shapecharge / Getty Images

(shapecharge / Getty Images)Quick Read

Those born in 1960 face full retirement age of 67, the highest under current law.

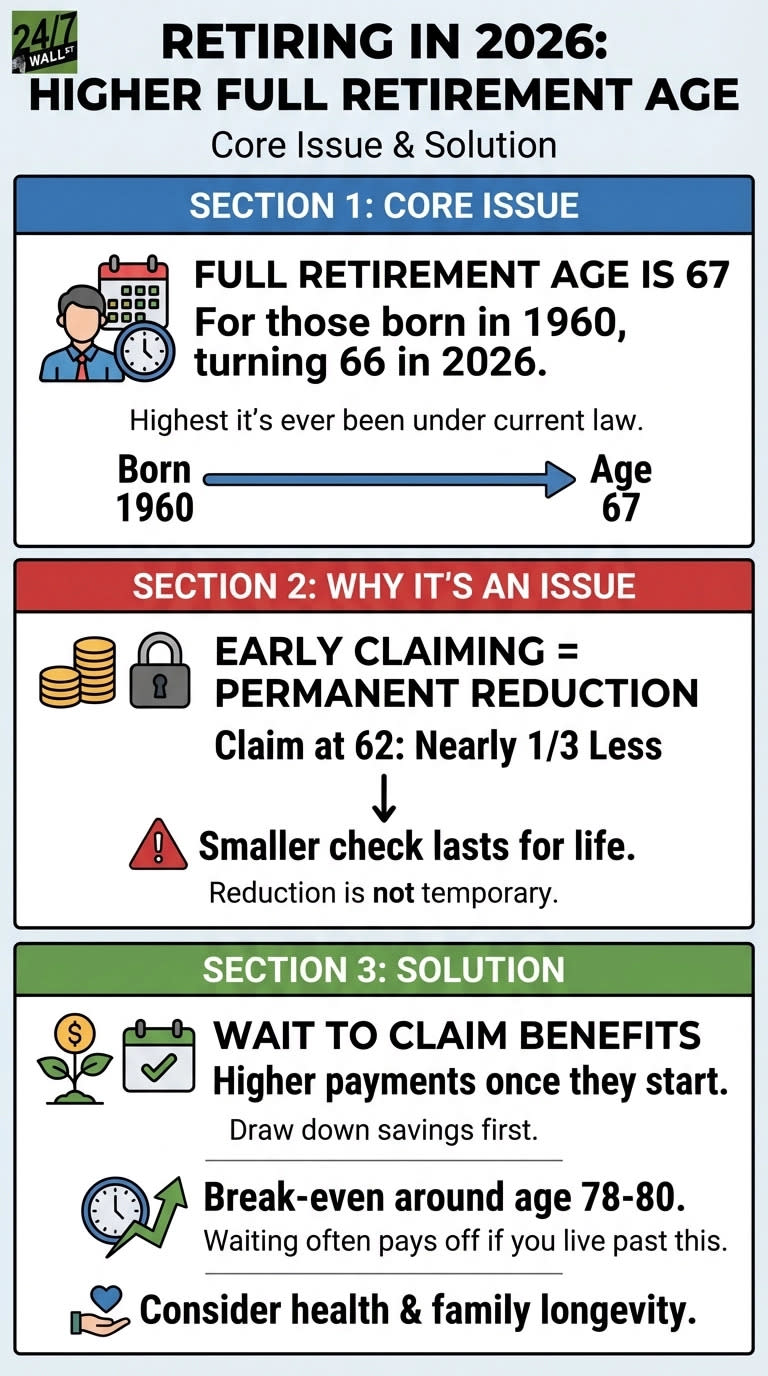

Claiming at 62 cuts monthly benefits by nearly one-third permanently versus waiting until 67.

Break-even for delaying benefits to 67 occurs around age 78 to 80.

If you were born in 1960, you’re turning 66 in 2026 and facing a milestone that earlier retirees didn’t encounter: a full retirement age of 67. This is the highest it’s ever been under current law and fundamentally changes the math around when to claim Social Security benefits.

The 1960 birth year represents the final step in a decades-long transition. Earlier retirees enjoyed lower full retirement ages—those born in 1937 or earlier could claim full benefits at 65. Congress gradually increased this threshold to shore up the program’s finances, and the 1960 cohort bears the full weight of that policy shift with a 67-year requirement.

The One Decision That Matters Most: When You Claim

The timing of your claim creates a permanent difference in monthly income. Starting benefits at 62 means accepting a significant reduction that reflects the additional years Social Security expects to pay you. For context, someone who would receive full benefits at 67 would see their monthly check reduced by nearly a third if they claim early—turning what could be a comfortable monthly payment into a more modest amount that must stretch just as far. This reduction isn’t temporary; it lasts for life.

Claiming early means smaller checks for potentially 20 or 30 years. Waiting until 67 means five years without Social Security income, but higher payments once they start. The break-even point typically falls around age 78 to 80. If you expect to live past that, waiting often pays off.

24/7 Wall St.

(24/7 Wall St.)

For those born in 1960 and turning 66 in 2026, the full retirement age for Social Security benefits is 67. This infographic outlines the implications of early claiming and suggests strategies for maximizing payments.

The reduction from early claiming is permanent. You can’t change your mind at 70 and suddenly get full benefits. The only exception is a narrow withdrawal window within 12 months of claiming, which requires repaying every dollar received.

How This Interacts With Other Retirement Income

If you have a 401(k) or IRA, the question becomes whether you can afford to delay Social Security by drawing down savings first. This strategy preserves the higher monthly benefit while living off investments during your early 60s.

The tax picture adds another layer of complexity. While the recent 2.8% cost-of-living adjustment provides some relief against inflation, higher benefit amounts can create an unexpected tax burden. Social Security income becomes taxable when combined with other retirement income, and this becomes especially problematic when required minimum distributions from retirement accounts begin in your 70s. The result is a tax situation that catches many retirees off guard.

What to Think Through Before Deciding

The hardest mistake to undo is claiming too early without considering your health and family longevity. If your parents lived into their 90s and you’re in good health, the case for waiting strengthens considerably. If you need the income now or have serious health concerns, claiming at 62 may be the practical choice.

Another factor: spousal benefits. If you’re married, the higher earner’s claiming decision affects survivor benefits. Waiting until 67 locks in a larger benefit for the surviving spouse.

Circumstances differ, and details like part-time work, pensions, or unexpected expenses can shift the calculation. What matters most is understanding that a full retirement age of 67 means the early claiming penalty is steeper than it was for previous generations, and that difference compounds over decades of retirement.

It’s Time To Rethink Passive Investing

For more than a decade, the investing advice aimed at everyday Americans followed a familiar script: automate everything, keep costs low, and don’t touch a thing. And increasingly, investors are realizing that being completely hands-off also means being completely disengaged.

That realization hits like a lightning bolt when you realize not just how much better your returns could be, but that there are amazing offers like one app where new self-directed investing accounts funded with as little as $50 can receive stock worth up to $1,000.

Take back your investing and start earning real returns, your way.