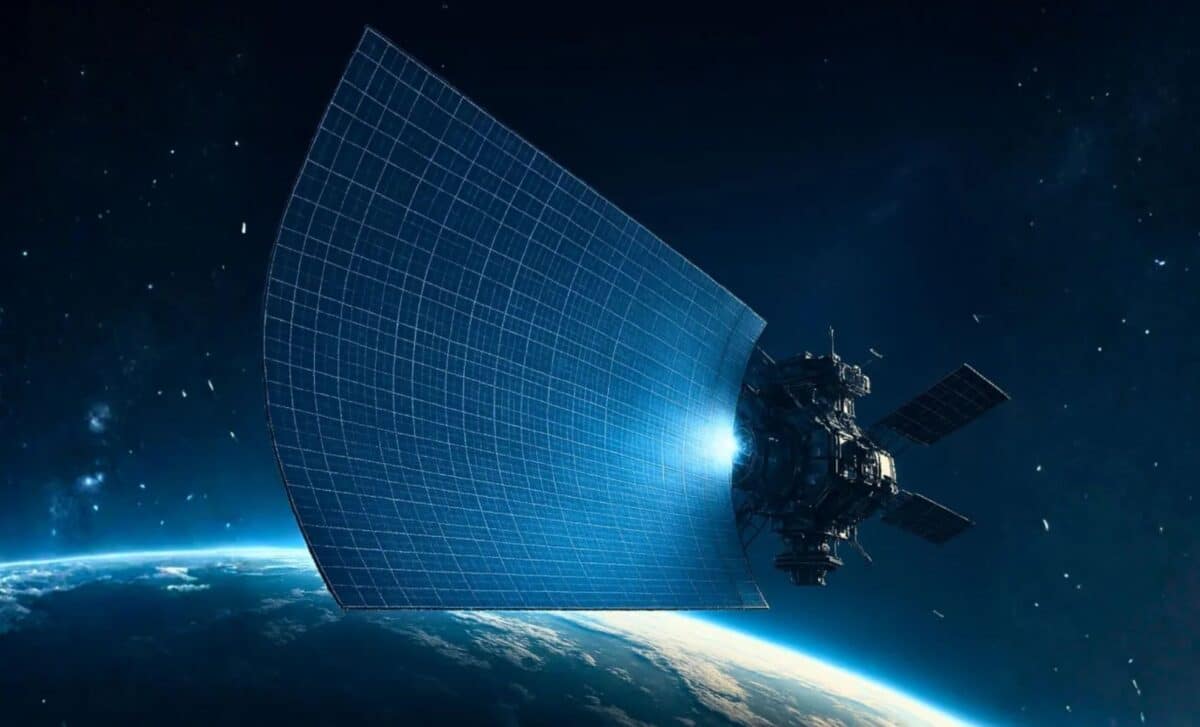

In a year already packed with aerospace milestones, one upcoming satellite launch could redraw the map of global telecommunications. Texas-based AST SpaceMobile is preparing to launch what it calls the largest commercial communications satellite ever placed in low Earth orbit (LEO). Weighing 6.5 metric tons and stretching over 220 square meters of phased-array antennas, BlueBird 6 isn’t just a hardware marvel—it’s a signal flare for a rapidly evolving sector where space-based networks are gaining ground.

Unlike traditional satellite internet systems that require dish terminals or fixed infrastructure, AST’s system is built to beam broadband connectivity directly to standard smartphones. No tower, modem, or router—just the sky above. If it works, the technology could disrupt entrenched terrestrial networks and reframe the economics of mobile coverage, especially in rural and underserved areas.

But technological promise is only part of the story. Backed by more than $3.2 billion in liquidity, bolstered by global telecom partners like Verizon, Vodafone, and stc Group, AST is orchestrating a constellation campaign that could see 60 satellites in orbit by the end of 2026. The company reports over $1 billion in contracted revenue commitments, a rare milestone for a still-pre-revenue aerospace firm.

The Launch That Could Reshape Terrestrial Coverage

The first orbital piece of AST’s network, BlueBird 6, is scheduled to launch in early December from India’s Satish Dhawan Space Centre, according to company financial filings. With its vast antenna array and 10 GHz of signal processing bandwidth, the satellite is designed to offer up to 120 Mbps of throughput per cell, with coverage extending across thousands of simultaneous mobile connections.

Unlike Starlink, which requires user terminals and dishes, AST’s direct-to-device (D2D) approach works with unmodified smartphones, leveraging standard 4G and 5G protocols. It’s a technically ambitious approach that, if proven, would eliminate the need for ground-based towers in hard-to-reach locations.

BlueBird 7 is set to follow, launching from Cape Canaveral, while satellites 8 through 19 are already in various stages of production. AST expects to conduct five orbital launches by the end of Q1 2026, with launches continuing every one to two months after that.

According to its Q3 investor release, AST aims to complete 45–60 orbital deployments by the close of 2026. This first generation—Block 1—is intended to deliver intermittent national coverage across the United States, Canada, Saudi Arabia, Japan, and the United Kingdom by early 2026.

Billion-Dollar Bets and Global Telecom Integration

Beyond engineering, AST’s business strategy is aggressively aligned with legacy telecom operators. Its 10-year agreement with stc Group includes a $175 million prepayment for future services, targeting coverage across Saudi Arabia and other MENA markets. Meanwhile, its expanded agreement with Verizon, announced earlier this year, positions AST to deliver 100% geographical coverage across the continental United States.

In Europe, AST is collaborating with Vodafone to build a new constellation serving European network operators. The company plans to base its satellite operations in Germany, reinforcing its EU footprint. These deals give AST near-immediate integration with over 50 mobile network operators representing nearly 3 billion global subscribers.

At a time when over 2.7 billion people remain offline, mostly in underserved or rural regions, AST is positioning itself as the scalable alternative to ground-based infrastructure.

AST reported $14.7 million in revenue for Q3 2025, driven primarily by U.S. government contract milestones and gateway hardware deliveries. Despite a $123 million net loss for the quarter, its financial cushion—secured through a $1.15 billion convertible note offering—places it among the best-capitalized players in the direct-to-device race.

Credit: NASA/Shutterstock

Credit: NASA/Shutterstock

A Crowded Sky and Rising Regulatory Pressure

AST reported $14.7 million in revenue for Q3 2025, driven primarily by U.S. government contract milestones and gateway hardware deliveries. Despite a $123 million net loss for the quarter, its financial cushion—secured through a $1.15 billion convertible note offering—places it among the best-capitalized players in the direct-to-device race.

The pace of satellite deployment globally is accelerating. In the past 12 months alone, 3,664 satellites were launched into orbit. As of October 1, 2025, there were 15,965 active satellites, according to the Union of Concerned Scientists Satellite Database, with 13,026 currently operational.

AST’s constellation would add dozens more to the already congested LEO environment, raising renewed concerns about orbital debris, electromagnetic interference, and sky visibility for ground-based astronomy. Unlike geostationary satellites, LEO systems require far greater numbers to achieve continuous coverage, compounding risks of collision and spectral overlap.

As direct-to-device systems become more prevalent, regulatory bodies are under increasing pressure to coordinate spectrum allocation, enforce orbital traffic rules, and ensure that public-interest concerns—like equitable access and scientific impact—are considered in commercial deployments.