy, both companies face distinct challenges and opportunities that shape their risk-reward profiles.

AMD Boasts Strength in Hardware Innovation

AMD recently reported better-than-expected third-quarter results and offered upbeat guidance, signaling strong demand for its AI infrastructure products. However, much of this optimism was already reflected in the share price, leading to a modest post-earnings pullback. At its Financial Analyst Day on November 11, AMD announced ambitious goals, including a 35% total revenue CAGR, 60% data center growth, and a $100 billion AI revenue target by 2030.

Loop Capital analyst Gary Mobley initiated coverage of AMD with a Buy rating and $290 price target, implying nearly 17% upside potential. He emphasized AMD’s potential to grow data center revenue, expand share in server and PC markets versus Intel (INTC), and reach over $20 in non-GAAP earnings per share within five years. He even cited challenges, including competition from Arm (ARM) licensees, margin sacrifices entering data center GPUs, Nvidia’s (NVDA) AI GPU lead, and custom AI chips.

Meanwhile, Goldman Sachs analyst James Schneider reiterated his Hold rating and $210 price target, implying 15.3% downside potential. He cited AMD’s promising long-term growth targets but remained cautious about the company’s reliance on its OpenAI partnership and execution risks.

Palantir Is Expanding AI Software Lead

Palantir also reported blockbuster Q3 results and raised its full year guidance, yet shares fell nearly 8% after the results. Analysts and investors remain skeptical about Palantir’s high valuation, especially after famed investor Michael Burry disclosed bearish bets against the company. Many analysts acknowledge Palantir’s growth momentum but view its valuation as pricing in years of future success.

Recently, Morgan Stanley analyst Sanjit Singh kept his Hold rating on PLTR, while raising the price target from $155 to $205, implying 19.1% upside potential. Singh highlighted that Palantir’s revenue growth accelerated for the ninth consecutive quarter, reaching 63%. He expects this momentum to continue, with Q4 guidance forecasting 61% growth driven by strong bookings in Q3.

Conversely, Freedom Capital Markets analyst Almas Almaganbetov kept his Sell rating on PLTR, but raised his price target from $125 to $170, implying 31.4% downside potential. He warned that U.S. commercial demand could cool next year due to tighter budgets and rising costs from AI talent hiring. Despite solid near-term performance, he argued that Palantir’s valuation leaves little room for disappointment.

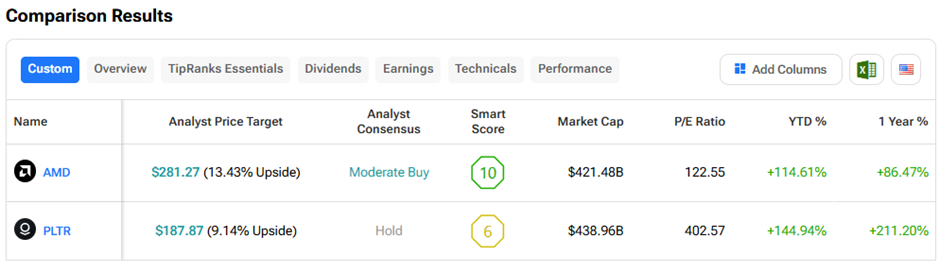

AMD vs PLTR: Which Is the Better AI Stock, According to Analysts?

We used the TipRanks Stock Comparison Tool to determine which AI stock among the two is currently favored by analysts.

AMD stock has a Moderate Buy consensus rating, a higher upside potential over the next twelve months, and a Smart Score of Perfect 10, implying it is highly likely to outperform expectations.